The High Price of Promises in SpaceX

In 2023, KCR noticed that Chamath Palihapitiya was invoking the "Man in the Arena" concept from Theodore Roosevelt's spectacular Citizenship in a Republic speech given at the Sorbonne in 1910. We quickly unleashed our first-ever critique of any one individual in our 15-year history.

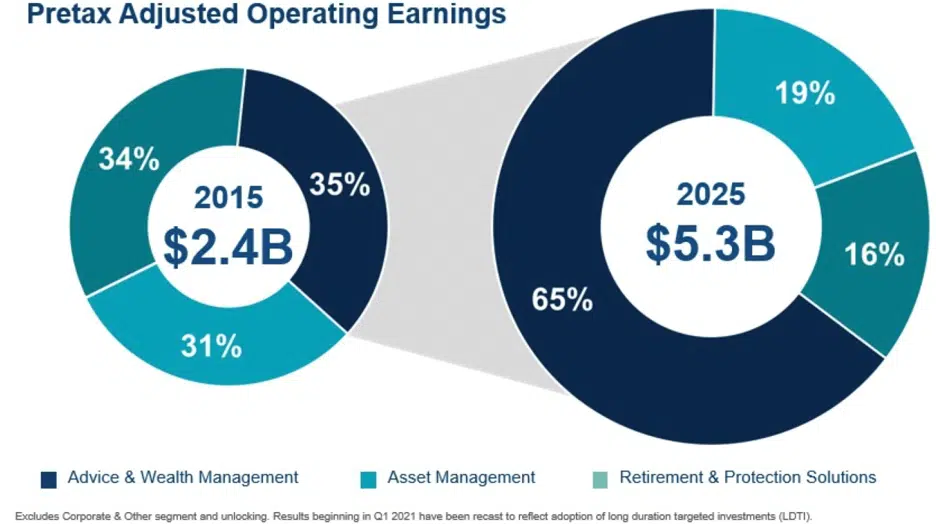

Ameriprise Financial, Inc (AMP)

Spun off from American Express in 2005, Ameriprise Financial, Inc. (AMP) is a diversified financial services company. It has three operating divisions: Advice and Wealth Management, by far AMP’s fastest growing unit, makes up about two-thirds of its adjusted operating earnings; while Asset Management and Retirement & Protection Solutions represent 16% and 19%, respectively, of this key financial metric.

The Market and the Economy: Two Sides, Same Coin?

