Are Stocks With the Highest Growth Healthy?

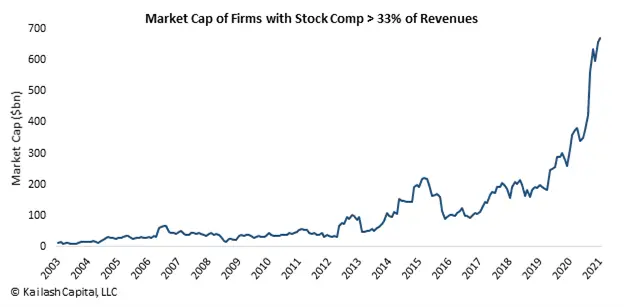

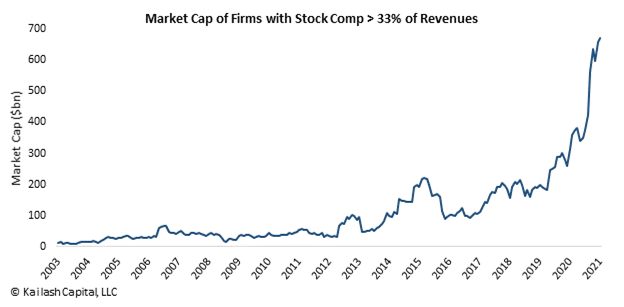

- The chart shows the market cap of firms where stock compensation represents over a third of SALES

- We have written three pieces about how stock compensation creates the illusion of cost-free cash flow at some firms

- Specifically we wrote a Quick Take here, a white paper here and the academic on the team published a peer reviewed piece here

- When companies pay management and employees in stock, they add it back to cash profits

- While legal, we believe reported “cash profitability” is overstated and shareholders are often unknowingly paying the tab

Get our insights direct to your inbox: SUBSCRIBE

History will decide if this ends in steep losses and more regulations as many of the “shiny objects” – stocks investors believe will grow fast – are often entirely dependent on stock compensation to subsidize loss-making sales growth.

We believe executive stock options should be reported as compensation expense in the statement of cash flows.

In our paper The Great Inflation we noted that many high growth stocks for 2021 were “….easily seen devices by which equity and bond holders transfer funds into their coffers to subsidize high rates of sales growth.” We believe the abuse of stock comp expense has merely moved from the income statement to the statement of cash flows. The idea that total compensation – including stock based compensation – can be deemed “non cash” when there is serious dilution underway strikes us as disingenuous.

Below is a list of firms that have stock compensation expense that is equivalent to 33% of revenues. To make the list, a dubious “award”, these firms also could not be in the biotech sector, had to have a market cap greater than $1bn and trade at over 10x price to sales.

Want more content? Subscribe now

Disclaimer

The information, data, analyses, and opinions presented herein (a) do not constitute investment advice, (b) are provided solely for informational purposes and therefore are not, individually or collectively, an offer to buy or sell a security, (c) are not warranted to be correct, complete or accurate, and (d) are subject to change without notice. Kailash Capital Research, LLC and its affiliates (collectively, “Kailash Capital Research, LLC ”) shall not be responsible for any trading decisions, damages or other losses resulting from, or related to, the information, data, analyses or opinions or their use. The information herein may not be reproduced or retransmitted in any manner without the prior written consent of Kailash Capital Research, LLC . In preparing the information, data, analyses, and opinions presented herein, Kailash Capital Research, LLC has obtained data, statistics, and information from sources it believes to be reliable. Kailash Capital Research, LLC , however, does not perform an audit or seeks independent verification of any of the data, statistics, and information it receives. Kailash Capital Research, LLC and its affiliates do not provide tax, legal, or accounting advice. This material has been prepared for informational purposes only and is not intended to provide, and should not be relied on for tax, legal, or accounting advice. You should consult your tax, legal, and accounting advisors before engaging in any transaction. © 2021 Kailash Capital Research, LLC – All rights reserved.

Nothing herein shall limit or restrict the right of affiliates of Kailash Capital Research, LLC to perform investment management or advisory services for any other persons or entities. Furthermore, nothing herein shall limit or restrict affiliates of Kailash Capital Research, LLC from buying, selling or trading securities or other investments for their own accounts or for the accounts of their clients. Affiliates of Kailash Capital Research, LLC may at any time have, acquire, increase, decrease or dispose of the securities or other investments referenced in this publication. Kailash Capital Research, LLC shall have no obligation to recommend securities or investments in this publication as result of its affiliates’ investment activities for their own accounts or for the accounts of their clients.