These are days of high-hopes and higher stock prices. As documented in two of our recent Charts For The Curious (“CFTC”), history suggests a very dim view on the cash-flow consuming speculations currently trading at massive multiples of sales. Our empirical research into the IPO frenzy underway, the most speculative fringes of growth, the mania chasing stocks that grow fast, and even the elevated valuations ascribed to many high-quality growth firms is conclusive in all instances: it ends badly. Whole swaths of today’s market offer the very definition of stock speculation in a simple chart.

Get our insights direct to your inbox: SUBSCRIBE

In true Kailash fashion, we have suggested investors avoid the herd and embrace the wonderful bargains[1] among some of the most reliable and proven businesses. It is not easy to quell the urge to rush into the stocks you hear are making the neighbors millionaires overnight. Yet Kailash has been keen to point out that if you are willing to avoid speculative IT, many firms selling products that you understand and need, renowned for their reliable compounding of wealth, Staples stocks, are trading at record discounts to the market.

In our view, one of the greatest bubbles underway is in Electric Vehicles and the broader renewable energy space. While Kaialsh views the spectacular valuations ascribed to the bevy of cleantech stocks and SPACs that are, or soon will be, pouring more unreliable and unproven products into the market, Kailash understands the economic, strategic, and environmental benefits that motivate the global race to renewables. Despite our aversion to such stories, we found the recent documentation provided by a maverick and visionary breathtaking. The man asserted the following:

- Private enterprise working in cooperation with various Federal and State regulators could rebuild and modernize the US power grid’s distribution in a systematic and organized fashion

- Despite the large capital costs involved, the benefits were so great they could be shared between consumers and the private enterprise committing the capital to build the necessary asset base

- This symbiotic behavior between corporation, government, and consumer could lead to lower prices for consumers, much needed and new infrastructure, and vast increases in renewable power

Get our White Papers direct to your inbox: SUBSCRIBE

Kailash admits to being entranced by the story. The man did not just promise these things – he asserted the firm doing it could still grow actual earnings, not just sales!, at rates wildly in excess of GDP.