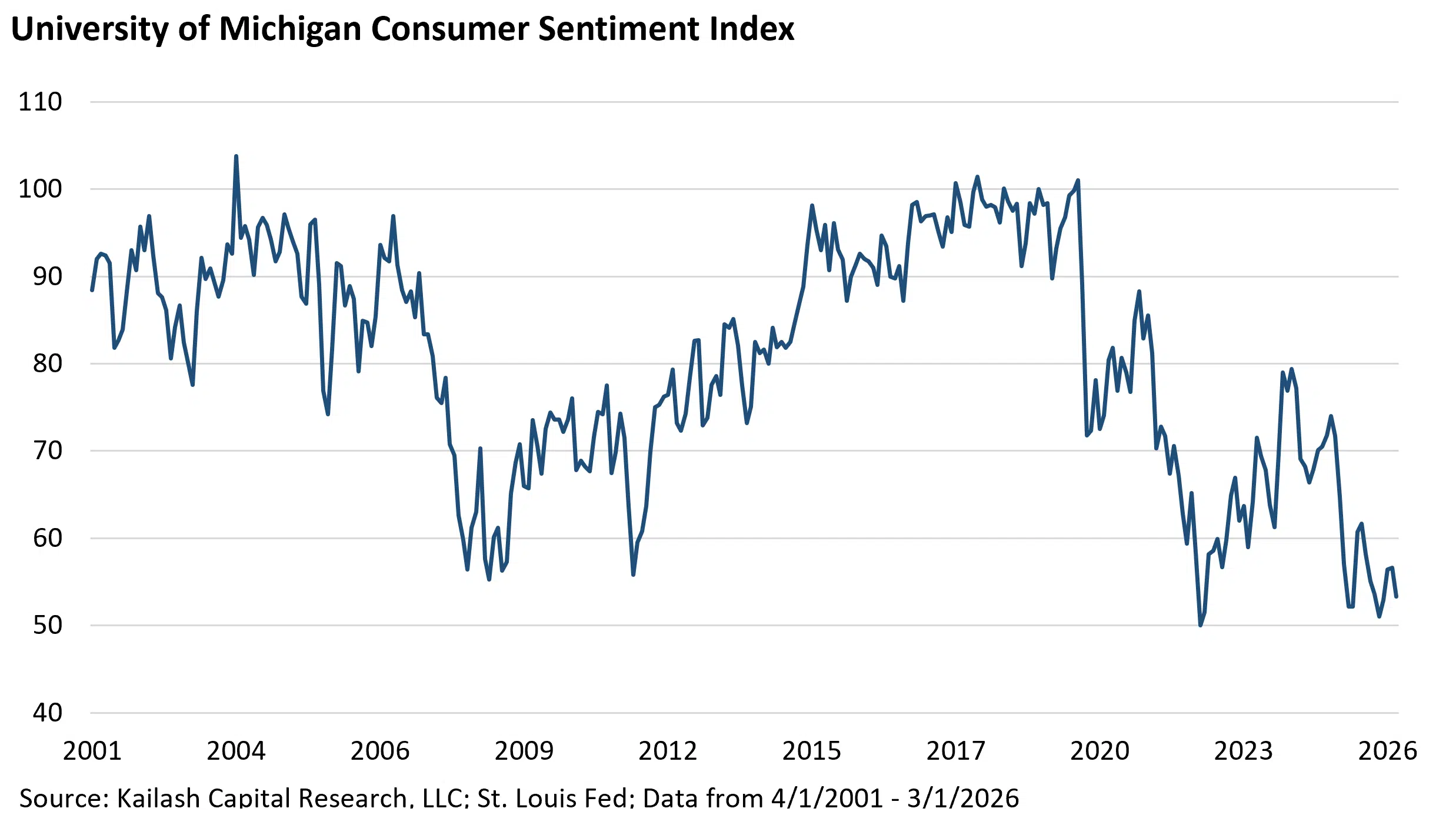

Consumers haven’t been this glum since COVID pandemic supply chain snarls met up with stimulus payments to push inflation up to levels not seen in decades. The University of Michigan Consumer Sentiment Index, which often correlates more tightly with grocery and gas prices than the stock market, is lower than it was during the global financial crisis of 2008.

