Executive Summary

Introduction: In May 2014 we published the white papers “Bubble Trouble? Comparing the Current Markets to 1999 and 2007” and “Comparing the Small & Mid Cap Valuation Tails: Low Dispersion, Reduced Opportunities & Fundamental Fixes.” In that work, we surmised that the R2500 was in the “Value Doldrums” which indicated that the cheapest stocks would likely underperform the most expensive stocks (i.e., growth would likely outperform value). This came to fruition over the last 13 months, with the most expensive stocks soaring in value despite deteriorating fundamentals.

Get our White Papers direct to your inbox: SUBSCRIBE

Conclusions:

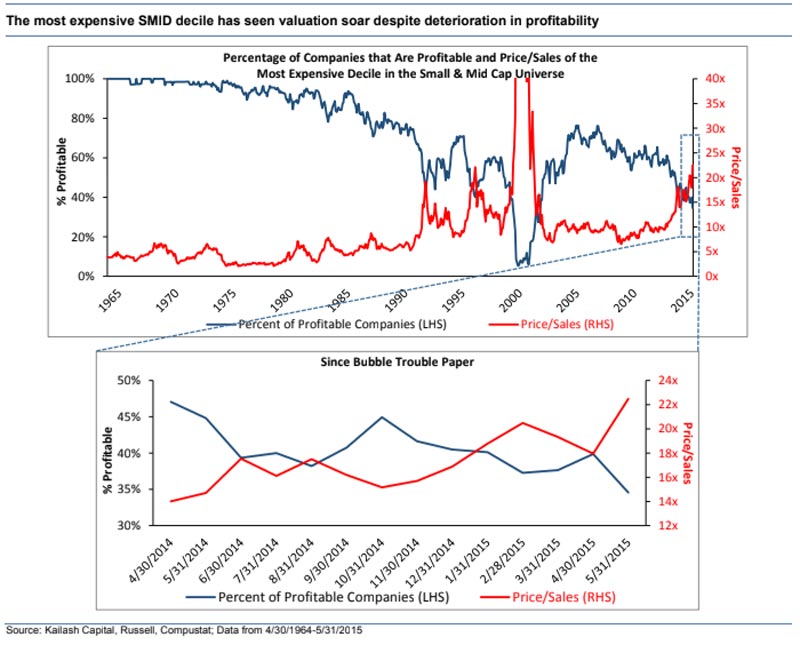

1) Median P/S valuation has soared 60% for the most expensive SMID decile since our earlier papers while profitability, as measured by the percentage of companies that are profitable, has deteriorated by a significant 13% points to only 35% of the companies being profitable. One could infer from the below charts that the excess returns of the most expensive decile came entirely or primarily from multiple expansion and not an improvement in fundamentals.

Disclaimer

The information, data, analyses, and opinions presented herein (a) do not constitute investment advice, (b) are provided solely for informational purposes and therefore are not, individually or collectively, an offer to buy or sell a security, (c) are not warranted to be correct, complete or accurate, and (d) are subject to change without notice. Kailash Capital Research, LLC and its affiliates (collectively, “Kailash Capital Research, LLC ”) shall not be responsible for any trading decisions, damages or other losses resulting from, or related to, the information, data, analyses or opinions or their use. The information herein may not be reproduced or retransmitted in any manner without the prior written consent of Kailash Capital Research, LLC . In preparing the information, data, analyses, and opinions presented herein, Kailash Capital Research, LLC has obtained data, statistics, and information from sources it believes to be reliable. Kailash Capital Research, LLC , however, does not perform an audit or seeks independent verification of any of the data, statistics, and information it receives. Kailash Capital Research, LLC and its affiliates do not provide tax, legal, or accounting advice. This material has been prepared for informational purposes only and is not intended to provide, and should not be relied on for tax, legal, or accounting advice. You should consult your tax, legal, and accounting advisors before engaging in any transaction. © 2021 Kailash Capital Research, LLC – All rights reserved.

Nothing herein shall limit or restrict the right of affiliates of Kailash Capital Research, LLC to perform investment management or advisory services for any other persons or entities. Furthermore, nothing herein shall limit or restrict affiliates of Kailash Capital Research, LLC from buying, selling or trading securities or other investments for their own accounts or for the accounts of their clients. Affiliates of Kailash Capital Research, LLC may at any time have, acquire, increase, decrease or dispose of the securities or other investments referenced in this publication. Kailash Capital Research, LLC shall have no obligation to recommend securities or investments in this publication as result of its affiliates’ investment activities for their own accounts or for the accounts of their clients.

August 8, 2015 |

| Authors: Matthew Malgari, Nathan Przybylo, Dr. Sanjeev Bhojraj and John Durkin

August 8, 2015

Authors: Matthew Malgari, Nathan Przybylo, Dr. Sanjeev Bhojraj and John Durkin