Low Yields are Now the Norm

KCR recently came across a fabulous tweet by @charliebilello that caught our attention. In his tweet, he pointed out that the dividend yield of the S&P500 was at its lowest point since the stock market bubble of 2000. With the treasury bond market offering so little in interest rates, it begs the question: Is there anywhere to find yield today?

Get our insights direct to your inbox: SUBSCRIBE

In his 2020 letter to shareholders, Buffett stated, “Fixed-income investors worldwide – whether pension funds, insurance companies or retirees – face a bleak future.” We quote him extensively in our piece examining the inflation of the 1970s and believe the charts below tell the story with brutal clarity.

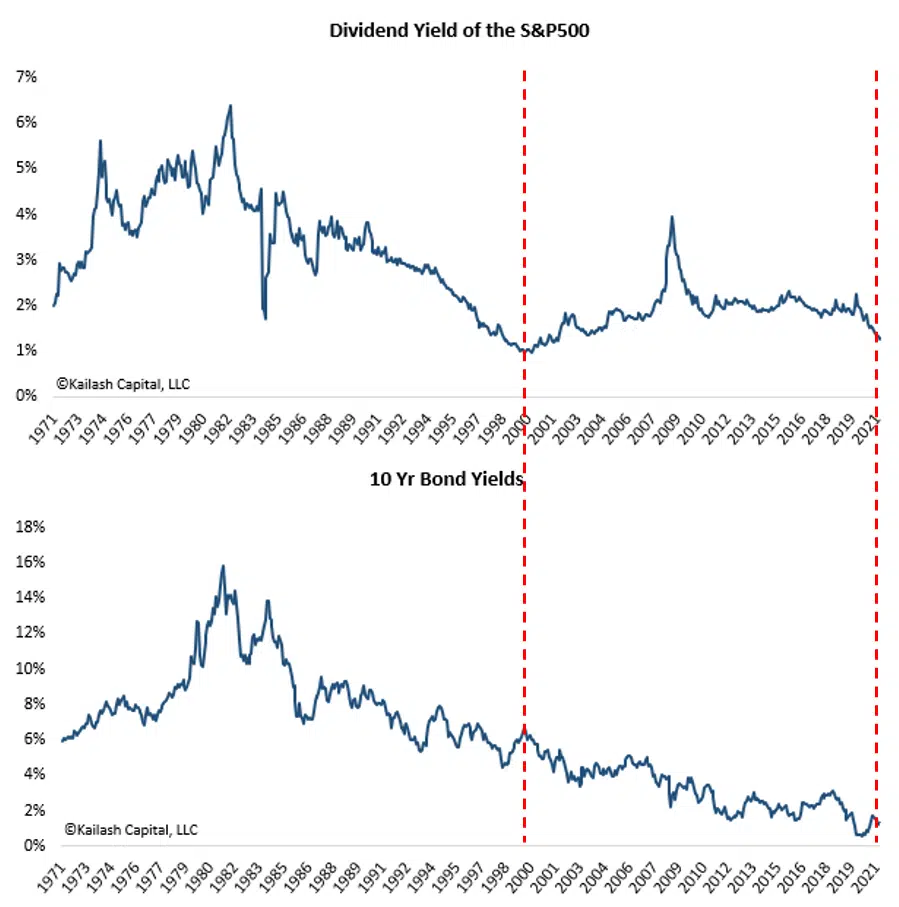

The S&P500’s dividend yield is approaching the lowest level in over 40 years.

Unfortunately, yield-starved investors seeking income securities have few alternatives for their savings accounts.

Here is the nominal yield on 10 Year US Treasury Bonds.

In the dot.com bubble, you could buy risk-free 10 year Treasury Bonds with ~7% interest payments.

Today, those same bonds offer virtually no return in exchange for record duration risk. As we explained, this issue is magnified due to stocks with record equity duration.

Market Bubbles In Years Past Offered High Real Yields, Unlike Today

A recent article from MarketWatch noted that “…the $1 trillion that has flowed to global stocks in 2021 is bigger than the last 20 years combined” – we’ve posted the stunning image below.[1] We believe this is the apogee of behavioral errors that plague investors’ returns.[2]

These record inflows are happening at stock prices that started at the 2000 dot.com peak valuations. These flows have driven equities to multiples never before seen.

