Another Reason to Pursue High Quality Value Investing

My father, a youthful 77-year-old, recently flattered me with some investment advice. Having recently received an email solicitation encouraging him to sell any muni bonds he might have to fund some “easy money” in SPACs, he wanted to share the good news. The email’s enthusiasm for an entirely unverified asset-class of mixed reputation was predicated on recent returns achieved in the SPAC category. By way of preview, your author is unconvinced. This morning’s SPAC news did little to mitigate that skepticism.

Get our insights direct to your inbox: SUBSCRIBE

Apparently, the Germans are bringing their engineering expertise to the US SPAC frenzy. The target company being acquired by the US listed SPAC is German startup Lilium. Lilium is a future manufacturer of electric powered aircraft. The assertion being that Lilium will revolutionize regional travel at incredibly low costs via aircraft with comfortable seating for 16. San Fran to Palo Alto? According to the press release, give them $90 and 90 minutes – no problem. The article notes that the SPAC will buy the German firm at a price valuing the combined entity at $3.3bn. In the world of battery electric anything, $3.3bn sounds like a bargain lately.

I will be the first to admit that when the story hit, my knowledge regarding the commercial viability of electric powered aircraft was precisely zero. Now I have googled “Lilium,” and found a remarkable video of their product – an electric aircraft. This stuff is amazing to see and a testament to human ingenuity and optimism. What is less-than-amazing is the company’s not-yet-working website, copied below. This article from a year ago about how one of Lilium’s two prototypes exploded in flames also might be considered a potential red-flag. Even Kailash has a working website now.

And a website is a big innovation for us old-fashioned believers in things like revenues and, when possible, profits. We are short big ideas and long big profits at reasonable prices. As value investors with a quality bias, Kailash has substantiated the rationale for our process in papers such as High-Quality Midcap Value, Value Investing in Manias, Value vs. Momentum and many other papers found on our website. All these papers and our ever-expanding library of quantamental research is predicated on identifying the risks and opportunities that emerge from behavioral biases that have plagued investors since records began.

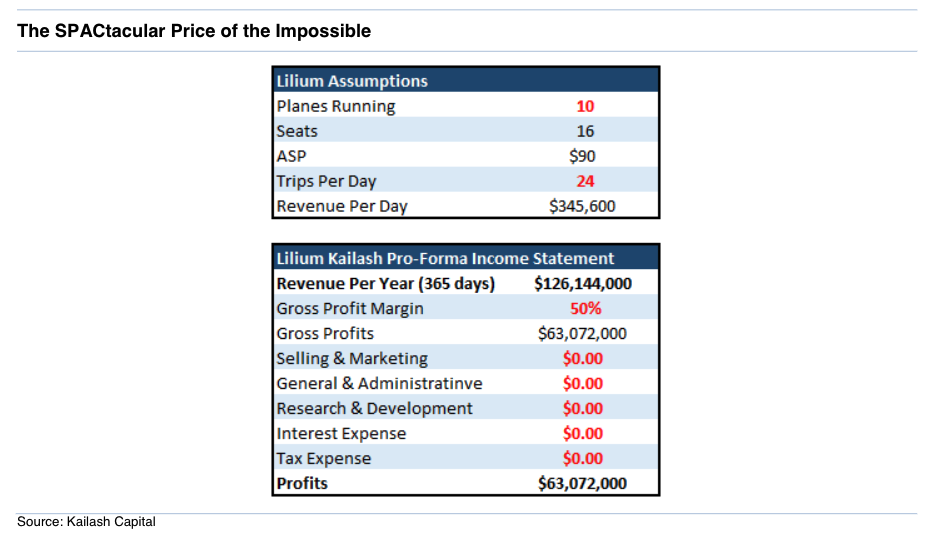

But let’s give Lilium the benefit of the doubt – after all it has the authentic stamp of German ingenuity. Plus, the prototype looks really cool. The company claims they may have an operating craft to carry 16 people to-and-fro by 2024. Let’s also recognize we are in the age of innovation and give the company a series of extraordinary breakthroughs. Let’s grant Lilium the following operating advancements effective immediately:

