We believe that Staples stocks’ ability to raise prices is a feature that may be highly valuable in the current environment. We don’t make macro forecasts but have written extensively about inflation, equity duration and how the market has priced in almost no chance of inflation. If the Fed’s forecasts prove wrong, the impact will be dire.

We became constructive on the makers of food products earlier this year. Our January piece Staples & the Power of the Prosaic made the case that companies that make the goods and services you need were at a possible inflection point in terms of valuation and sentiment. Summarily we think euphoria in tech has left some of the most durable, stable, and non-cyclical companies at unusual discounts.

Get our insights direct to your inbox: SUBSCRIBE

Before jumping into how these firms protected against inflation in the 1970s, let’s quickly revisit the basic thesis in a simple chart. The chart below shows that Consumer Staples, as a sector, are cheaper than 67% of large-cap firms today. You can see that sellers of packaged foods and other boring basics were cheaper than 73% of all large-cap companies at the peak of the internet mania.

That makes sense intuitively. Swept up in the dot.com mania, investors abandoned the boring, slow-growing but highly profitable and, frequently, income-producing staples sectors. And they did so at precisely the moment when such attributes would prove to be most valuable.

While not as cheap as they were in 2000, we believe it is a good time to be researching and being opportunistic in buying these stable firms.

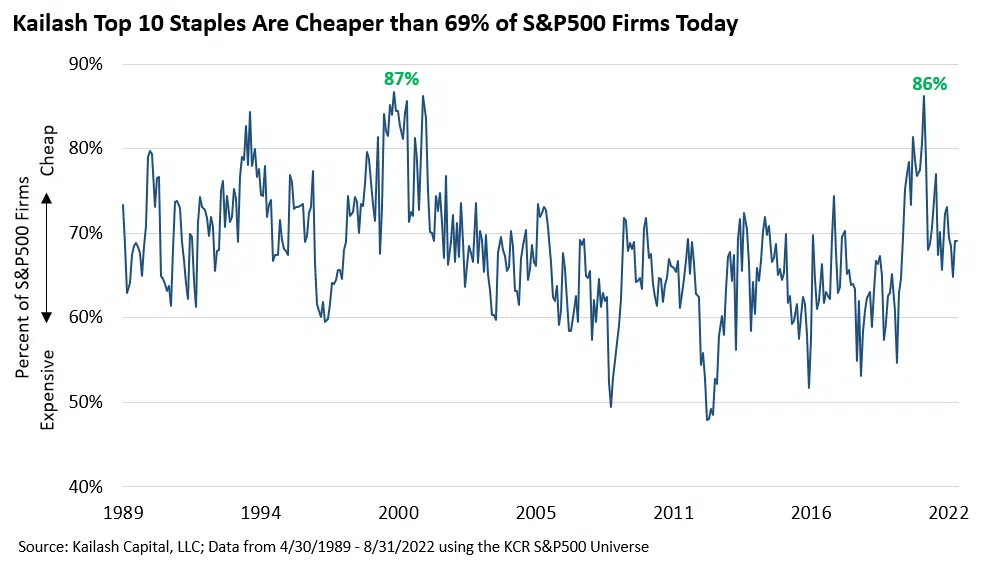

This next chart shows the same data for our ranking model’s top 10 best stocks. The chart is stunning. Our top 10 ranked firms are exactly as cheap today as our top 10 were in 2000. These picks also tend to offer very low equity duration – a valuable trait in our view.

As longtime subscribers know, our ranking models can easily be sorted by sector. The chart below is the same as the prior one. The only difference is it uses our top 10 ranked staples stocks. Our favorite staples stocks are cheaper than 86% of all the stocks in our Large Cap Universe.

Disclaimer

The information, data, analyses, and opinions presented herein (a) do not constitute investment advice, (b) are provided solely for informational purposes and therefore are not, individually or collectively, an offer to buy or sell a security, (c) are not warranted to be correct, complete or accurate, and (d) are subject to change without notice. Kailash Capital Research, LLC and its affiliates (collectively, “Kailash Capital Research, LLC ”) shall not be responsible for any trading decisions, damages or other losses resulting from, or related to, the information, data, analyses or opinions or their use. The information herein may not be reproduced or retransmitted in any manner without the prior written consent of Kailash Capital Research, LLC . In preparing the information, data, analyses, and opinions presented herein, Kailash Capital Research, LLC has obtained data, statistics, and information from sources it believes to be reliable. Kailash Capital Research, LLC , however, does not perform an audit or seeks independent verification of any of the data, statistics, and information it receives. Kailash Capital Research, LLC and its affiliates do not provide tax, legal, or accounting advice. This material has been prepared for informational purposes only and is not intended to provide, and should not be relied on for tax, legal, or accounting advice. You should consult your tax, legal, and accounting advisors before engaging in any transaction. © 2021 Kailash Capital Research, LLC – All rights reserved.

Nothing herein shall limit or restrict the right of affiliates of Kailash Capital Research, LLC to perform investment management or advisory services for any other persons or entities. Furthermore, nothing herein shall limit or restrict affiliates of Kailash Capital Research, LLC from buying, selling or trading securities or other investments for their own accounts or for the accounts of their clients. Affiliates of Kailash Capital Research, LLC may at any time have, acquire, increase, decrease or dispose of the securities or other investments referenced in this publication. Kailash Capital Research, LLC shall have no obligation to recommend securities or investments in this publication as result of its affiliates’ investment activities for their own accounts or for the accounts of their clients.