The Value of Hard Work and Humility

After 25 years on a waiting list, my father’s family immigrated to the US from the shattered remnants of post WWII Europe. Arriving here as a 13 year old, my dad would quickly go from not being able to speak English to attending one of America’s most prestigious universities. As time went on he would gather advanced degrees and work tirelessly for a unique nonprofit to help bring cutting edge engineering solutions to the US military.

Having appropriately flattered my father let me get to the actual point. His brilliance and kindness are only matched by his obdurate insistence on doing everything the hard way. Faced with housing his family he bought some land, cut down a lot of trees and built a house…on the nights and weekends. Growing up in a family where “a restful weekend” typically involved a chainsaw, tractor and a fair bit of dangerous labor has left me with some odd hobbies.

I always look forward to visiting the home my father built and raised me in. My dad and I still work shoulder to shoulder on many weekends. The smell of diesel exhaust pouring out of our Kubota tractor and the sound of a chainsaw running full tilt brings a grin to my face. I know I am home. In my life, hard work and burning fuel are directly related to productivity and progress.

Today the world is awash in stories about “wealth without work.” This is not a new thing. It is a recurring theme of speculative manias that dot human history more-often than one might believe. Our historically informed quantamental approach to investing has hoisted the “high risk” flags in a manner beyond that seen at either the peak of the internet or mortgage bubbles of 1999 and 2007. The crucial investment insights offered by the likes of Mr. Klarman’s Margin of Safety book have been completely abandoned.

Look at the list of names trading at valuations far above those seen at the peak of the dot.com bubble highlighted in this one pager. The market is, once again, creating the illusion of wealth as investors pile into firms that race higher despite dubious business models. Markets intermittently succumb to these bouts of reckless stock market speculation. And markets are doing it again. We believe it will end in the bear markets that have always followed such periods.

Get our insights direct to your inbox: SUBSCRIBE

Economic Activities are Essential to Income & Wealth Creation:

If there was a way to give everyone everything without consequences or effort we believe the world would have done it. Yield Curve Control – where the Fed just prints money with the explicit goal of holding borrowing rates down and other policies will only increase the possibility of sending the measure of inflation higher, a major risk to investors we explained in our Inflation of the 1970s white paper. To state the obvious, if you have 10% more money but a basket of goods you might typically buy costs 15% more, you are worse off.

Let’s work with the historically proven assertion that nobody can forecast the future with any accuracy or reliability[1]. As Buffett is fond of saying “Forecasts may tell you a great deal about the forecaster; they tell you nothing about the future.” This view also happens to be held by living investment legend Seth Klarman. As we will share in our upcoming learning piece on his timeless book Margin of Safety, Risk-Averse Value Investing Strategies for the Thoughtful Investor, his skepticism of forecasting the future is founded on the bedrock of thoughtful humility.

Like it or not, hydrocarbons are still a critical part of global economic activity. Yet where do markets price companies that we rely on for a barrel of oil today? In the enthusiasm for ESG, markets have forgotten: we simply are not there yet. Tesla alone is worth almost as much as the entire energy sector in the S&P.

The End of the Energy Capital Supply Glut:

As the Houston Chronical recently documented here (hat tip DM!), E&P companies are scrapping rigs with 30++ year operational lives when they are only 10 years old. We are not energy experts but we simply cannot recall seeing the “raw materials” of oil production scrapped on this scale.

In fact – we’re not sure we’ve seen quite this much supply destruction in the energy sector in such a short period of time. How much more difficult will it be to ramp crude oil production if demand accelerates? What is the average change in prices required to bring new capacity online? In 2019 the US was the world’s energy capital. We were the largest oil exporting country and the largest supplier to overall global oil production.

The ESG movement is good for the world and a huge thematic trend. The beneficiaries in the battery electric vehicle space and many others have seen outsized returns. They may continue to do so. But we think it might also be creating the perfect storm for oil.

