Tap Dancing with TINA & a Moment to Remember in US Monetary Policy

Macro Investing: The Rising Pressure of a Decade of Fiscal Profligacy

KCR’s investment process does not use macro inputs or engage in macro trading. We use historical security-level data around valuation, profitability, quality, and other metrics to identify opportunities for short sellers and long investors alike. Macro investing can be a challenging endeavor.

A great example is the enormous bailout of Wall Street used to end the Great Financial Crisis. Many people thought a brutal bout of inflation was inevitable. Instead, the world proceeded to borrow and spend ever larger sums. And the more governments borrowed and spent, the lower interest rates fell.

Get our insights direct to your inbox: SUBSCRIBE

A piece by the always-wonderful John Authers explained how the recent tax cuts in the UK detonated a Lehman-like crisis in gilts. His walk-through of the stunning -24% collapse and subsequent rally of the 30-year British bond was a terrific reminder of how the big picture doesn’t matter until it is all that matters.

This piece is not designed to wow macro investors or macro hedge funds. KCR was simply stunned at our own complacency on what is, ultimately, a very basic issue. The world has gone from pillorying the Fed for keeping rates too low to screaming bloody murder for taking them to 3.25%. In many ways, the agonies a meager 3.25% have caused global markets is a testament to the enormous leverage and fragility of our financial system.

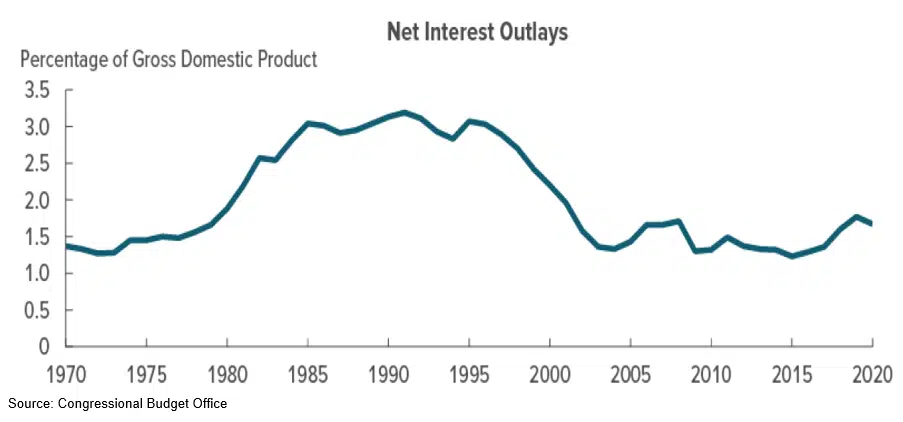

We also believe the very simple analysis below is at the heart of why the Fed must shatter inflation.

Disclaimer

The information, data, analyses, and opinions presented herein (a) do not constitute investment advice, (b) are provided solely for informational purposes and therefore are not, individually or collectively, an offer to buy or sell a security, (c) are not warranted to be correct, complete or accurate, and (d) are subject to change without notice. Kailash Capital Research, LLC and its affiliates (collectively, “Kailash Capital Research, LLC ”) shall not be responsible for any trading decisions, damages or other losses resulting from, or related to, the information, data, analyses or opinions or their use. The information herein may not be reproduced or retransmitted in any manner without the prior written consent of Kailash Capital Research, LLC . In preparing the information, data, analyses, and opinions presented herein, Kailash Capital Research, LLC has obtained data, statistics, and information from sources it believes to be reliable. Kailash Capital Research, LLC , however, does not perform an audit or seeks independent verification of any of the data, statistics, and information it receives. Kailash Capital Research, LLC and its affiliates do not provide tax, legal, or accounting advice. This material has been prepared for informational purposes only and is not intended to provide, and should not be relied on for tax, legal, or accounting advice. You should consult your tax, legal, and accounting advisors before engaging in any transaction. © 2021 Kailash Capital Research, LLC – All rights reserved.

Nothing herein shall limit or restrict the right of affiliates of Kailash Capital Research, LLC to perform investment management or advisory services for any other persons or entities. Furthermore, nothing herein shall limit or restrict affiliates of Kailash Capital Research, LLC from buying, selling or trading securities or other investments for their own accounts or for the accounts of their clients. Affiliates of Kailash Capital Research, LLC may at any time have, acquire, increase, decrease or dispose of the securities or other investments referenced in this publication. Kailash Capital Research, LLC shall have no obligation to recommend securities or investments in this publication as result of its affiliates’ investment activities for their own accounts or for the accounts of their clients.