Introduction:

This paper builds on our recent work highlighting that many of the market’s highest quality firms are trading at discounts to the broad market. The exhibits that follow provide potent evidence that today is one of the most compelling times in history to adopt a simple dividend investing strategy in Consumer Staples. Specifically:

- Tech Investing: The recent mania for loss-making tech firms, speculative investments and impossibly priced “Nifty Fifty” stocks has inhaled capital and left many of the most proven and profitable firms at historic discounts

- Staples – An Income Investing Strategy: The yield famine in markets today combined with the historical power of investing in Consumer Staples creates a compelling opportunity to buy the market’s best assets

- Trading Places: Why today is a terrific time to start selling out of overpriced tech and buying into Staples

This newsletter has not been afraid to suggest that the market is deep in the grip of a mania similar to the one seen at the peak of the Nifty Fifty and the Internet Bubble of 2000. As the cadence of those papers has increased, so have those dedicated to exploiting an increasingly wide array of superb investment opportunities in some of the best companies. Before adding to our expanding series advocating for long-tenured, profitable, growing, and dividend-paying firms trading at reasonable prices, we think it is worth reminding readers of the severity of today’s pricing dichotomy.

Get our White Papers direct to your inbox: SUBSCRIBE

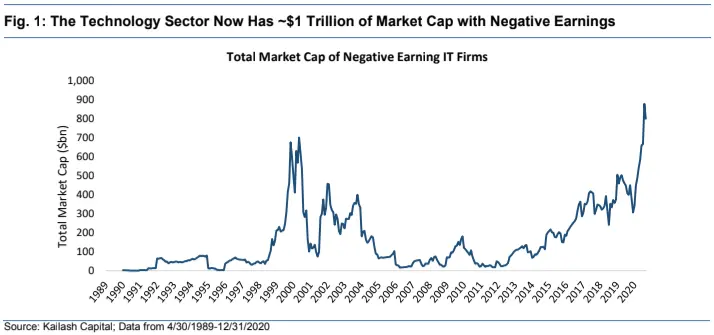

Aside from the obvious arithmetic headwinds facing today’s Nifty Fifty, the next major problem can be seen in Figure 1 below. This is the market cap of Large Cap IT firms losing money. Approaching a trillion dollars, the losers are now worth ~30% more than the same group was at the peak of the internet bubble. In a rare breach of policy, Kailash will make a forecast: we doubt the tech IPO pipeline is brimming with profitable tech and cleantech stocks. The situation will only deteriorate as Wall Street does its job filling demand for neat tech stocks lack credible and self-funding business models.

As Kailash explained in How to Build a Growth Stock, even if all these firms owned a proprietary and critical new technology like a few firms in 1999 did, paying obscene multiples for money losers is still a mugs game. While the post-2000 losses in the IT high-flyers were horrendous, that bubble built the internet and transformed society and the world. Figure 1 strikes us as fearsome evidence that speculators are chasing the “shiny objects” in tech ever higher, and participants in the frenzy would be wise in reducing exposure.

KCR would also like to highlight our research on what we believe are some of the best opportunities we have seen in GARP stocks for those looking to find mispriced growth stocks.

Disclaimer

The information, data, analyses, and opinions presented herein (a) do not constitute investment advice, (b) are provided solely for informational purposes and therefore are not, individually or collectively, an offer to buy or sell a security, (c) are not warranted to be correct, complete or accurate, and (d) are subject to change without notice. Kailash Capital Research, LLC and its affiliates (collectively, “Kailash Capital Research, LLC ”) shall not be responsible for any trading decisions, damages or other losses resulting from, or related to, the information, data, analyses or opinions or their use. The information herein may not be reproduced or retransmitted in any manner without the prior written consent of Kailash Capital Research, LLC . In preparing the information, data, analyses, and opinions presented herein, Kailash Capital Research, LLC has obtained data, statistics, and information from sources it believes to be reliable. Kailash Capital Research, LLC , however, does not perform an audit or seeks independent verification of any of the data, statistics, and information it receives. Kailash Capital Research, LLC and its affiliates do not provide tax, legal, or accounting advice. This material has been prepared for informational purposes only and is not intended to provide, and should not be relied on for tax, legal, or accounting advice. You should consult your tax, legal, and accounting advisors before engaging in any transaction. © 2021 Kailash Capital Research, LLC – All rights reserved.

Nothing herein shall limit or restrict the right of affiliates of Kailash Capital Research, LLC to perform investment management or advisory services for any other persons or entities. Furthermore, nothing herein shall limit or restrict affiliates of Kailash Capital Research, LLC from buying, selling or trading securities or other investments for their own accounts or for the accounts of their clients. Affiliates of Kailash Capital Research, LLC may at any time have, acquire, increase, decrease or dispose of the securities or other investments referenced in this publication. Kailash Capital Research, LLC shall have no obligation to recommend securities or investments in this publication as result of its affiliates’ investment activities for their own accounts or for the accounts of their clients.

January 7, 2021 |

| Authors: Matthew Malgari, Nathan Przybylo, Dr. Sanjeev Bhojraj and John Durkin

January 7, 2021

Authors: Matthew Malgari, Nathan Przybylo, Dr. Sanjeev Bhojraj and John Durkin