- Introduction: Sometimes Equities Are Bond Proxies, Other Times They Are Not

- Where Are We Today?

- Qualitative Conclusion on Empirical Outcomes

- Optimizing Picks Within a Pack of Winners

- Exhibits

- Appendix: Small & Mid Cap Data

Introduction: Sometimes Equities Are Bond Proxies, Other Times They Are Not

In a world beset by central bankers driving yields relentlessly lower with no respect for a growing cohort of stakeholders (i.e., retirees) investors have been in a frenzy to find yield and investors seem to be taking what they can get where they can get it – both pursuing higher coupons in explicitly riskier assets while also pursing assets with some modicum of coupon in sectors they perceive as safe. As recently as June, BlackRock data showed that high dividend funds took the dubious title of top honors in the ETF category with $3.8 billion in flows, the best month on record.1 In the mutual fund category, Vanguard’s monolithic $30 billion dollar Dividend Growth Fund, which has seen AUM double over the past three years, stopped accepting new investors after a $3 billion inflow in just six months.2 Seeing investors trample all over themselves in the quest for yield, even the Wall Street Journal began to warn that “Low Vol” and “High Dividend” strategies were often overlapping concepts and noted that low volatility shares traded at as wide a premium to high volatility shares as at any time in the past 30 years.3 Yet recent headlines seem to be pointing toward the beginning of an exodus from such strategies that, should it continue, may turn into an unpleasant stampede.4

Get our White Papers direct to your inbox: SUBSCRIBE

This is not the first time Kailash has flirted with dividends. In our paper The Dividend Deception dated January 2014 we worried that the group, then dominated by MLPs characterized by excessive payouts and stretched valuations, appeared a bit like inviting investors to have a quick smoke in the dynamite shed rather than a place appropriate for widows and orphans as the group was often marketed. We find aspects and areas of today’s investment environment no-less confusing and precarious as we did back then, but rather than try and call the timing around a specific sector or group we are intent on helping our partners do a better job of locating intelligent yields.

In working through different methods on how best to pursue shareholder yields (dividends + repurchases), we examined a good deal of the product offerings in both the passive and active universes. One of the things that stood out to us is that many of the passive approaches seemed to embrace survivorship bias by buying only stocks that had achieved certain historical hurdles for certain historical horizons while active participants most often embraced highly qualitative items that we found difficult to memorialize and test in empirical form. In typical Kailash fashion we decided to couch our approach in the arcane and complex world of “COMMON SENSE.”

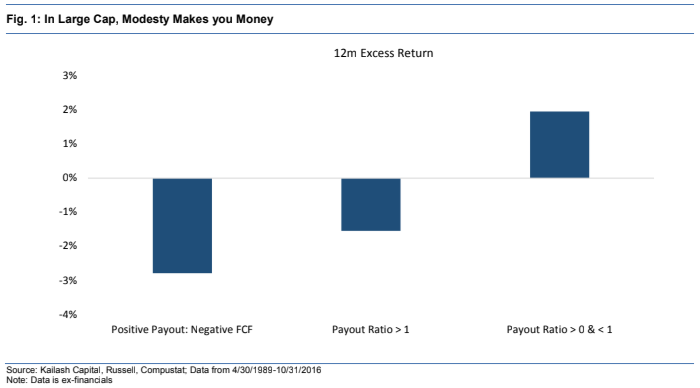

We made the decision to bucket firms that paid investors into three discreet groups:

- Those with negative free cash flow who paid owners either via dividends, repurchases or both (Positive Payout: Negative FCF)

- Those with positive free cash flow who paid owners via dividends, repurchases or both but in amounts exceeding available free cash flow (Payout Ratio >1)

- Those with positive free cash flow who paid owners via dividends, repurchases or both but in amounts greater than zero but less than 100% of available funds from ongoing free cash flows (Payout Ratio >0 and <1)

Considering the intuitive and obvious appeal of such an approach we found the results shown in Figure 1 below quite compelling.

Disclaimer

The information, data, analyses, and opinions presented herein (a) do not constitute investment advice, (b) are provided solely for informational purposes and therefore are not, individually or collectively, an offer to buy or sell a security, (c) are not warranted to be correct, complete or accurate, and (d) are subject to change without notice. Kailash Capital Research, LLC and its affiliates (collectively, “Kailash Capital Research, LLC ”) shall not be responsible for any trading decisions, damages or other losses resulting from, or related to, the information, data, analyses or opinions or their use. The information herein may not be reproduced or retransmitted in any manner without the prior written consent of Kailash Capital Research, LLC . In preparing the information, data, analyses, and opinions presented herein, Kailash Capital Research, LLC has obtained data, statistics, and information from sources it believes to be reliable. Kailash Capital Research, LLC , however, does not perform an audit or seeks independent verification of any of the data, statistics, and information it receives. Kailash Capital Research, LLC and its affiliates do not provide tax, legal, or accounting advice. This material has been prepared for informational purposes only and is not intended to provide, and should not be relied on for tax, legal, or accounting advice. You should consult your tax, legal, and accounting advisors before engaging in any transaction. © 2021 Kailash Capital Research, LLC – All rights reserved.

Nothing herein shall limit or restrict the right of affiliates of Kailash Capital Research, LLC to perform investment management or advisory services for any other persons or entities. Furthermore, nothing herein shall limit or restrict affiliates of Kailash Capital Research, LLC from buying, selling or trading securities or other investments for their own accounts or for the accounts of their clients. Affiliates of Kailash Capital Research, LLC may at any time have, acquire, increase, decrease or dispose of the securities or other investments referenced in this publication. Kailash Capital Research, LLC shall have no obligation to recommend securities or investments in this publication as result of its affiliates’ investment activities for their own accounts or for the accounts of their clients.

November 23, 2016 |

| Authors: Matthew Malgari, Nathan Przybylo, Dr. Sanjeev Bhojraj and John Durkin

November 23, 2016

Authors: Matthew Malgari, Nathan Przybylo, Dr. Sanjeev Bhojraj and John Durkin