Your author’s 11 year-old, like many her age, has become not just a purveyor of various games on Roblox but has also written code for two games. She and her younger sister watched with grave disapproval as their father managed to suffer calamitous, early, and presumably avoidable deaths attempting to navigate the hellish obstacle courses she had designed. Looking to redeem my daughters’ perceived confidence in me, I made the catastrophic decision to show her the “game daddy plays all day in his office.”

Having secured her an app with stock prices, given her a brief primary on how stocks are not just slips of paper but also interests in real companies, her stock-picking began[1]. “This is easy dad,” she quipped on a recent Friday. Her method is to find the stocks at the top of the list with green arrows….and pencil them down as picks. If they go down a few days in a row, she sells them. Her results rival the best managers of our time. In this age of “helicopter parenting,” where parents often herald the success of children, I share this story to show my intellectual honesty: my 11-year-old will be wrong!

Get our insights direct to your inbox: SUBSCRIBE

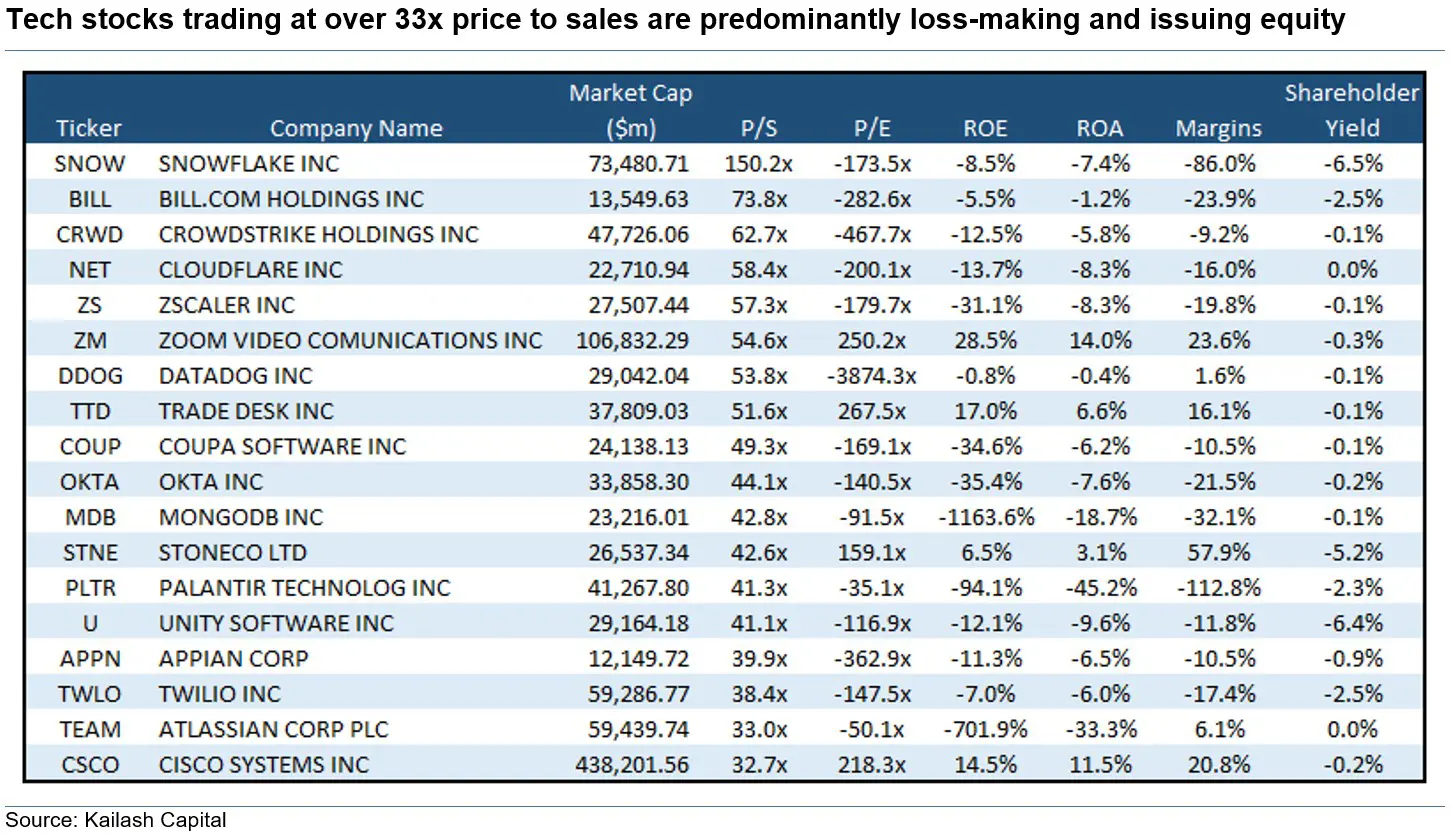

Many of us here at Kailash sport gray hair and have proven ourselves no match for the rip-roaring rise of tech-heavy index funds to even more concentrated specialty ETFs. While “growth” and “value” have traded blows for the majority of the post-2010 period, Kailash has documented, in Fig. 2 of this paper and Fig. 1 of this paper, that the ballistic rise of many highly speculative firms, such as clean technology stocks, occurred in the years since 2017. Today Kailash believes market participants are standing on a dangerous precipice. Below we have provided a list and some simple salient fundamentals of all the Tech stocks trading over 33x Price to Sales. Why 33x? More on that in a moment.