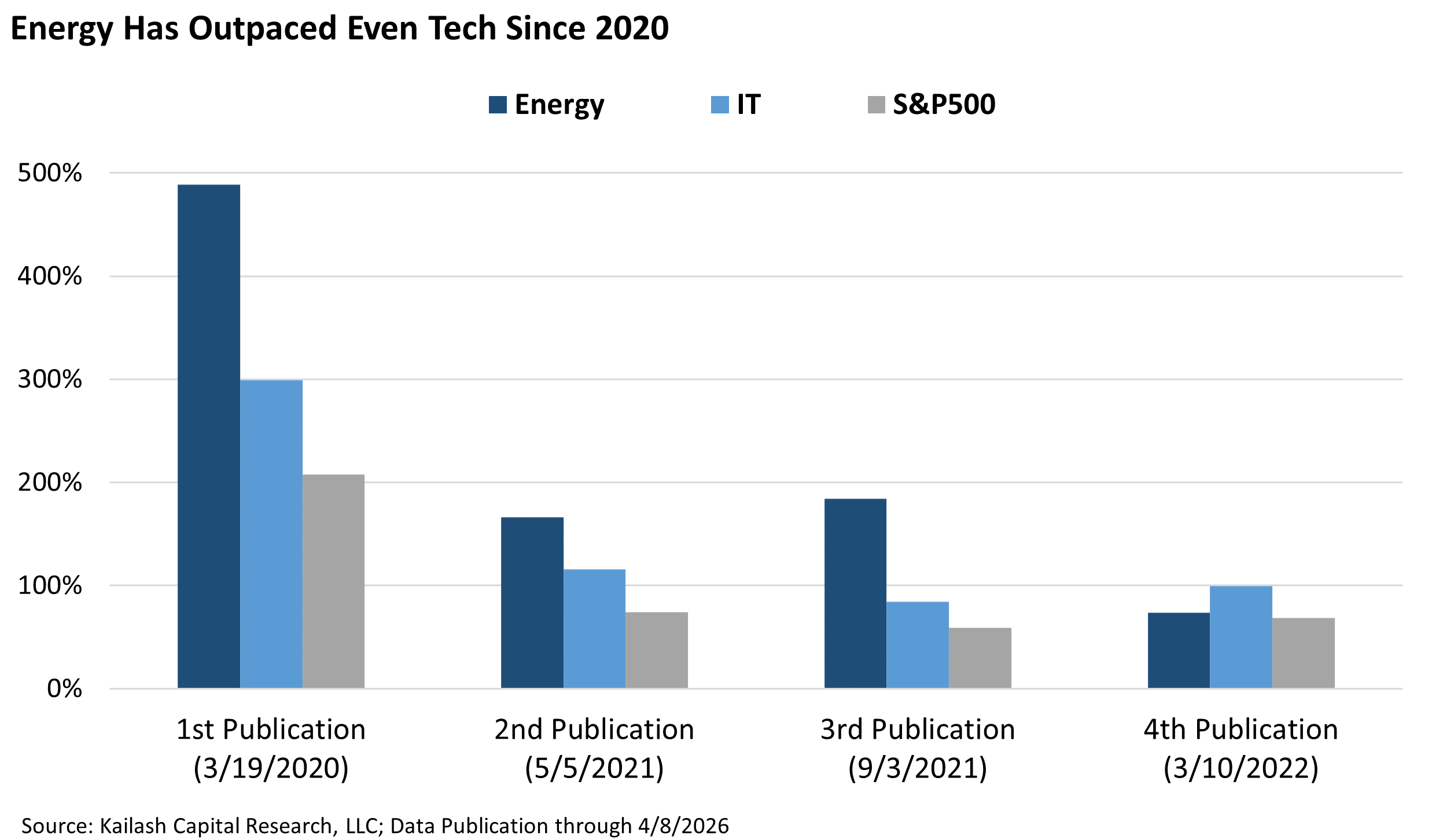

Information Technology & Energy: The Two Tails of Extrapolation Bias

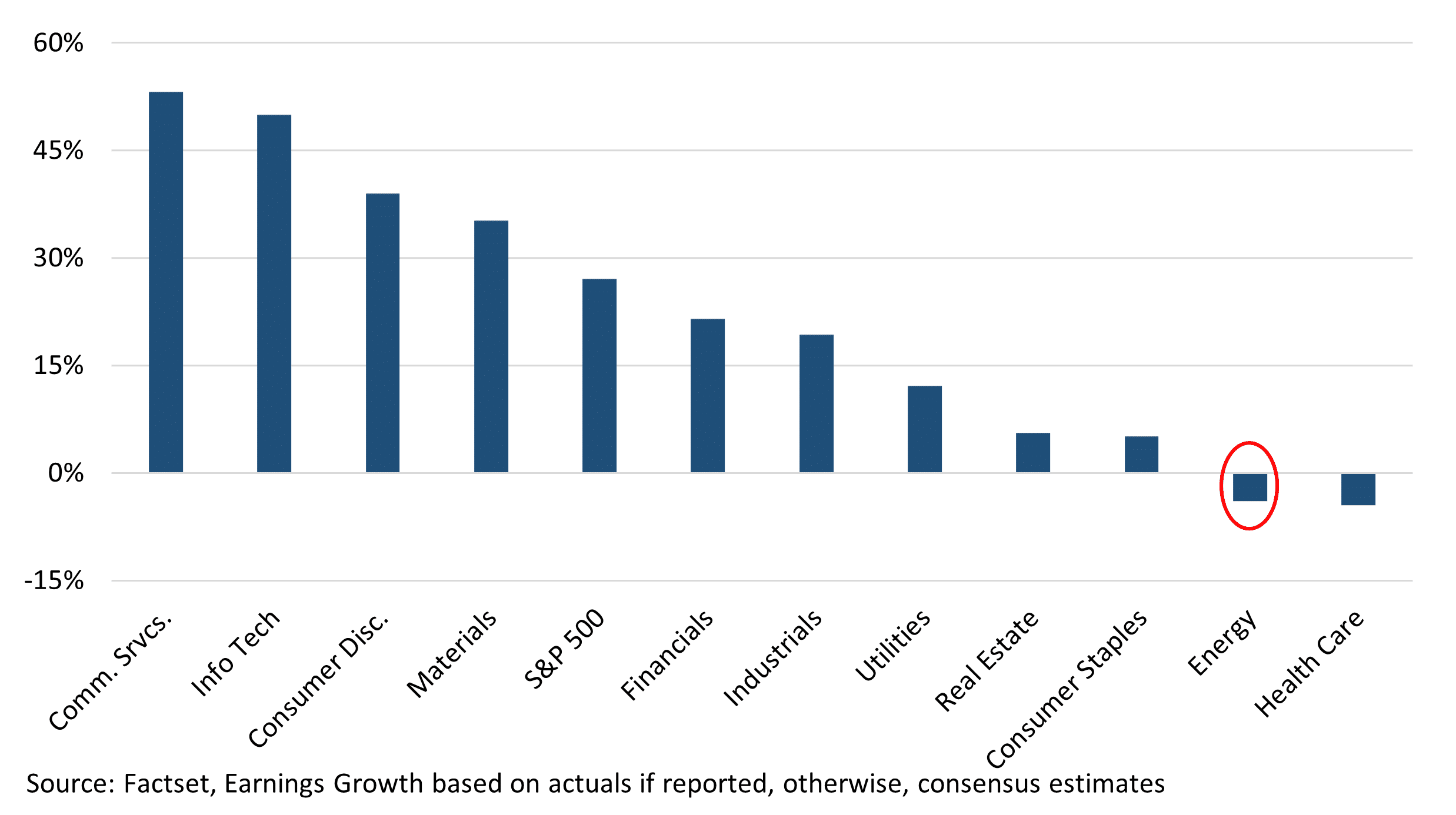

U.S. GDP grew 2% annualized in Q1 2026 after inflation, including gas prices hit their highest since 2022. Private non-residential fixed investment drove 70% of that growth, with "information-processing equipment" alone accounting for one-third of private demand growth over the past 12 months.