Everyone is dumping energy as an asset class. Many OECD countries are withdrawing, or contemplating withdrawing, billions in subsidies for oil and gas projects which simply means hurdle rates for projects are only going higher. This tremendous supply constraint is happening right in front of the most cash rich consumer in US history. A consumer we believe is hell-bent on seeing family, friends and going on vacations which could create a tremendous increase in demand for oil.

We encourage you to read the recent quarter from XOM. After burning cash for 9 straight quarters XOM is back in the black. Paying down debt. Reducing costs. Reducing capex. Deep water production now generates a 10% return….at $35 oil[2]. Chemicals are shattering profit records. Shale costs are down 40%. At 15x forward earnings XOM doesn’t look “dirt cheap” but what price deck is being used to get those numbers? Does it contemplate the massive cost reductions? What if oil prices were to rise?

In mid-2019 XOM was at $80/share despite burning cash, adding leverage and oil was right where it is today. The stock is now at $58, costs have been slashed, capex tamped down, profitability exploding, debt being reduced and the dividend covered.

If oil companies continue these capital allocation policies of debt reduction it will reduce fear and bring higher multiples. This is at the core of our two white papers on the power of debt reduction and its impact on stock valuations. The papers were titled Activism Lite Part I and Part II. Reducing leverage is a massive source of alpha and the more “value” embedded in the stock the more bang you get from multiple expansion.

Tarred and feathered by the shale collapse, junk bond-holders who went into energy are now making capital for these investments expensive.[3] This is one of the few places where capital is scarce and highly valued. How many million barrels per day of production will now require consistently higher natural gas and oil prices to receive funding today vs. just a few years ago?