- 10 Liliums operating today between San Francisco and Palo Alto

- A set of indefatigable pilots trained in the yet-to-exist aircraft willing to work 24×7 without compensation

- Let’s give them Google’s gross profit margins of ~50%

- Let’s then alleviate them of the sundry marketing, wage, regulatory, research, advertising and tax costs that encumber most income statements

- Let’s assume that instead of taking the aforementioned 90 minutes to make the flights, it takes 60 minutes

- Let’s further assume that the planes never need maintenance and can operate 24/7 with zero time for takeoff, landing, embarkation or disembarkation

- Let’s further assume that 100% of every flight is fully sold out 24/7/365 a year

We can summarize the above assumptions into the excel exhibit immediately below. Revenues are 10 planes x 16 passengers x $90 per passenger x 24 hours x 7 days a week x 365 days a year. Gross profits = net profits. Don’t ever accuse Kailash of lacking optimism! If we afforded the company that cascading series of impossible breakthroughs, it’s income statement would look like the one below. Even granting Lilium a series of impossible breakthroughs, at $3.3bn that would put the company at over 25x revenues or 50x earnings. This exercise shows that with free money, a dearth of regulatory encumbrance, powerful incentives adverse to shareholder interests and a set of ludicrous assumptions, we too can still come up with an overpriced SPAC….

For investors who find speculating in SPACs unappealing Kailash may have a solution. Our products are committed to helping people interested in compounding capital using the industry’s best investment tools. You can find them on our website or by contacting us here. To learn about and gain access to our powerful tools built using research proven out in practice and academia please:

- Click here for our paper explaining our Stock Ranking Tools

- Click here for our research explaining how to identify firms manipulating earnings to fool investors

- Click here for our research explaining how to identify the best peers to compare stocks you might have an interest in researching and investing in

- Click here for our research on how to think about Beta and the risk of individual securities and indexes

- Click here for our research on some of the pitfalls faced by investors in index funds

For those of you unfamiliar with Kailash, we believe our organization provides cutting edge, thought-driven, investment analysis tools at prices others simply cannot match. Our research staff has been together for over a decade, has well over 100 years of experience. The team includes proven veterans in the investment management business and one of the most prominent academics in the field of behavioral finance. Our services bring the best of breed quantamental tools and themes to your doorstep.

Disclaimer

The information, data, analyses, and opinions presented herein (a) do not constitute investment advice, (b) are provided solely for informational purposes and therefore are not, individually or collectively, an offer to buy or sell a security, (c) are not warranted to be correct, complete or accurate, and (d) are subject to change without notice. Kailash Capital Research, LLC and its affiliates (collectively, “Kailash Capital Research, LLC ”) shall not be responsible for any trading decisions, damages or other losses resulting from, or related to, the information, data, analyses or opinions or their use. The information herein may not be reproduced or retransmitted in any manner without the prior written consent of Kailash Capital Research, LLC . In preparing the information, data, analyses, and opinions presented herein, Kailash Capital Research, LLC has obtained data, statistics, and information from sources it believes to be reliable. Kailash Capital Research, LLC , however, does not perform an audit or seeks independent verification of any of the data, statistics, and information it receives. Kailash Capital Research, LLC and its affiliates do not provide tax, legal, or accounting advice. This material has been prepared for informational purposes only and is not intended to provide, and should not be relied on for tax, legal, or accounting advice. You should consult your tax, legal, and accounting advisors before engaging in any transaction. © 2021 Kailash Capital Research, LLC – All rights reserved.

Nothing herein shall limit or restrict the right of affiliates of Kailash Capital Research, LLC to perform investment management or advisory services for any other persons or entities. Furthermore, nothing herein shall limit or restrict affiliates of Kailash Capital Research, LLC from buying, selling or trading securities or other investments for their own accounts or for the accounts of their clients. Affiliates of Kailash Capital Research, LLC may at any time have, acquire, increase, decrease or dispose of the securities or other investments referenced in this publication. Kailash Capital Research, LLC shall have no obligation to recommend securities or investments in this publication as result of its affiliates’ investment activities for their own accounts or for the accounts of their clients.