Why Private Equity and Private Credit Have No Place in America’s 401(k) Plans

The Setup

On August 7, 2025, the Trump administration signed an executive order titled “Democratizing Access to Alternative Assets for 401(k) Investors,” directing the Department of Labor and the Securities and Exchange Commission to dismantle the regulatory friction that has historically kept private equity, private credit, real estate funds, and similar illiquid alternatives out of the country’s workplace retirement plans.[1a, 1b] Within days the DOL stripped its previous cautionary language about private equity from public guidance.[2] For an asset-management lobby that had been working this angle for years, the path to the prize was finally clear.[3]

Get our insights direct to your inbox: SUBSCRIBE

The financial stakes are very large. As of year-end 2024, U.S. defined-contribution plans collectively held approximately $12.4 trillion — what the Wall Street Journal candidly described as “a massive pot of gold” for the private-equity business.[4] Private credit, for its part, now sits near $1.7 trillion in total assets, a figure that has more than doubled since 2020.[5] BlackRock’s chief financial officer has already told analysts that the industry will need litigation reform before plan sponsors can comfortably plug private assets into employees’ accounts; meanwhile, Apollo, Blue Owl, Blackstone, and KKR are all building target-date and hybrid retirement-channel products specifically engineered for defined-contribution plans.[6a, 6b]

The pitch is dressed in egalitarian clothes. Why should the wealthy and the institutional clients be the only investors permitted to harvest the alleged premium of private markets?[7a, 7b] Why should the office worker in Cleveland or the tradesperson in Phoenix be denied the asset class that CalPERS and similar large public pensions have been buying for decades?[8] The argument is just plausible enough to slip past anyone not paying close attention.[9]

This paper argues that anyone who is paying close attention should reach the opposite conclusion. The campaign to push private equity and private credit into 401(k)s is not a sudden reawakening to the unmet investment needs of ordinary American workers.[10] It is a supply-side response to an asset class that has outgrown its plausible borrower base, that depends on internal valuations no outside party can verify, that has become entangled with the banking system in ways every major financial-stability regulator has flagged as dangerous, that is quietly stacking on more leverage to defend its yields, and — most damning of all — that has not actually delivered superior returns even for the sophisticated institutional investors who pioneered the strategy.[11] Five charts make the case in detail.

The Supply-Side Squeeze

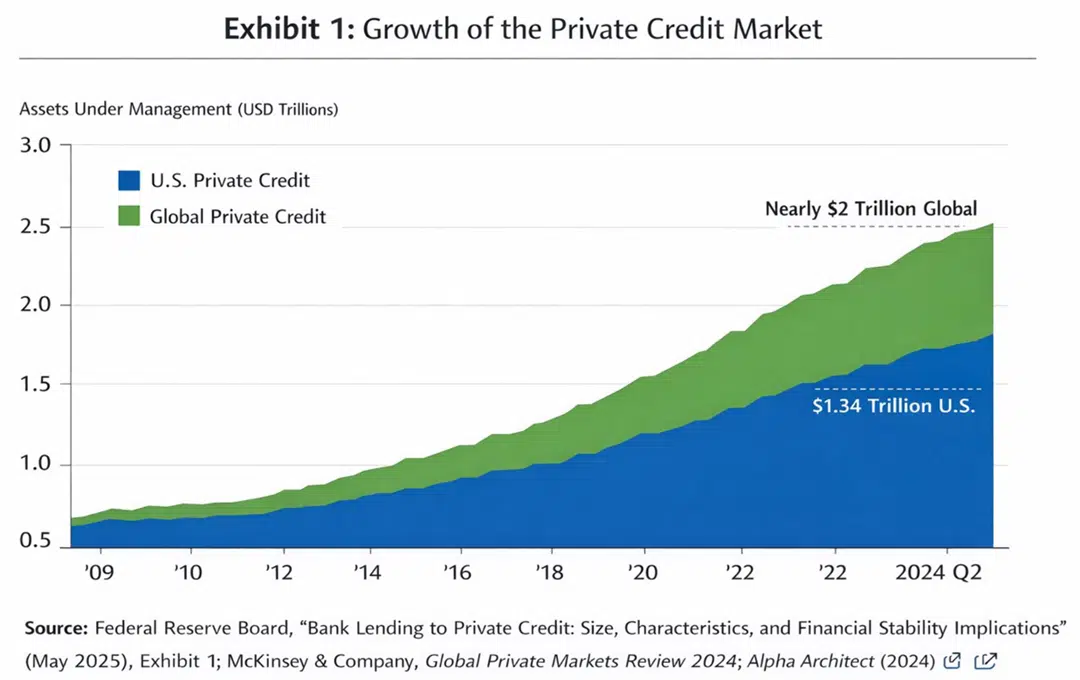

Note: Reconstructed from Federal Reserve Board, “Bank Lending to Private Credit: Size, Characteristics, and Financial Stability Implications” (FEDS Notes, May 2025), Exhibit 1; cross-checked against McKinsey & Company, Global Private Markets Review 2024, and Alpha Architect (2024). U.S. private credit AUM ~$1.34 trillion; global ~$2 trillion; ~5x growth since 2009.

