Bloomberg News recently published an article, Amazon Fights Union Drive With Fact-Free Bombast, discussing Amazon’s alleged use of misinformation to prevent employees from unionizing. In the same manner Kailash recused itself from having a “bull” or “bear” thesis on Bitcoin, we will recuse ourselves from any discussion of unions. What we would like to draw our readers’ attention to however is the method by which Amazon pays many senior executives. In the Bloomberg article it noted that the former head of Amazon’s logistics business was awarded stock compensation worth $160 million dollars.

Get our insights direct to your inbox: SUBSCRIBE

In the wake of the scandals that occurred during the financially profligate dot.com bubble, rule FAS123 was passed requiring stock compensation be expensed in a company’s income statement. In papers written both in the professional and academic worlds, Kailash has used Amazon as an example of how cash flow accounting contradicts the intent of FAS123. The Kailash note found here showed how Amazon’s well explained and GAAP compliant use of lease and stock comp accounting could potentially cause confusion among analysts. Kailash’s academic expert on stock compensation put his work, Stock Compensation Expense, Cash Flows and Inflated Valuations through peer review. His work made it painfully clear that this GAAP compliant accounting method diminished the information value of traditional calculations of free cash flows.

Our views are obviously shared by many including Jamie Powell at the FT who noted the issue with stock compensation accounting in a 2018 article here. When it comes to accounting Kailash believes the headlines do plenty to explain the dubious nature of many practices common in today’s markets. Our views in both the professional and academic spheres express a belief that the regulators will either make a gentle amendment today or will be chasing the issue after an explosion of investor outrage in the wake of losses. While things like prudence and transparency have been slaughtered at the trough of improvident financial practices today, we believe that overstating profitability by billions is worth the attention of investors. Should we slide into a bear market, we believe these issues will land on the “front pages” of media around the world.

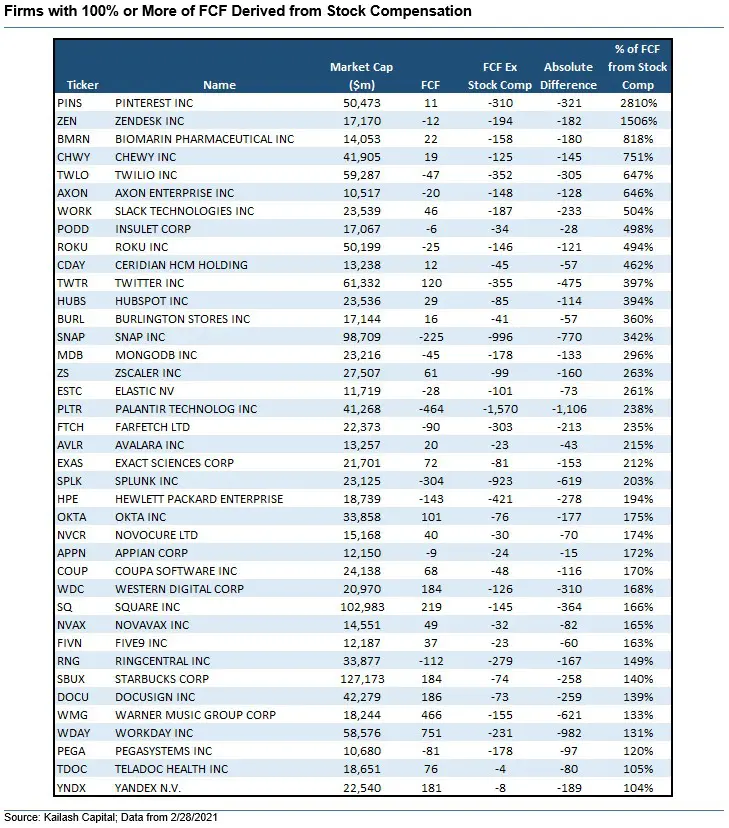

Kailash would like to note that Amazon is by no means the most aggressive user of stock compensation. We highlight them in our work due to the exemplary clarity of their footnotes and disclosures. In effect, the clarity of Amazon’s reporting makes understanding the magnitude of the issue easy. For copies of our research on this accounting chimera please click here. Below we have provided a list of firms that derive over 100% of their their free cash flows from stock compensation. We would like to note that many of the firms on this list are already at elevated valuations and this is merely another risk factor if the recent pullback in growth persists. If you would like to see how companies outside those listed below are impacted by stock compensation please contact us here.

Get our White Papers direct to your inbox: SUBSCRIBE

For a complete review of the myriad tools Kailash has for equity investors including:

- Equity Rankings

- Earnings Manipulation

- Peer Selection

- Short Selling

- Management Integrity

- Single Stock Heatmap

Please contact us here and a member of the team will reach out to your shortly.

For those who want to learn more details about stock compensation and how it works, if you have a friend with an Amazon logistics comp login they may be able to teach you more than we can. Barring that, there is no shortage of folks receiving stock comp that you may know. This is a researchers practical application of Peter Lynch’s “Buy What You Know” type approach to learning!

Disclaimer

The information, data, analyses, and opinions presented herein (a) do not constitute investment advice, (b) are provided solely for informational purposes and therefore are not, individually or collectively, an offer to buy or sell a security, (c) are not warranted to be correct, complete or accurate, and (d) are subject to change without notice. Kailash Capital Research, LLC and its affiliates (collectively, “Kailash Capital Research, LLC ”) shall not be responsible for any trading decisions, damages or other losses resulting from, or related to, the information, data, analyses or opinions or their use. The information herein may not be reproduced or retransmitted in any manner without the prior written consent of Kailash Capital Research, LLC . In preparing the information, data, analyses, and opinions presented herein, Kailash Capital Research, LLC has obtained data, statistics, and information from sources it believes to be reliable. Kailash Capital Research, LLC , however, does not perform an audit or seeks independent verification of any of the data, statistics, and information it receives. Kailash Capital Research, LLC and its affiliates do not provide tax, legal, or accounting advice. This material has been prepared for informational purposes only and is not intended to provide, and should not be relied on for tax, legal, or accounting advice. You should consult your tax, legal, and accounting advisors before engaging in any transaction. © 2021 Kailash Capital Research, LLC – All rights reserved.

Nothing herein shall limit or restrict the right of affiliates of Kailash Capital Research, LLC to perform investment management or advisory services for any other persons or entities. Furthermore, nothing herein shall limit or restrict affiliates of Kailash Capital Research, LLC from buying, selling or trading securities or other investments for their own accounts or for the accounts of their clients. Affiliates of Kailash Capital Research, LLC may at any time have, acquire, increase, decrease or dispose of the securities or other investments referenced in this publication. Kailash Capital Research, LLC shall have no obligation to recommend securities or investments in this publication as result of its affiliates’ investment activities for their own accounts or for the accounts of their clients.