Enviri Corp (NVRI): A Small Stock with Big Upside?

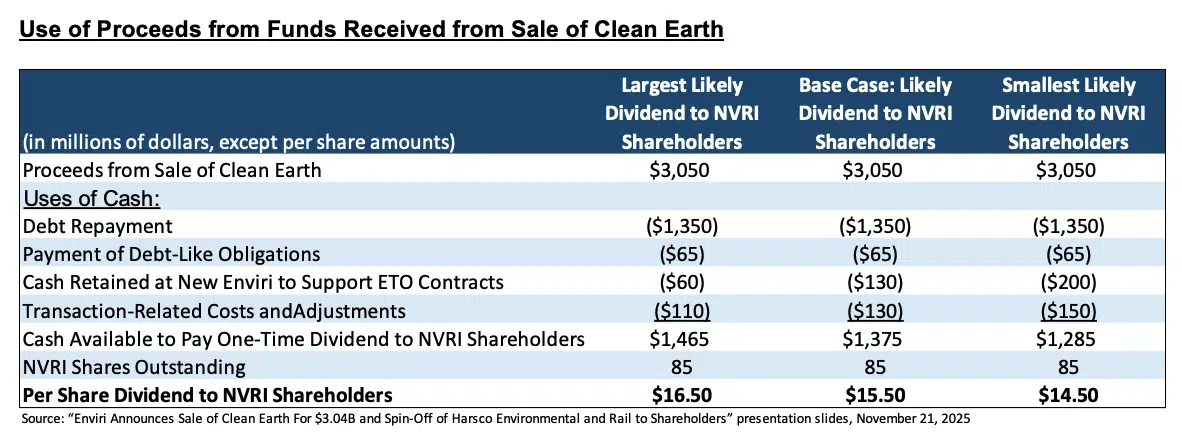

Like many conglomerates, Enviri Corporation (NVRI) has traded for many years at a discount to its sum-of-the-parts net worth. However, management has recently taken steps to close this discount with the announced sale of their largest division and a distribution of remaining assets to shareholders.