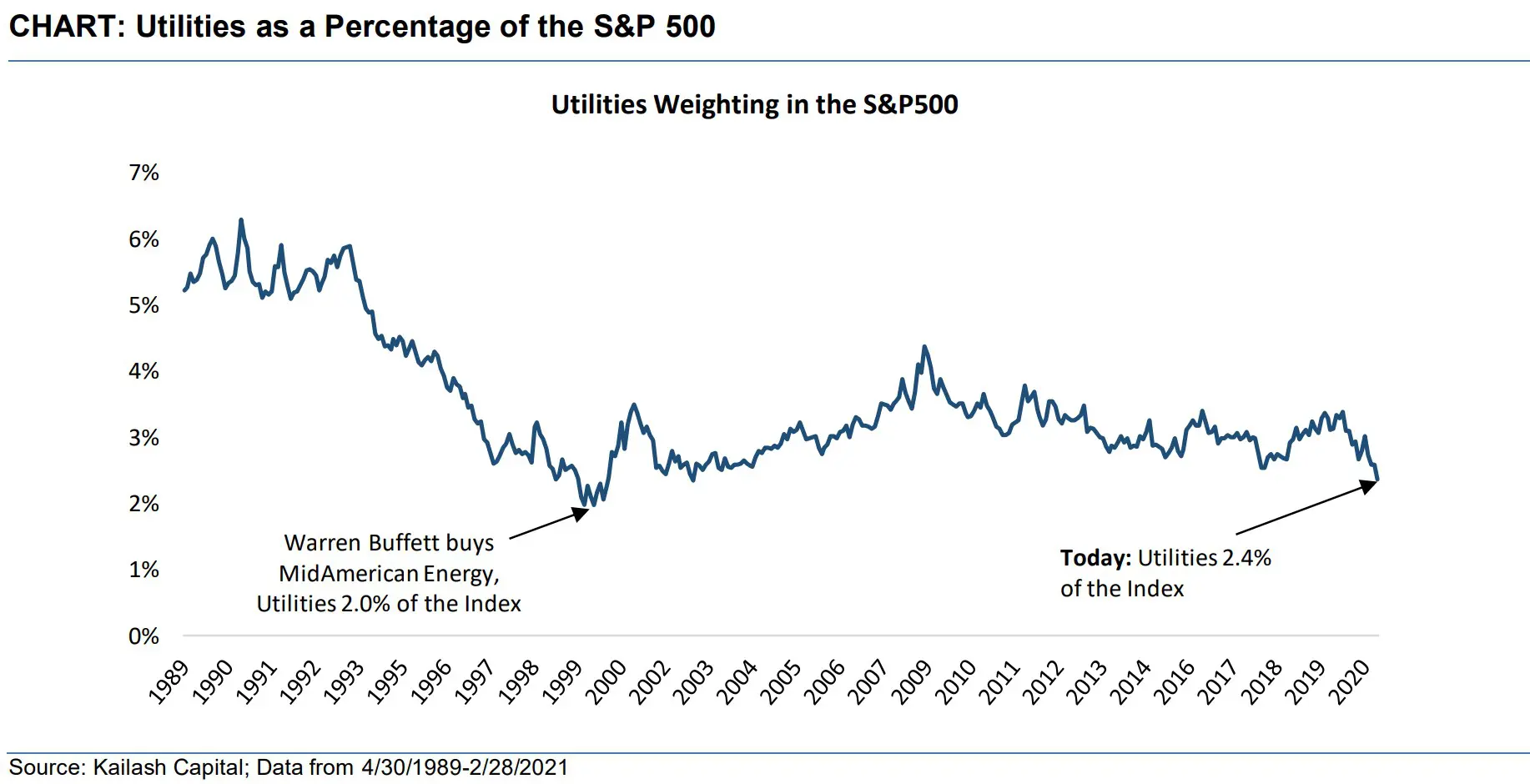

We are obviously referring to Warren Buffett’s discussion of Berkshire Hathaway Energy (BHE) in his last two letters to shareholders of Berkshire Hathaway. In 1999 while the world was awash in novel tech stocks that promised to change the world, Warren Buffett bought what many would suggest is the most boring asset of all: a utility.[2],[3] While many might not realize it: bought for a fair price and run well, utilities can be sultry and appealing businesses. Over 21 years, BHE would pay no dividends, reinvesting all its income and grow profits from $122 million to $3.4 billion – a 17% annualized growth rate.

While legend in outcome, Buffett’s arithmetic aptitude surfaces in some remarkable ways. BHE has retained $28 billion since Berkshire’s purchase and never paid a dividend. “That pattern is an outlier in the world of utilities, whose companies customarily pay big dividends … Our view: the more we can invest, the more we like it.”[4] Kailash finds it truly humbling to see how Buffett & Co. has transformed a utility into an incredible wealth compounding machine that also provides better prices to customers while building much needed infrastructure. His discussion of Berkshire’s Iowa utility is a stunning example of the benefits of retained earnings, compounding, and profitable growth investing. How much wealthier is BHE vs. a typical utility that pays out all its earnings?

More importantly, note that this penchant for simply reinvesting has now given BHE and its residential customers a 70% price advantage in the commodity business of electricity. BHE is the only investor-owned utility to achieve wind self-sufficiency. Even more remarkable is that the low-cost power provided by BHE has likely been a key reason three high-tech giants chose to site their plants in Iowa. Those three tech “newcomers” to Iowa are now three of BHE’s five largest customers.

Like 1999, today the press bemoans Buffett’s $140bn cash-pile and weak performance vs. the S&P over the last 10 years as discussed in our CFTC here. Kailash finds it instructive to revisit the benefits of a counter-cyclical investment process. Lagging the broad benchmark in 1999, the press on Buffett was merciless.[5],[6],[7],(the list could go on) In a six-hour presentation he gave, one Berkshire shareholder “…asked if Buffett would consider investing a small percentage … in technology companies. After all, the shareholder said, he himself had made up for heavy losses in Berkshire’s stock with keen investments in technology companies.”[8] Described on one message board as a “’middlebrow insurance company studded with a bizarre mélange of assets, including candy stores, hamburger stands, jewelry shops, a shoemaker and a third-rate encyclopedia company’”[9] the derision Buffett faced was more than this writer could take.

In the face of it all, Berkshire bought a utility. They went on to turn the industry model upside down and invest in green energy long before it was trendy, and managed to turn a utility into a growth stock. As a reminder, he purchased natural gas giant Dominion Energy in 2020 and recently cut Apple to buy Chevron and Verizon. In the same manner as the internet bubble, Kailash believes Buffett & Mungers’ no-nonsense commitment to compounding profits will once again outstrip the indexes, bloated by cash-flow lite tech stocks trading at incredible valuations, handily in the years ahead.

Kailash encourages investors to review his brief discussions of Berkshire Energy from his 2019 and 2020 Chairman’s Letters which we have reproduced, chronologically, below:

Chairman’s Letter – 2019

Berkshire Hathaway Energy

Berkshire Hathaway Energy is now celebrating its 20th year under our ownership. That anniversary suggests that we should be catching up with the company’s accomplishments.

We’ll start with the topic of electricity rates. When Berkshire entered the utility business in 2000, purchasing 76% of BHE, the company’s residential customers in Iowa paid an average of 8.8 cents per kilowatt-hour (kWh). Prices for residential customers have since risen less than 1% a year, and we have promised that there will be no base rate price increases through 2028. In contrast, here’s what is happening at the other large investor-owned Iowa utility: Last year, the rates it charged its residential customers were 61% higher than BHE’s. Recently, that utility received a rate increase that will widen the gap to 70%.

The extraordinary differential between our rates and theirs is largely the result of our huge accomplishments in converting wind into electricity. In 2021, we expect BHE’s operation to generate about 25.2 million megawatt-hours of electricity (MWh) in Iowa from wind turbines that it both owns and operates. That output will totally cover the annual needs of its Iowa customers, which run to about 24.6 million MWh. In other words, our utility will have attained wind self-sufficiency in the state of Iowa.

