- Beta, or the amount a stock price goes up and down relative to the market, is a popular measure of “risk”

- Famous investors such as Seth Klarman have observed that this idea is “preposterous”[1]

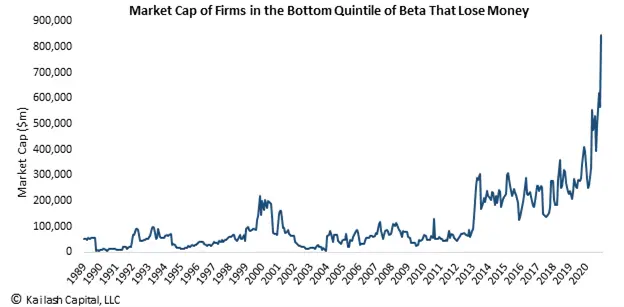

- Below is the market cap of firms that lose money but are very low risk[2] based on beta

- In our CFTC here we documented that there is a record $6 trillion worth of stocks losing money

- We believe common sense indicates that expensive firms bleeding cash are dangerous

Get our insights direct to your inbox: SUBSCRIBE

As documented in our research on volatility and beta we discussed the dangers of relying on these commonly used and accepted measures of “risk.”

See below for a list of stocks that lost money in 2019 (pre Covid) and are still losing money today but beta is telling you are “low risk”

Portfolio Betas Lack Critical Quality & Valuation Information:

Investopedia offers a terrific summary of Beta that you can find here. KCR’s research team has a famous academic on staff who could grind your brain cells into the floor going into the painful details of substantive math underpinning how this metric contemplates cash flows, market risks, systematic risks and numerous other items.

For our purposes here, however, we are going to keep it simple. For an individual stock, beta measures its “risk” using statistical inputs. A stock with a beta of 1.0 is, in theory, exactly as risky as the overall market. Companies with higher beta coefficients are riskier and those with numbers below “1” are less volatile than the market index.

KCR has written a good deal about beta and we both respect it but also believe it has serious limitations. We encourage investors to think of it more like one of many inputs in determining how risky a stock might be. Let’s use the list of comparable companies below to make this point more clearly.

The Beta of a Portfolio of These Money Losers Looks “Wrong”

In our view, the list below is emblematic of the shortcomings of using beta as a catch-all to assess a firm’s risk. All of the companies in the list below lost money pre-Covid and continue to do so today. That means they could not turn a profit when the economy was flying and still cannot turn a profit in the current environment. Consistent with our research and intuition, companies that lose money tend to have weaker return characteristics.

Looking at the list below, the fact that beta deems all these companies to be less risky than the market strikes us as evidence of nonsense! A company’s debt, debt to equity ratio, operating and financial leverage, capital structure, tax rate, and valuation are all immensely important factors when thinking about a stock’s risk.

In an age when asset classes like bonds no longer offer any substantive income, we believe understanding the weighted average risk of your portfolio has never been more important or more difficult to do.

Please read our research or reach out to info@kailashconcepts.com if you would like to learn more. As always, we are grateful for our new readers and look forward to connecting with you!

Disclaimer

The information, data, analyses, and opinions presented herein (a) do not constitute investment advice, (b) are provided solely for informational purposes and therefore are not, individually or collectively, an offer to buy or sell a security, (c) are not warranted to be correct, complete or accurate, and (d) are subject to change without notice. Kailash Capital Research, LLC and its affiliates (collectively, “Kailash Capital Research, LLC ”) shall not be responsible for any trading decisions, damages or other losses resulting from, or related to, the information, data, analyses or opinions or their use. The information herein may not be reproduced or retransmitted in any manner without the prior written consent of Kailash Capital Research, LLC . In preparing the information, data, analyses, and opinions presented herein, Kailash Capital Research, LLC has obtained data, statistics, and information from sources it believes to be reliable. Kailash Capital Research, LLC , however, does not perform an audit or seeks independent verification of any of the data, statistics, and information it receives. Kailash Capital Research, LLC and its affiliates do not provide tax, legal, or accounting advice. This material has been prepared for informational purposes only and is not intended to provide, and should not be relied on for tax, legal, or accounting advice. You should consult your tax, legal, and accounting advisors before engaging in any transaction. © 2021 Kailash Capital Research, LLC – All rights reserved.

Nothing herein shall limit or restrict the right of affiliates of Kailash Capital Research, LLC to perform investment management or advisory services for any other persons or entities. Furthermore, nothing herein shall limit or restrict affiliates of Kailash Capital Research, LLC from buying, selling or trading securities or other investments for their own accounts or for the accounts of their clients. Affiliates of Kailash Capital Research, LLC may at any time have, acquire, increase, decrease or dispose of the securities or other investments referenced in this publication. Kailash Capital Research, LLC shall have no obligation to recommend securities or investments in this publication as result of its affiliates’ investment activities for their own accounts or for the accounts of their clients.