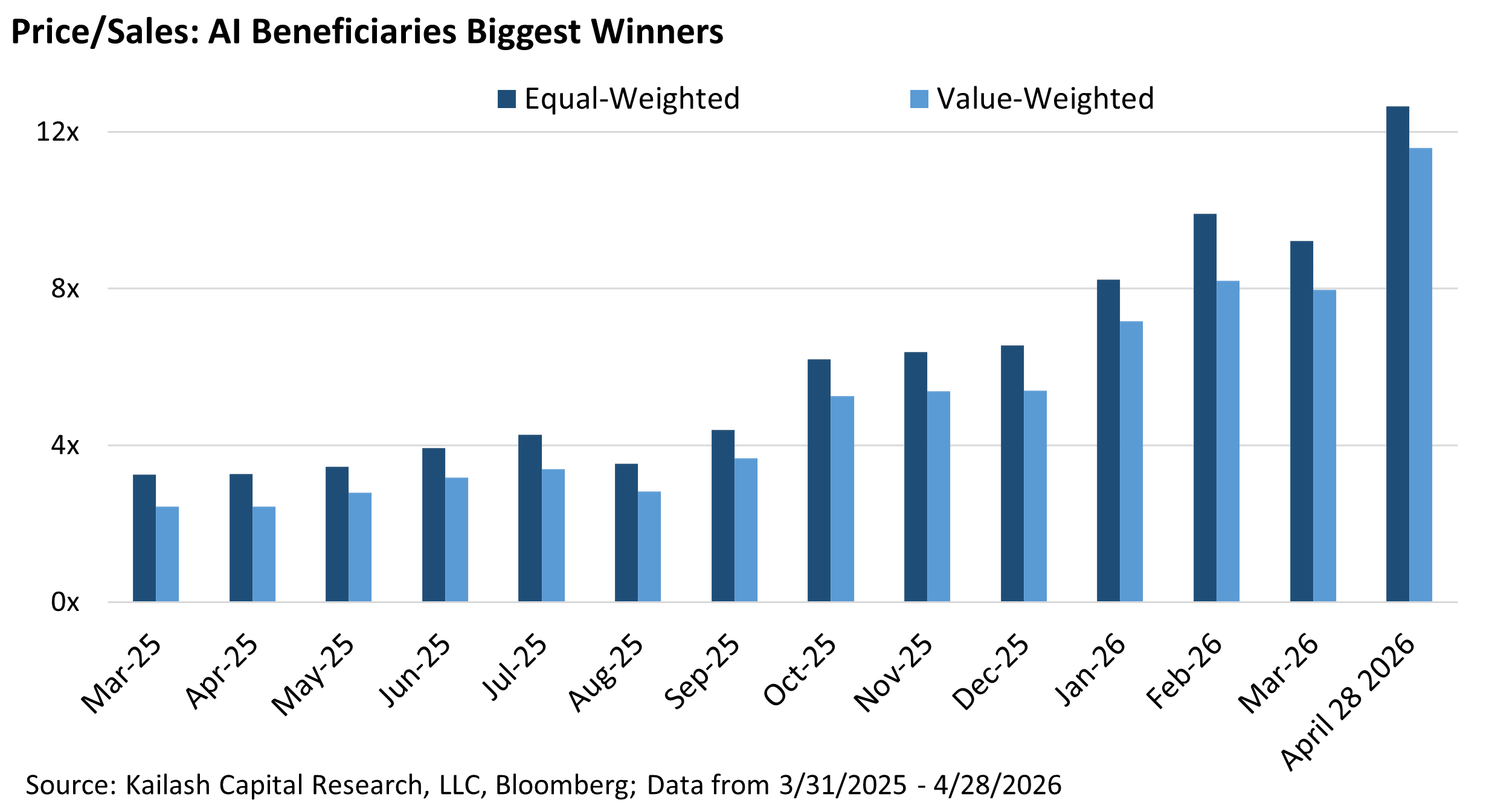

Anything for AI & Could Software Still be Far too Expensive?

