Lessons from Warren Buffet’s Investing Strategy: Bonds & the Evidence for Value Investing

Yes, Kailash has done vast amounts of research on the historical data and built powerful proprietary quantamental models to help long-term investors make money with an emphasis on quality and price. Yes, this method has been proven out in the data since the advent of capitalism. And yes….this method of investing very much foots with the teachings of the greatest investors in US history.

Get our insights direct to your inbox: SUBSCRIBE

In that vein, Kailash believes reading how the long-term compounders of capital won and win is one of the most potent methods to uncover true “value” in markets. Kailash brings no hubris to investing: we will listen to all sides of a debate, analyze the history when available and render our findings with the integrity and trust our readers expect. We use this Quick Take to suggest that in today’s markets there is nothing less common than common sense.

Learning from the Berkshire Hathaway Company:

In our QTFC on Berkshire Hathaway Energy, Kailash documented that Buffett has succeeded in showing America a profitable path to build out lower priced renewable energy for customers while investing massive and much needed funds into the grid. In our last QTFC, Kailash hammered a recent battery electric SPAC. We contrast the two pieces here because we find it confusing that in a world swamped with aspirational environmental plans, people are paying huge sums for the profitless and unproven.

Sitting there for the entire country to see is a successfully implemented roadmap to move America to energy independence in a manner that is good for all stake-holders. Kailash views the dichotomy as still more evidence of the obvious: the path to compounding wealth at above average rates is paved with proven and profitable firms trading at reasonable prices. Although not often discussed, reducing equity duration risk is equally important.

Our most recent white paper on the Great Inflation carried no less than six outsized quotes from Buffett & Munger. For those irritated by our insistent beating of the Buffett & Munger drum you can be sure that we intend to apologize at a quarter-past-never. These are days of miracle, wonder and malfeasance in our view. As legendary equity researcher and short seller Jim Chanos discussed in the FT, we are in the Golden Age of Fraud.[1]

Kailash believes in times like these the need to remember the lessons of history and stick to the basics is an urgent imperative.

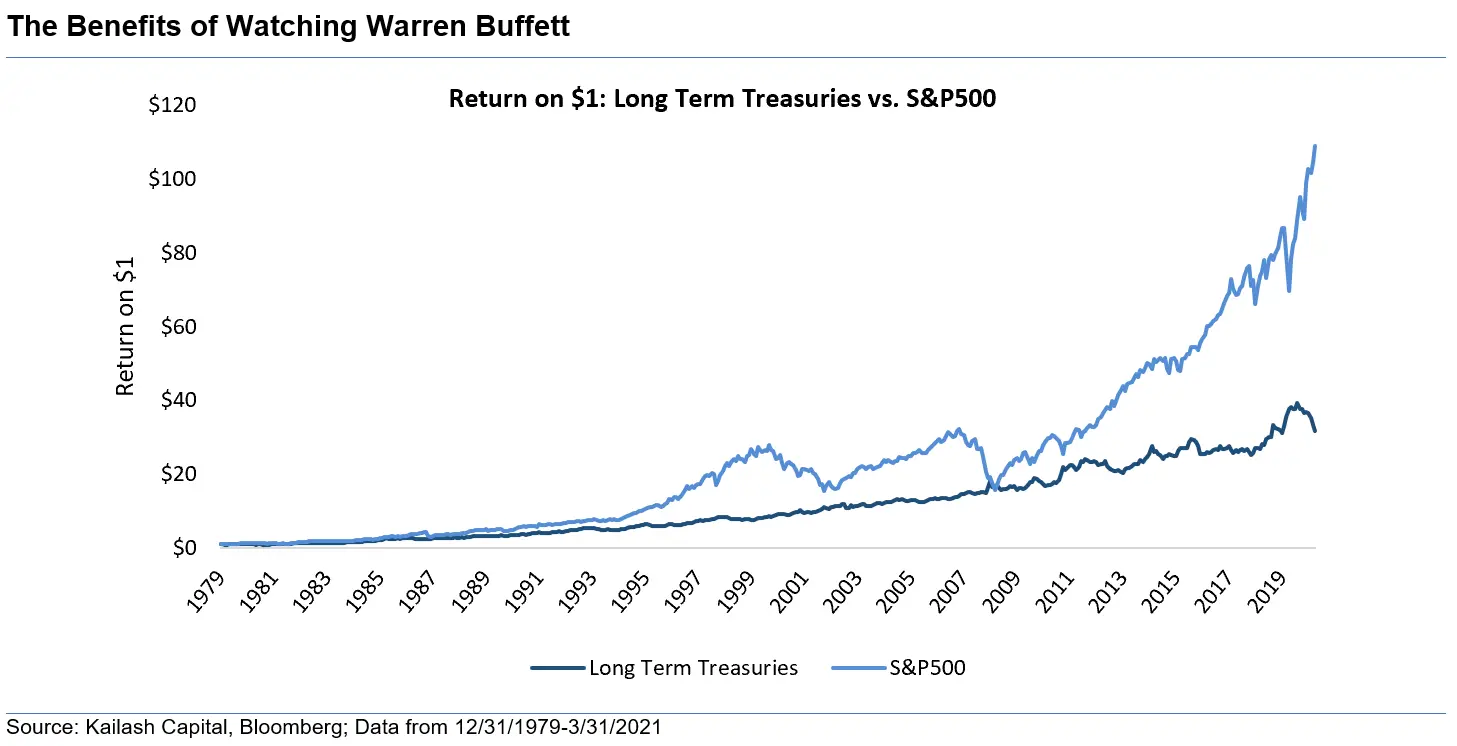

Stocks Versus Bonds & Buffett’s Case for Value Investing in 1980:

As mentioned above, Kailash believes that our investment tools are potent stuff. That belief stems from the fact they were built based on the empirical data from history – not from a set of preconceived notions. Kailash republishes Buffett’s quote from 1980 discussing how bonds, which were paying interest at 12% then, were a losing proposition vs. equities. Incredibly, he contextualizes the idea by addressing how the two assets might perform between 1980 and 2020.

