- Introduction: Value vs. Momentum

- Small & Mid Cap: A Historical Outlier Suggests Outsized Opportunities

- The Myth of Melting Ice Cubes?

- Conclusion: A Basket Worth Buying?

- Exhibit

Introduction: Value vs. Momentum

In Kailash’s recent pieces discussing the dispersion in value vs. growth stocks carrying the scintillating titles of Growth vs. Value and Growth vs. Value Part II, these papers built on some of our prior work that pointed out:

• Private Equity firms were reporting historically large inflows while having fewer promising targets and an uncommon reliance on unusually accommodative debt markets

• Elevated market valuations as defined by Warren Buffett posed a potential risk to investors of all stripes

• The methodologies of some indexes’ construction could make passive investors particularly vulnerable as discussed in Kailash’s July and October papers about the “Passive Patsies”

Get our White Papers direct to your inbox: SUBSCRIBE

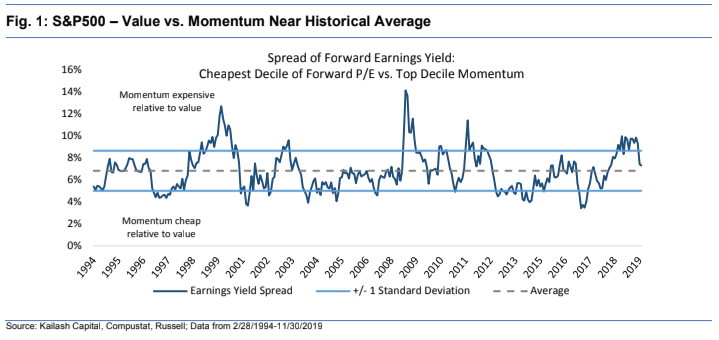

Your author wants to acknowledge a recent article in the Wall Street Journal1 which cited data suggesting value investing might not be dead. Of particular interest was a chart showing that “value” stocks as defined by forward P/E ratios vs. stocks with high 12-month momentum were at spreads rarely seen before. In Growth vs. Value Part I and Part II page one displayed a chart highlighting that growth ceded a decade’s outperformance over value in just 6 months post the tech bubble.

Reflecting on this Kailash decided to analyze the spreads between the forward P/Es of the cheapest decile of stocks and high momentum stocks.2 In the Kailash S&P500 Universe we discovered a materially different finding as displayed in Fig. 1 below. S&P500 momentum stocks are roughly in line with history when comparing forward P/Es to their value counterparts. However, upon further investigation Kailash did discover a meaningful and actionable finding within the Small and Mid Cap universe explained in the ensuing pages.

Disclaimer

The information, data, analyses, and opinions presented herein (a) do not constitute investment advice, (b) are provided solely for informational purposes and therefore are not, individually or collectively, an offer to buy or sell a security, (c) are not warranted to be correct, complete or accurate, and (d) are subject to change without notice. Kailash Capital Research, LLC and its affiliates (collectively, “Kailash Capital Research, LLC ”) shall not be responsible for any trading decisions, damages or other losses resulting from, or related to, the information, data, analyses or opinions or their use. The information herein may not be reproduced or retransmitted in any manner without the prior written consent of Kailash Capital Research, LLC . In preparing the information, data, analyses, and opinions presented herein, Kailash Capital Research, LLC has obtained data, statistics, and information from sources it believes to be reliable. Kailash Capital Research, LLC , however, does not perform an audit or seeks independent verification of any of the data, statistics, and information it receives. Kailash Capital Research, LLC and its affiliates do not provide tax, legal, or accounting advice. This material has been prepared for informational purposes only and is not intended to provide, and should not be relied on for tax, legal, or accounting advice. You should consult your tax, legal, and accounting advisors before engaging in any transaction. © 2021 Kailash Capital Research, LLC – All rights reserved.

Nothing herein shall limit or restrict the right of affiliates of Kailash Capital Research, LLC to perform investment management or advisory services for any other persons or entities. Furthermore, nothing herein shall limit or restrict affiliates of Kailash Capital Research, LLC from buying, selling or trading securities or other investments for their own accounts or for the accounts of their clients. Affiliates of Kailash Capital Research, LLC may at any time have, acquire, increase, decrease or dispose of the securities or other investments referenced in this publication. Kailash Capital Research, LLC shall have no obligation to recommend securities or investments in this publication as result of its affiliates’ investment activities for their own accounts or for the accounts of their clients.

December 23, 2019 |

| Authors: Matthew Malgari, Nathan Przybylo, Dr. Sanjeev Bhojraj and John Durkin

December 23, 2019

Authors: Matthew Malgari, Nathan Przybylo, Dr. Sanjeev Bhojraj and John Durkin