The S&P 500 is up roughly 9% so far in April – less than one month! This despite the fact that the ongoing blockades in the Strait of Hormuz could turn into another “endless war” and is preventing many countries from getting the oil, natural gas, jet fuel, fertilizer, and petrochemicals they need to keep their economies functioning.

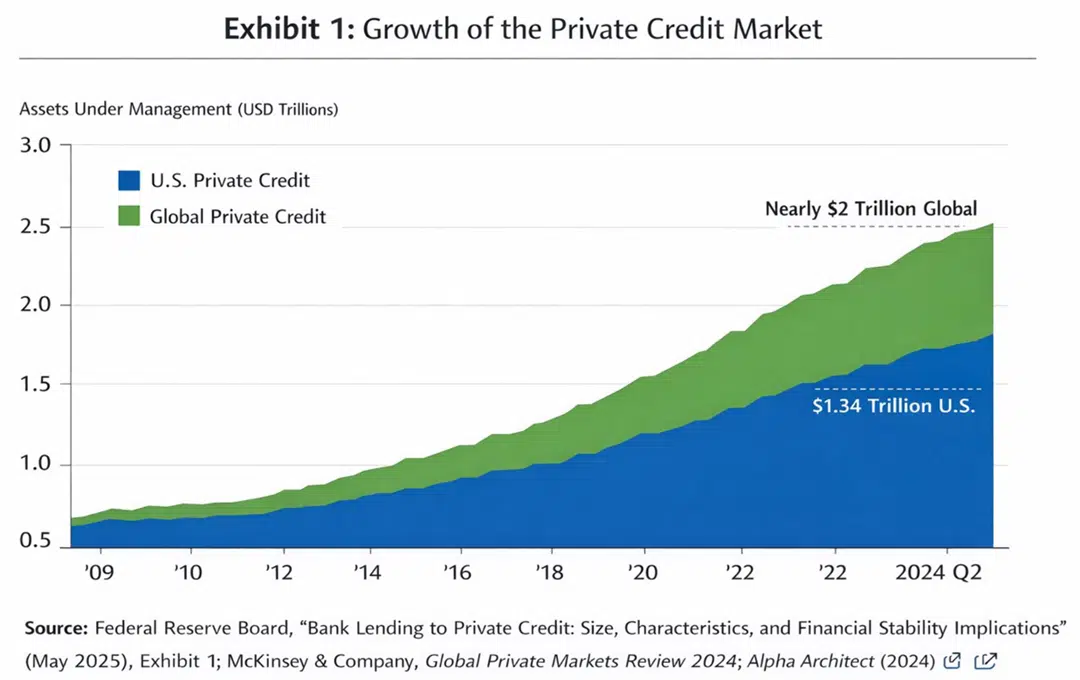

The Wrong Asset, the Wrong Account, the Wrong Moment

On August 7, 2025, the Trump administration signed an executive order titled “Democratizing Access to Alternative Assets for 401(k) Investors,” directing the Department of Labor and the Securities and Exchange Commission to dismantle the regulatory friction that has historically kept private equity, private credit, real estate funds, and similar illiquid alternatives out of the country’s workplace retirement plans.

Take the Moral High-Ground or the Moral High-Ground Will Take You

At the end of March, we published a piece on why the war in Iran could continue longer than expected and another piece on how the consequences of the conflict may be seriously underestimated. Before we dive into the bull-case on energy, the KCR team would like to clarify that the human suffering that may be coming from the war – successful peace deal or not - is front-and-center in our minds.

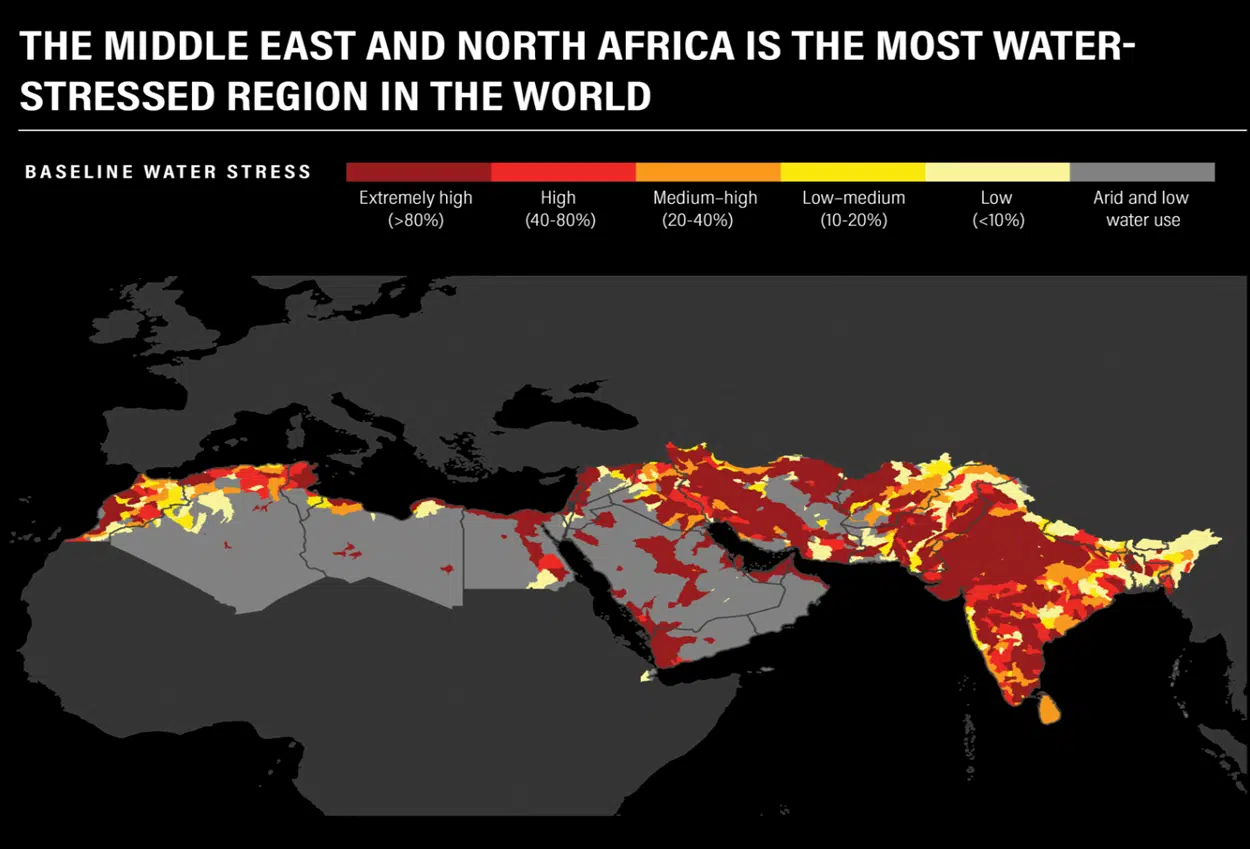

Water, Food, & Fuel: Is the Market Mispricing the War on Iran?

Water Risk from a Prolonged War with Iran Markets have rightly fixated on what the Iran war means for oil and gas flows through the Strait of Hormuz—but in doing so, they have largely ignored a vulnerability that may prove even more destabilizing: the Middle East's near-total dependence on desalinated water.

AN ENDLESS WAR? Why the Conflict in Iran May Not End Soon—And What the Market May be Getting Wrong

Certain of the views expressed in the material below are sourced from center to hard-left-leaning sources. Regardless of what our staff's highly diverse personal views on the war are, we believe that just because some suggesting the conflict may be protracted are left-leaning, does not nullify their thinking from the probability distribution of possible outcomes

Should Retail Investors Head to the Casino?

Leveraged ETFs look like a shortcut: twice (or three times) the action of a stock, in a tidy wrapper you can buy in a brokerage account. The problem—explained plainly in this paper—is that the shortcut is built on a misunderstanding.

Devon Energy Corporation (DVN)

Today’s topic: a large-cap company trading at 11 times earnings, with a ~12% free cash flow yield, and will pay owners a 10% yield in the very near future. Staring at your savings account, stuffed with index funds bloated by supersized tech stocks trading at 30x earnings, one can scarcely believe such discounts exist.