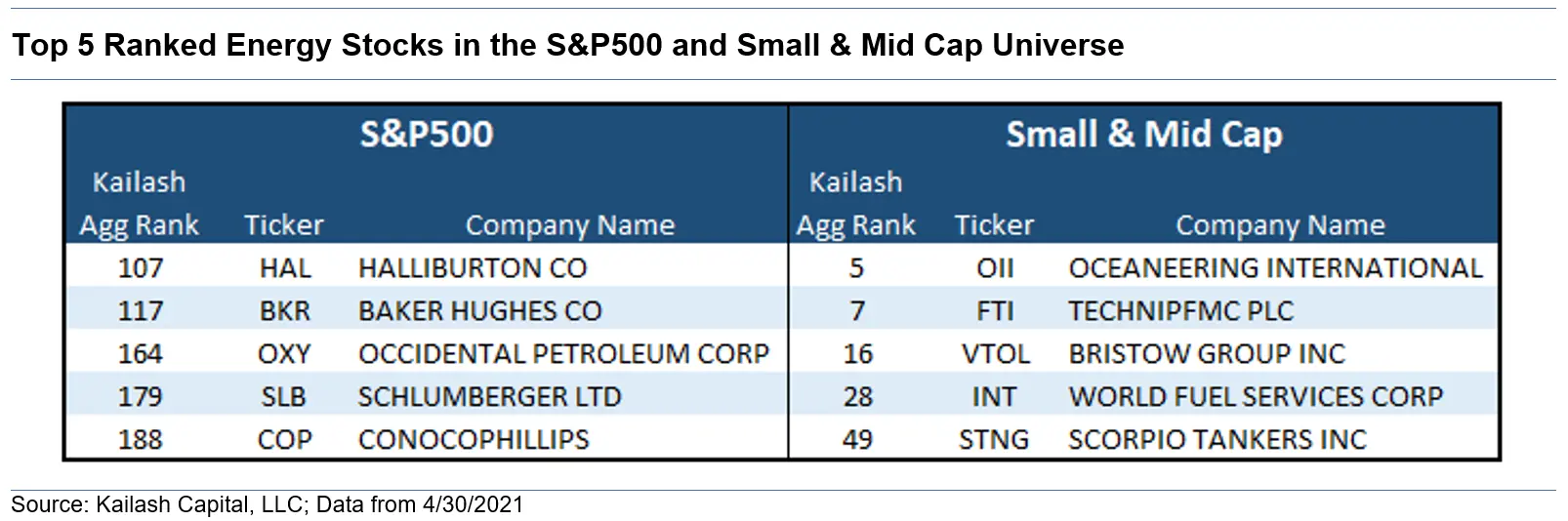

In the figure below we provide the five highest ranked energy companies in our S&P 500 and Small & Mid Cap models. You will note – XOM is not among them! We use that stock merely to make the broader case that today is a compelling time to be doing some work on one of the least-liked sectors in the market. For those bearish on energy, we strongly encourage even the most confident forecasters to contemplate “what if my view of the future is wrong?”

How our research platform can help you no matter what the consumer price index cpi does:

No matter if you are a bear or bull the history books are unambiguous: buying high quality cash-generating businesses at fair to low prices is a terrific way to compound wealth. Today’s market is a highly bifurcated one. Part of the market is trading at obscene multiples as government subsidized capital, weak covenants from lenders and a speculative mania drive some oil stocks to absurd prices. The good news is that in these manic times there are pockets of opportunity that we believe, held over the long haul, will provide far better returns than those available in fixed income.

Kailash’s newsletters and investment tools are committed to helping people interested in compounding capital using the most time-tested methods we know of. Good companies, good managements and good businesses purchased at reasonable prices. You can find them on our website or by contacting us. To learn about and gain access to our powerful tools built using research proven out in practice and academia please:

- Click here for our paper explaining our Stock Ranking Tools

- Click here for our research on some of the pitfalls faced by investors in index funds

- Visit our research explaining how to identify firms manipulating earnings to fool investors

For those of you unfamiliar with Kailash, we believe our organization provides cutting edge, thought-driven, investment analysis tools at prices others simply cannot match. Our research staff has been together for over a decade and has well over 100 years of experience. The team includes proven veterans in the investment management business and one of the most prominent academics in the field of behavioral finance. Our services bring the best of breed quantamental tools and themes to your doorstep.

Said differently: we think all someone needs to be interested in our list of energy companies is a bit of financial prudence, some common sense and the recognition of all the money being created by the Federal Reserve.

Disclaimer

The information, data, analyses, and opinions presented herein (a) do not constitute investment advice, (b) are provided solely for informational purposes and therefore are not, individually or collectively, an offer to buy or sell a security, (c) are not warranted to be correct, complete or accurate, and (d) are subject to change without notice. Kailash Capital Research, LLC and its affiliates (collectively, “Kailash Capital Research, LLC ”) shall not be responsible for any trading decisions, damages or other losses resulting from, or related to, the information, data, analyses or opinions or their use. The information herein may not be reproduced or retransmitted in any manner without the prior written consent of Kailash Capital Research, LLC . In preparing the information, data, analyses, and opinions presented herein, Kailash Capital Research, LLC has obtained data, statistics, and information from sources it believes to be reliable. Kailash Capital Research, LLC , however, does not perform an audit or seeks independent verification of any of the data, statistics, and information it receives. Kailash Capital Research, LLC and its affiliates do not provide tax, legal, or accounting advice. This material has been prepared for informational purposes only and is not intended to provide, and should not be relied on for tax, legal, or accounting advice. You should consult your tax, legal, and accounting advisors before engaging in any transaction. © 2021 Kailash Capital Research, LLC – All rights reserved.

Nothing herein shall limit or restrict the right of affiliates of Kailash Capital Research, LLC to perform investment management or advisory services for any other persons or entities. Furthermore, nothing herein shall limit or restrict affiliates of Kailash Capital Research, LLC from buying, selling or trading securities or other investments for their own accounts or for the accounts of their clients. Affiliates of Kailash Capital Research, LLC may at any time have, acquire, increase, decrease or dispose of the securities or other investments referenced in this publication. Kailash Capital Research, LLC shall have no obligation to recommend securities or investments in this publication as result of its affiliates’ investment activities for their own accounts or for the accounts of their clients.