The buyer of money to be used between 1980 and 2020 has been able to obtain a firm price now for each year of its use while the buyer of auto insurance, medical services, newsprint, office space – or just about any other product or service – would be greeted with laughter if he were to request a firm price now to apply through 1985. … our unwillingness to fix a price now for a pound of See’s candy … to be delivered in 2010 or 2020 makes us equally unwilling to buy bonds which set a price on money now for use in those years. Overall, we opt for Polonius (slightly restated): “Neither a short-term borrower nor a long-term lender be.” [2]

-Warren Buffett, 1980

The Results: How Warren Buffet’s Views on Bonds Panned Out

So how did Mr. Buffett’s “call” to avoid government bonds throwing off 12% interest payments and invest in the stock market turn out? The chart below suggests the man who said “long equities” and “avoid bonds” in 1980 understood something few could grasp at the time. In 1980 Warren Buffett said that by 2020 bonds were a losing proposition vs. equities and he was right.

With government bonds yielding near zero, corporate bonds at record low spreads and the junk bond market offering some of the weakest covenants in history, today strikes us as more challenging. If your time horizon is short, holding equities does create a higher risk if you are forced to sell. If you intend to hold your investments for a long time however, bonds on the other hand carry both interest rate risk and near-zero nominal returns today. Considering this painful set of choices we can think of far worse places to invest than Mr. Buffett’s holding company.

As documented in footnotes 2-9 in this QTFC, Buffett was absolutely pilloried in the press in 2000. We see a similar, if somewhat less caustic, behavior underway today. Kailash holds a fervent belief that the man who helms the largest private owner of American assets[3] will be vindicated much like he was post the 2000 bubble. With his 60+ year track record of successfully swimming against the tide, Kailash believes watching what he does is more important today than any time in his storied career.

Kailash believes that there is a large swath of low quality firms priced at valuations that have always been the precursors to horrible future returns. We believe this is particularly true in the IT sector where the froth has eclipsed the levels seen at the peak of the internet bubble in 2000. In our paper Income Investing: Staples & IT Kailash presented a brutal chart showing that over a trillion dollars of IT stocks were losing money and published a list of all the IT stocks trading over 100x earnings. These stocks strike us as an uncommonly good way to skip a trip to the casino but an uncommonly poor way to handle your savings.

The good news for long-term investors looking to compound capital at above average rates is that the application of common sense has rarely been more important than it is today. The history books are unambiguous: buying high quality cash-generating businesses at fair to low prices is a terrific way to compound wealth.

This is what Kailash specializes in. Our newsletters and investment tools are committed to helping people interested in compounding capital using the most time-tested method we know of. Good companies, good managements and good businesses purchased at reasonable prices. You can find them on our website or by contacting us here. To learn about and gain access to our powerful tools built using research proven out in practice and academia please:

- Click here for our paper explaining our Stock Ranking Tools

- Click here for our research explaining how to identify firms engaged in earnings management

- Click here for our research on some of the pitfalls faced by investors in index funds

For those of you unfamiliar with Kailash, we believe our organization provides cutting edge, thought-driven, investment analysis tools at prices others simply cannot match. Our research staff has been together for over a decade and has well over 100 years of experience. The team includes proven veterans in the investment management business and one of the most prominent academics in the field of behavioral finance. Our services bring the best of breed quantamental tools and themes to your doorstep.

Disclaimer

The information, data, analyses, and opinions presented herein (a) do not constitute investment advice, (b) are provided solely for informational purposes and therefore are not, individually or collectively, an offer to buy or sell a security, (c) are not warranted to be correct, complete or accurate, and (d) are subject to change without notice. Kailash Capital Research, LLC and its affiliates (collectively, “Kailash Capital Research, LLC ”) shall not be responsible for any trading decisions, damages or other losses resulting from, or related to, the information, data, analyses or opinions or their use. The information herein may not be reproduced or retransmitted in any manner without the prior written consent of Kailash Capital Research, LLC . In preparing the information, data, analyses, and opinions presented herein, Kailash Capital Research, LLC has obtained data, statistics, and information from sources it believes to be reliable. Kailash Capital Research, LLC , however, does not perform an audit or seeks independent verification of any of the data, statistics, and information it receives. Kailash Capital Research, LLC and its affiliates do not provide tax, legal, or accounting advice. This material has been prepared for informational purposes only and is not intended to provide, and should not be relied on for tax, legal, or accounting advice. You should consult your tax, legal, and accounting advisors before engaging in any transaction. © 2021 Kailash Capital Research, LLC – All rights reserved.

Nothing herein shall limit or restrict the right of affiliates of Kailash Capital Research, LLC to perform investment management or advisory services for any other persons or entities. Furthermore, nothing herein shall limit or restrict affiliates of Kailash Capital Research, LLC from buying, selling or trading securities or other investments for their own accounts or for the accounts of their clients. Affiliates of Kailash Capital Research, LLC may at any time have, acquire, increase, decrease or dispose of the securities or other investments referenced in this publication. Kailash Capital Research, LLC shall have no obligation to recommend securities or investments in this publication as result of its affiliates’ investment activities for their own accounts or for the accounts of their clients.