For a quick rundown on the power of the Buffett Valuation metric, see our work here, here, and here.

Useless for timing, valuation does, however, flag investors to the risks of paying too much.

The cost of “buying high” in 2000 and 2007 served up terrible losses for investors as the market swung from greed to fear.

We can only guess what they will be whenever the next correction comes.

The chart to the left is the real return on 10 Year US Treasury bonds today.

In the face of record debt, soaring food inflation, record low high-yield spreads, and interest rate risk, you are paying to lend money to the US Government. For a decade.

We offered some possible solutions to the income drought here, here, here, and here among other pieces in our Quick Takes and White Papers. While we believe these are some of the best available solutions, by no means are they a panacea.

With coupon payments on fixed income securities of all types of fixed income low, investors are yield chasing. With elevated credit risks[3], we believe today is the single most challenging investment environment in history as bond mutual funds, corporate bonds, and municipal bonds offer so little in the way of income.

These dismal bond yields have investors chasing returns in the most expensive equity market in history that also offers all-time low dividend yields.

The timing could not be worse. With over 10,000 Americans turning 65 every day, we are reminded of hearing legendary Value Investor Jean-Marie Eveillard quip, “Life’s bills do not come at market tops.” We believe these are times for avoiding the behavioral errors that have plagued investor returns where people crowd in at the highs and panic out at the lows.

If you would like some of the academic literature from Behavioral Finance that infuses all our work, please reach out. For the sake of simplicity, please find some terrific pieces by Capital Group, The Financial Times, Forbes, and Russell Investments if you are interested in the steep costs of our emotions.

Today’s market has become enamored with the prospects for economic growth in sectors that are often speculative. The KCR research team has generated a body of research showing that some of the best inflation hedges happen also to be some of the most reasonably priced and stable investments based on history.

We understand there is a compulsive desire to chase markets. Legendary investors and academics alike have documented this effect. Today, surveys show that investors expect returns to be 17.5% above inflation in the years ahead. We have not seen expectations this high since 2000. When you are thinking about where to invest, we encourage working closely with your financial advisor as these markets are, by nearly every metric, as precarious as any in our lifetimes.

Image from MarketWatch Article on Investor Flows into Stocks:

Disclaimer

The information, data, analyses, and opinions presented herein (a) do not constitute investment advice, (b) are provided solely for informational purposes and therefore are not, individually or collectively, an offer to buy or sell a security, (c) are not warranted to be correct, complete or accurate, and (d) are subject to change without notice. Kailash Capital Research, LLC and its affiliates (collectively, “Kailash Capital Research, LLC ”) shall not be responsible for any trading decisions, damages or other losses resulting from, or related to, the information, data, analyses or opinions or their use. The information herein may not be reproduced or retransmitted in any manner without the prior written consent of Kailash Capital Research, LLC . In preparing the information, data, analyses, and opinions presented herein, Kailash Capital Research, LLC has obtained data, statistics, and information from sources it believes to be reliable. Kailash Capital Research, LLC , however, does not perform an audit or seeks independent verification of any of the data, statistics, and information it receives. Kailash Capital Research, LLC and its affiliates do not provide tax, legal, or accounting advice. This material has been prepared for informational purposes only and is not intended to provide, and should not be relied on for tax, legal, or accounting advice. You should consult your tax, legal, and accounting advisors before engaging in any transaction. © 2021 Kailash Capital Research, LLC – All rights reserved.

Nothing herein shall limit or restrict the right of affiliates of Kailash Capital Research, LLC to perform investment management or advisory services for any other persons or entities. Furthermore, nothing herein shall limit or restrict affiliates of Kailash Capital Research, LLC from buying, selling or trading securities or other investments for their own accounts or for the accounts of their clients. Affiliates of Kailash Capital Research, LLC may at any time have, acquire, increase, decrease or dispose of the securities or other investments referenced in this publication. Kailash Capital Research, LLC shall have no obligation to recommend securities or investments in this publication as result of its affiliates’ investment activities for their own accounts or for the accounts of their clients.