• Introduction: Never Has So Much Value Been Ascribed to Such Losses

• The Simplicity of Price-to-Sales Tells the Same Story

• Unforgiving Fundamentals

• Conclusions

• Exhibit

Introduction: Never Has So Much Value Been Ascribed to Such Losses

Kailash’s most recent paper “S&P500 vs. R2500: Will the Herding Continue?” detailed the record valuation spreads between the S&P500 and R2500 and the Kailash’s picks within the Small & Mid Cap universe. Kailash suggested the below action items in the conclusion as a means to exploit the anomaly. This paper seeks to emphasize in a simple way why an actively managed product might prove a better option than purchasing a Small & Mid Cap index fund.

1. Buy actively managed Small & Mid Cap Products

2. Buy a Small & Mid Cap Index Fund

3. Buy the Kailash SMID Top 25 Picks

4. Buy All-Cap Index Funds which may benefit from the rise of smaller firms

5. Purchase long/short products in large cap that can short the most overvalued firms since 2000

Get our White Papers direct to your inbox: SUBSCRIBE

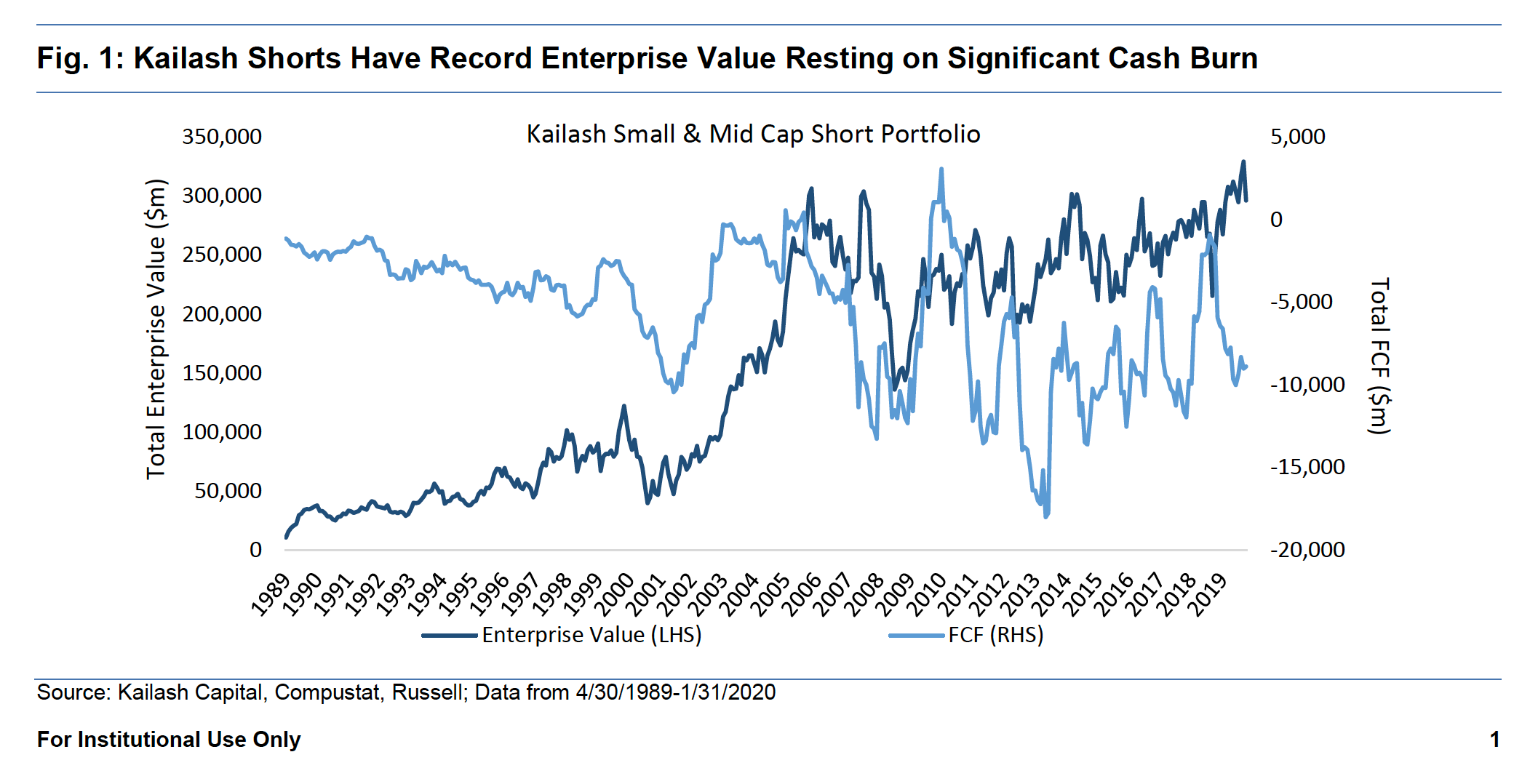

Figure 1 below presents the Kailash Small & Mid Cap Short portfolio’s aggregate historical Enterprise Value (EV) and Free Cash Flow (FCF). Negative numbers are a funny item for analysts. If two companies lose $100 but one has an EV of $1,000 and the other an EV of $2,000, the FCF/EV is -10% and -5% respectively. One could suggest that the $2,000 firm is “less” expensive than the $1,000 firm because the market has told us it is worth twice as much and the market is efficient. Or, in your author’s view, the second firm is 100% more expensive – if two firms lose the same amount of money, the one with the higher enterprise value is just pricing in more promises! The data below shows that never in history has such an immense amount of EV rested on such a large amount of losses in our short portfolio. Our SMID short book has essentially pooled a group of companies that, combined, are worth $300bn dollars and lose $10bn.

Disclaimer

