Executive Summary

Introduction: As a client of our work we know you are an active manager and hence familiar with the barrage of news stories that seem to revel in our industry’s pain. In fact, just this last Monday the Wall Street Journal had such an article on the front page. