Can the Might of Mean Reversion Send Small Caps Higher?

Our research team published a very simple Chart for The Curious earlier this month comparing the relative size of small cap vs large-cap stocks. While naïve, the implication was striking. Based on history, the difference between large and small cap stocks indicates that recent gains by small caps vs. large caps may have much further to run.

As documented in our research, we believe that asset bloat in index funds and speculative ETFs that focus on large cap, loss-making firms, has caused this anomaly. In this paper we intend to:

- Extend on The Low Cost of High Quality which showed there is a speculative cohort of small caps that are as financially weak today and more expensive than they were at the peak of the internet bubble!

- Show how a reversion to the long term averages of “large cap vs. small cap” could generate large gains for small cap investors[1]

- Offer investors a portfolio from our Small Cap Model that we believe may represent a generational opportunity to pay historically low prices for some of the highest quality Small Caps – a painfully obvious alternative to “speculation investing” in our view

Get our White Papers direct to your inbox: SUBSCRIBE

History suggests that the market bubble today is so dangerous and the opportunity to buy high-quality stocks at lower prices so obvious that keeping things simple is in the best interests of our readers. We would rather be roughly correct than precisely wrong to borrow from one of Buffett’s quips.

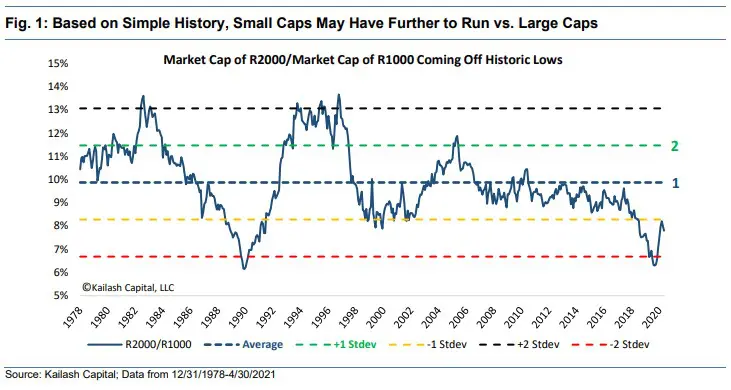

The chart below shows the market cap of Small Cap divided by the market cap of Large Cap Firms.

- Small Cap stocks need to rise 27% to get back to their average weight vs. large cap stocks[2]

- Small Cap stocks need to rise 47% to get back to where they went post the dot.com crash!2

Are Large Caps Losing Touch with Reality?

Our research team has written about Buffett’s valuation metric, which scales Market Cap to GDP, repeatedly over the years. Most recently, we published a Chart For The Curious showing that markets were at frightening valuations. We have documented that, while useless for timing markets, this metric has a potent history of predicting future returns over a long time horizon.

Disclaimer

The information, data, analyses, and opinions presented herein (a) do not constitute investment advice, (b) are provided solely for informational purposes and therefore are not, individually or collectively, an offer to buy or sell a security, (c) are not warranted to be correct, complete or accurate, and (d) are subject to change without notice. Kailash Capital Research, LLC and its affiliates (collectively, “Kailash Capital Research, LLC ”) shall not be responsible for any trading decisions, damages or other losses resulting from, or related to, the information, data, analyses or opinions or their use. The information herein may not be reproduced or retransmitted in any manner without the prior written consent of Kailash Capital Research, LLC . In preparing the information, data, analyses, and opinions presented herein, Kailash Capital Research, LLC has obtained data, statistics, and information from sources it believes to be reliable. Kailash Capital Research, LLC , however, does not perform an audit or seeks independent verification of any of the data, statistics, and information it receives. Kailash Capital Research, LLC and its affiliates do not provide tax, legal, or accounting advice. This material has been prepared for informational purposes only and is not intended to provide, and should not be relied on for tax, legal, or accounting advice. You should consult your tax, legal, and accounting advisors before engaging in any transaction. © 2021 Kailash Capital Research, LLC – All rights reserved.

Nothing herein shall limit or restrict the right of affiliates of Kailash Capital Research, LLC to perform investment management or advisory services for any other persons or entities. Furthermore, nothing herein shall limit or restrict affiliates of Kailash Capital Research, LLC from buying, selling or trading securities or other investments for their own accounts or for the accounts of their clients. Affiliates of Kailash Capital Research, LLC may at any time have, acquire, increase, decrease or dispose of the securities or other investments referenced in this publication. Kailash Capital Research, LLC shall have no obligation to recommend securities or investments in this publication as result of its affiliates’ investment activities for their own accounts or for the accounts of their clients.

May 26, 2021 |

| Authors: Matthew Malgari, Nathan Przybylo, Dr. Sanjeev Bhojraj and John Durkin

May 26, 2021

Authors: Matthew Malgari, Nathan Przybylo, Dr. Sanjeev Bhojraj and John Durkin