Note: Reconstructed from Federal Reserve Board, “Bank Lending to Private Credit: Size, Characteristics, and Financial Stability Implications” (FEDS Notes, May 2025), Exhibit 1; cross-checked against McKinsey & Company, Global Private Markets Review 2024, and Alpha Architect (2024). U.S. private credit AUM ~$1.34 trillion; global ~$2 trillion; ~5x growth since 2009.

Federal Reserve Board researchers have been tracking private credit’s expansion with the polite alarm that central-bank economists reserve for things they consider dangerous.[12] Their May 2025 FEDS Note documents a U.S. private credit market that reached approximately $1.34 trillion by the second quarter of 2024, with the global market approaching $2 trillion — roughly five times its size in 2009.[13] McKinsey’s Global Private Markets Review independently pegs private debt assets under management at $1.7 trillion as of mid-2023, the highest fundraising and AUM growth of any private asset class that year.[14a] Larry Swedroe, writing for Alpha Architect, characterized the trajectory more bluntly: an asset class that has grown “roughly ten times larger than it was in 2009,” with the pace prompting open speculation about whether a bubble has formed.[14b] For most of the period covered by these studies, private credit was a minor slice of U.S. business credit, dwarfed by the bank commercial-and-industrial loan book and by broadly syndicated lending. Then, in roughly four years after 2019, it tripled.[15]

Asset classes do not triple in four years because the underlying investments have suddenly become better. They triple because money is pouring in faster than the real-economy activity that justifies them, and that money has to find borrowers somewhere.[16] Pensions, endowments, sovereign-wealth funds, and the high-net-worth channel — the traditional buyers of private credit and private equity — have largely reached the asset-allocation ceilings their investment policies allow.[17] The strain is visible from inside those institutions: Allen Waldrop, the private-equity director at Alaska’s $80 billion Permanent Fund, told the Wall Street Journal in mid-2024 that he was watching “more money out and going out than is coming back” from the asset class, and described the resulting cash crunch as a source of considerable industry anxiety.[18]

Wall Street’s solution to running out of institutional buyers is…

Disclaimer

The information, data, analyses, and opinions presented herein (a) do not constitute investment advice, (b) are provided solely for informational purposes and therefore are not, individually or collectively, an offer to buy or sell a security, (c) are not warranted to be correct, complete or accurate, and (d) are subject to change without notice. Kailash Capital Research, LLC and its affiliates (collectively, “KCR”) shall not be responsible for any trading decisions, damages, or other losses resulting from, or related to, the information, data, analyses or opinions or their use. The information herein may not be reproduced or retransmitted in any manner without the prior written consent of KCR. In preparing the information, data, analyses, and opinions presented herein, KCR has obtained data, statistics, and information from sources it believes to be reliable. KCR, however, does not perform an audit or seek independent verification of any of the data, statistics, and information it receives. KCR and its affiliates do not provide tax, legal, or accounting advice. This material has been prepared for informational purposes only and is not intended to provide, and should not be relied on for tax, legal, or accounting advice. You should consult your tax, legal, and accounting advisors before engaging in any transaction.

Nothing herein shall limit or restrict the right of affiliates of KCR to perform investment management or advisory services for any other persons or entities. Furthermore, nothing herein shall limit or restrict affiliates of KCR from buying, selling, or trading securities or other investments for their own accounts or for the accounts of their clients. Affiliates of KCR may at any time have, acquire, increase, decrease, or dispose of the securities or other investments referenced in this publication. KCR shall have no obligation to recommend securities or investments in this publication as a result of its affiliates’ investment activities for their own accounts or for the accounts of their clients.

© 2026 Kailash Capital Research, LLC – All rights reserved.

April 17, 2026 |

| Authors: Matthew Malgari, Nathan Przybylo, Dr. Sanjeev Bhojraj and John Durkin

April 17, 2026

Authors: Matthew Malgari, Nathan Przybylo, Dr. Sanjeev Bhojraj and John Durkin