In still another contrast, that other Iowa utility generates less than 10% of its power from wind. Furthermore, we know of no other investor-owned utility, wherever located, that by 2021 will have achieved a position of wind self-sufficiency. In 2000, BHE was serving an agricultural-based economy; today, three of its five largest customers are high-tech giants. I believe their decisions to site plants in Iowa were in part based upon BHE’s ability to deliver renewable, low-cost energy.

Of course, wind is intermittent, and our blades in Iowa turn only part of the time. In certain periods, when the air is still, we look to our non-wind generating capacity to secure the electricity we need. At opposite times, we sell the excess power that wind provides us to other utilities, serving them through what’s called “the grid.” The power we sell them supplants their need for a carbon resource – coal, say, or natural gas.

Berkshire Hathaway now owns 91% of BHE in partnership with Walter Scott, Jr. and Greg Abel. BHE has never paid Berkshire Hathaway a dividend since our purchase and has, as the years have passed, retained $28 billion of earnings. That pattern is an outlier in the world of utilities, whose companies customarily pay big dividends – sometimes reaching, or even exceeding, 80% of earnings. Our view: The more we can invest, the more we like it.

Today, BHE has the operating talent and experience to manage truly huge utility projects – requiring investments of $100 billion or more – that could support infrastructure benefitting our country, our communities and our shareholders. We stand ready, willing and able to take on such opportunities.

Chairman’s Letter – 2020

BHE, unlike BNSF, pays no dividends on its common stock, a highly-unusual practice in the electric-utility industry. That Spartan policy has been the case throughout our 21 years of ownership. Unlike railroads, our country’s electric utilities need a massive makeover in which the ultimate costs will be staggering. The effort will absorb all of BHE’s earnings for decades to come. We welcome the challenge and believe the added investment will be appropriately rewarded.

Let me tell you about one of BHE’s endeavors – its $18 billion commitment to rework and expand a substantial portion of the outdated grid that now transmits electricity throughout the West. BHE began this project in 2006 and expects it to be completed by 2030 – yes, 2030.

The advent of renewable energy made our project a societal necessity. Historically, the coal-based generation of electricity that long prevailed was located close to huge centers of population. The best sites for the new world of wind and solar generation, however, are often in remote areas. When BHE assessed the situation in 2006, it was no secret that a huge investment in western transmission lines had to be made. Very few companies or governmental entities, however, were in a financial position to raise their hand after they tallied the project’s cost.

BHE’s decision to proceed, it should be noted, was based upon its trust in America’s political, economic and judicial systems. Billions of dollars needed to be invested before meaningful revenue would flow. Transmission lines had to cross the borders of states and other jurisdictions, each with its own rules and constituencies. BHE would also need to deal with hundreds of landowners and execute complicated contracts with both the suppliers that generated renewable power and the far-away utilities that would distribute the electricity to their customers. Competing interests and defenders of the old order, along with unrealistic visionaries desiring an instantly-new world, had to be brought on board.

Both surprises and delays were certain. Equally certain, however, was the fact that BHE had the managerial talent, the institutional commitment and the financial wherewithal to fulfill its promises. Though it will be many years before our western transmission project is completed, we are today searching for other projects of similar size to take on.

Whatever the obstacles, BHE will be a leader in delivering ever-cleaner energy

Disclaimer

The information, data, analyses, and opinions presented herein (a) do not constitute investment advice, (b) are provided solely for informational purposes and therefore are not, individually or collectively, an offer to buy or sell a security, (c) are not warranted to be correct, complete or accurate, and (d) are subject to change without notice. Kailash Capital Research, LLC and its affiliates (collectively, “Kailash Capital Research, LLC ”) shall not be responsible for any trading decisions, damages or other losses resulting from, or related to, the information, data, analyses or opinions or their use. The information herein may not be reproduced or retransmitted in any manner without the prior written consent of Kailash Capital Research, LLC . In preparing the information, data, analyses, and opinions presented herein, Kailash Capital Research, LLC has obtained data, statistics, and information from sources it believes to be reliable. Kailash Capital Research, LLC , however, does not perform an audit or seeks independent verification of any of the data, statistics, and information it receives. Kailash Capital Research, LLC and its affiliates do not provide tax, legal, or accounting advice. This material has been prepared for informational purposes only and is not intended to provide, and should not be relied on for tax, legal, or accounting advice. You should consult your tax, legal, and accounting advisors before engaging in any transaction. © 2021 Kailash Capital Research, LLC – All rights reserved.

Nothing herein shall limit or restrict the right of affiliates of Kailash Capital Research, LLC to perform investment management or advisory services for any other persons or entities. Furthermore, nothing herein shall limit or restrict affiliates of Kailash Capital Research, LLC from buying, selling or trading securities or other investments for their own accounts or for the accounts of their clients. Affiliates of Kailash Capital Research, LLC may at any time have, acquire, increase, decrease or dispose of the securities or other investments referenced in this publication. Kailash Capital Research, LLC shall have no obligation to recommend securities or investments in this publication as result of its affiliates’ investment activities for their own accounts or for the accounts of their clients.