The information, data, analyses, and opinions presented herein (a) do not constitute investment advice, (b) are provided solely for informational purposes and therefore are not, individually or collectively, an offer to buy or sell a security, (c) are not warranted to be correct, complete or accurate, and (d) are subject to change without notice. Kailash Capital Research, LLC and its affiliates (collectively, “Kailash Capital Research, LLC ”) shall not be responsible for any trading decisions, damages or other losses resulting from, or related to, the information, data, analyses or opinions or their use. The information herein may not be reproduced or retransmitted in any manner without the prior written consent of Kailash Capital Research, LLC . In preparing the information, data, analyses, and opinions presented herein, Kailash Capital Research, LLC has obtained data, statistics, and information from sources it believes to be reliable. Kailash Capital Research, LLC , however, does not perform an audit or seeks independent verification of any of the data, statistics, and information it receives. Kailash Capital Research, LLC and its affiliates do not provide tax, legal, or accounting advice. This material has been prepared for informational purposes only and is not intended to provide, and should not be relied on for tax, legal, or accounting advice. You should consult your tax, legal, and accounting advisors before engaging in any transaction. © 2021 Kailash Capital Research, LLC – All rights reserved.

Nothing herein shall limit or restrict the right of affiliates of Kailash Capital Research, LLC to perform investment management or advisory services for any other persons or entities. Furthermore, nothing herein shall limit or restrict affiliates of Kailash Capital Research, LLC from buying, selling or trading securities or other investments for their own accounts or for the accounts of their clients. Affiliates of Kailash Capital Research, LLC may at any time have, acquire, increase, decrease or dispose of the securities or other investments referenced in this publication. Kailash Capital Research, LLC shall have no obligation to recommend securities or investments in this publication as result of its affiliates’ investment activities for their own accounts or for the accounts of their clients.

February 16, 2020 |

| Authors: Matthew Malgari, Nathan Przybylo, Dr. Sanjeev Bhojraj and John Durkin

February 16, 2020

Authors: Matthew Malgari, Nathan Przybylo, Dr. Sanjeev Bhojraj and John Durkin