The list is ordered from most to least expensive. These firms trade at utterly ghastly multiples. Even more remarkable is that excluding three firms, every one of these companies loses money and is issuing stock (negative shareholder yield) to fill the hole!

Get our White Papers direct to your inbox: SUBSCRIBE

Why 33x Sales?

As documented in our historically informed brief on the catastrophic folly of investing in companies trading at 10x price to sales, massive multiples like this are a recipe for disaster. Kailash decided to jump to 33x sales after reading a brief but brilliant missive[2] by Jamie Powell in the Financial Times riffing off Keubiko[3]. In it, he documents Cisco’s meteoric 236% rise into the peak of the internet bubble “…backed by a crazed-enthusiasm for the technological shifts brought about by the internet. The Thesis was solid: as a provider of networking equipment for both telecom players and other businesses, Cisco was the shovel-seller in a dot com gold rush. What could go wrong?”

You may not have noticed but the last name on the list above was CISCO – and the fundamentals and valuations were as of MARCH 2000. The list above is merely “all the tech stocks that are MORE expensive than 2000 at its peak.” Look at the list again. What is remarkable is that Cisco is the CHEAPEST of that group, and it also had the second-best margins in the group. Compared to Cisco, the rest of the stocks listed above have the fundamental optics of a burning dumpster fire.

