The Combustible Mix of Low Quality & High Expectations

Introduction:

On Friday, our research team published a Charts For the Curious that triggered a good deal of feedback. The chart made it clear that firms with the highest future expectations from Wall Street have performed better than any time since the dot.com bubble. This is a topic we are very familiar with and have written about for a decade. A mania for stocks that grow fast has, once again, broken out.

In 2012 our research team penned The Siren Song of Growth explaining why people “reach for the stars.” In our later piece, The Persistence of Profits, we document that growing at high rates for long periods of time is impossible. We followed that up with numerous other pieces of research around quality investing and deep dive research on GARP investing, among other topics, demonstrating that capitalism is pretty effective. Over time competition takes its toll.

Get our insights direct to your inbox: SUBSCRIBE

A Difficult Investment Strategy:

In this Quick Take we focus on what we believe are the lowest quality speculative investments in the group of companies with the highest expectations. The chart below shows the returns to:

- The 10% of stocks with the highest expectations from Wall Street and…

- …are also in the bottom 20% of the scores from our Large Cap and Small & Midcap screening tools

These companies have the highest expectations and the least financial resources to meet them!

History suggests there may be a very high price to be paid by those who apply a buy and hold strategy to such a collection of stocks! Maybe you have the short term trading skills to time them but that requires a high risk tolerance. Investors seeking a growth stock like these may find themselves suddenly holding penny stocks. As we will show below many of these firms many not be good long term investments!

Higher Returns from These Firms May Prove Misleading:

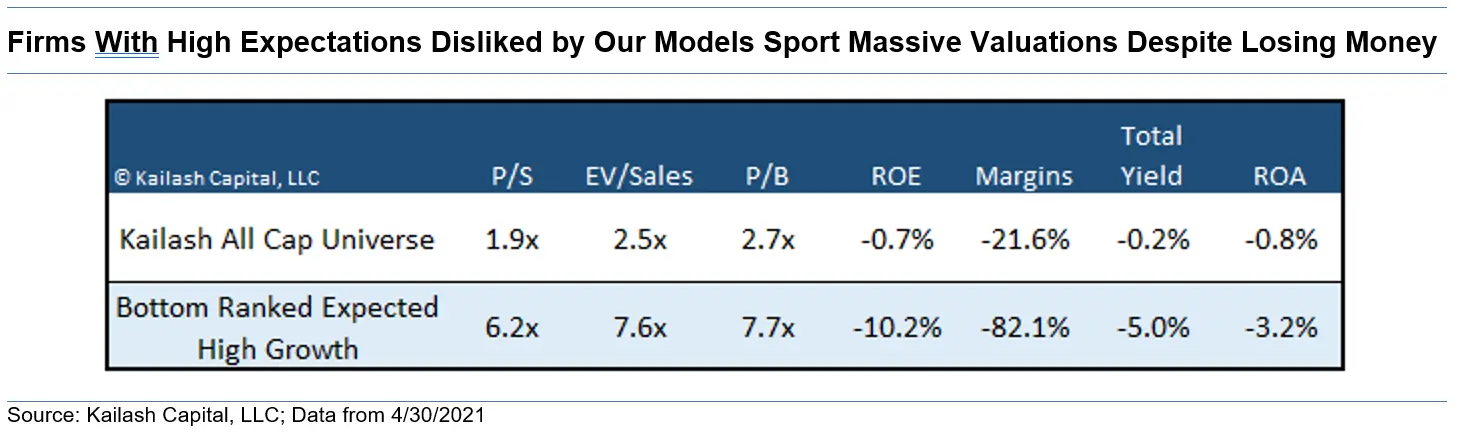

The exhibit below shows the fundamental traits of Kailash’s proprietary All-Cap universe in the first row. The second row are those firms that have the highest expected long term growth that also fall into the bottom of our equity screening tools. The contrast is astonishing.

The stock market as defined by our All Cap Universe trades at only 1.9x price to sales (P/S). Compare that to the firms with the highest expectations, that our ranking tools dislike in the second row which trade at 6.2x sales – a terrifying multiple.

Keep moving from left to right and the data is unforgiving. Look at the ROE of the firms with the highest expectations our model dislikes. Negative -10.2%. We omitted price to earnings in the table because the losses generated by these high expectation firms was so bad the number simply did not make sense.

The column “Total Yield” shows the amount of dividends added to share repurchases (issuance). A negative number means that firms are diluting owners by issuing lots of stock. Incredibly, the firms with the highest expected growth, those that have to achieve the most in order to keep investors happy, are charging investors 5% a year to own them. The number is plain in its meaning – these firms cannot fund their operations without constantly selling stock.

In our view this looks more like speculation than growth investing.

We believe the following can be said about stocks that have the highest expectations and are disliked by our models:

- They are dangerously valued based on historical precedent

- They lose money at an alarming rate

- They are charging people who invest in their stocks for the right to own them

Our team believes this is a recipe for disaster. Before you look at the names, would you disagree?

Our research team has written extensively about the degree of the mania underway today. In some of our other Charts for the Curious and Quick Takes, we have noted the abuses in stock compensation, the systematic overvaluation apparent in certain stocks, the collapse in the reliability of widely accepted risk metrics and the explosion in valuation ascribed to companies that lose money.

Our team of professionals has also done much more detailed research on where today’s bubble is concentrated. This research can be found in our pieces around growth and value, the Nifty-Fifty mania today, and the risk to trying to time markets in periods like today. We have also brought compelling evidence to the “other side of the coin.” For those willing to avoid the herd, hew to common sense and invest in profitable firms at reasonable to cheap prices we believe there are terrific opportunities in high quality midcaps, small caps and staples.

Please find below a list of the firms with the highest expectations that score in the bottom of our S&P 500 and Small & Midcap ranking models. We believe the firms below have the highest probability of disappointing investors.

Disclaimer

The information, data, analyses, and opinions presented herein (a) do not constitute investment advice, (b) are provided solely for informational purposes and therefore are not, individually or collectively, an offer to buy or sell a security, (c) are not warranted to be correct, complete or accurate, and (d) are subject to change without notice. Kailash Capital Research, LLC and its affiliates (collectively, “Kailash Capital Research, LLC ”) shall not be responsible for any trading decisions, damages or other losses resulting from, or related to, the information, data, analyses or opinions or their use. The information herein may not be reproduced or retransmitted in any manner without the prior written consent of Kailash Capital Research, LLC . In preparing the information, data, analyses, and opinions presented herein, Kailash Capital Research, LLC has obtained data, statistics, and information from sources it believes to be reliable. Kailash Capital Research, LLC , however, does not perform an audit or seeks independent verification of any of the data, statistics, and information it receives. Kailash Capital Research, LLC and its affiliates do not provide tax, legal, or accounting advice. This material has been prepared for informational purposes only and is not intended to provide, and should not be relied on for tax, legal, or accounting advice. You should consult your tax, legal, and accounting advisors before engaging in any transaction. © 2021 Kailash Capital Research, LLC – All rights reserved.

Nothing herein shall limit or restrict the right of affiliates of Kailash Capital Research, LLC to perform investment management or advisory services for any other persons or entities. Furthermore, nothing herein shall limit or restrict affiliates of Kailash Capital Research, LLC from buying, selling or trading securities or other investments for their own accounts or for the accounts of their clients. Affiliates of Kailash Capital Research, LLC may at any time have, acquire, increase, decrease or dispose of the securities or other investments referenced in this publication. Kailash Capital Research, LLC shall have no obligation to recommend securities or investments in this publication as result of its affiliates’ investment activities for their own accounts or for the accounts of their clients.