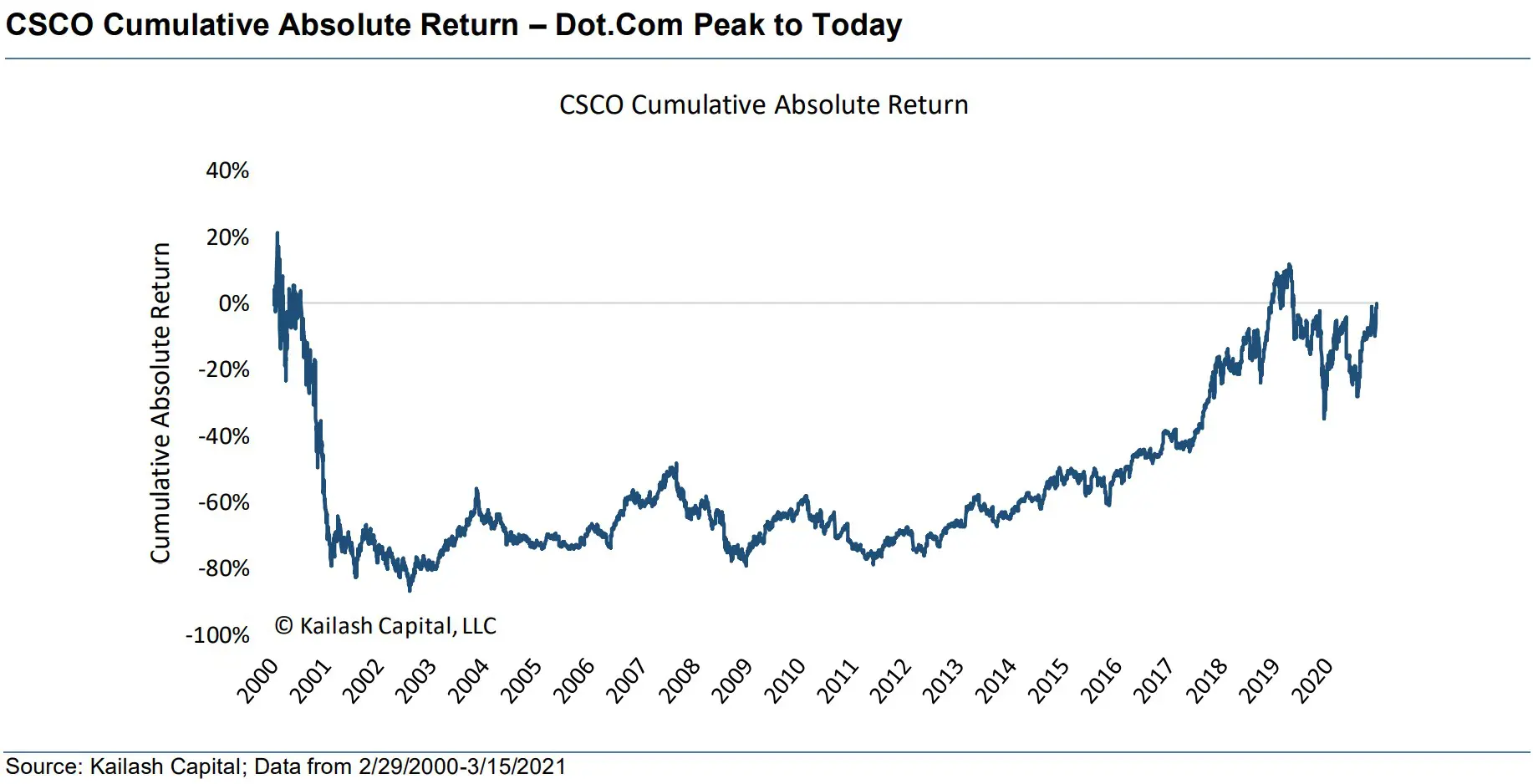

With hindsight, investors’ faith in the company’s fundamental prospects proved to be well placed. As documented by Powell, over the ensuing 21 years, Cisco would see its profits quintupled and the company averaging a 17% ROE. Similar to our analog between Carvana today and Akami in 1999, even if you had perfect foresight to know that Cisco would be a massive growth compounding engine, investing in the stock was a disaster. After suffering an -80% decline, you had to hang on for 21 years to get your money back.

Kailash urges investors to contemplate the brutal and unforgiving arithmetic lesson in the charts above.

EVEN WITH PERFECT FORESIGHT, IF YOU PAY TOO MUCH, YOUR RETURNS CAN BE HORRIBLE.

Disclaimer

The information, data, analyses, and opinions presented herein (a) do not constitute investment advice, (b) are provided solely for informational purposes and therefore are not, individually or collectively, an offer to buy or sell a security, (c) are not warranted to be correct, complete or accurate, and (d) are subject to change without notice. Kailash Capital Research, LLC and its affiliates (collectively, “Kailash Capital Research, LLC ”) shall not be responsible for any trading decisions, damages or other losses resulting from, or related to, the information, data, analyses or opinions or their use. The information herein may not be reproduced or retransmitted in any manner without the prior written consent of Kailash Capital Research, LLC . In preparing the information, data, analyses, and opinions presented herein, Kailash Capital Research, LLC has obtained data, statistics, and information from sources it believes to be reliable. Kailash Capital Research, LLC , however, does not perform an audit or seeks independent verification of any of the data, statistics, and information it receives. Kailash Capital Research, LLC and its affiliates do not provide tax, legal, or accounting advice. This material has been prepared for informational purposes only and is not intended to provide, and should not be relied on for tax, legal, or accounting advice. You should consult your tax, legal, and accounting advisors before engaging in any transaction. © 2021 Kailash Capital Research, LLC – All rights reserved.

Nothing herein shall limit or restrict the right of affiliates of Kailash Capital Research, LLC to perform investment management or advisory services for any other persons or entities. Furthermore, nothing herein shall limit or restrict affiliates of Kailash Capital Research, LLC from buying, selling or trading securities or other investments for their own accounts or for the accounts of their clients. Affiliates of Kailash Capital Research, LLC may at any time have, acquire, increase, decrease or dispose of the securities or other investments referenced in this publication. Kailash Capital Research, LLC shall have no obligation to recommend securities or investments in this publication as result of its affiliates’ investment activities for their own accounts or for the accounts of their clients.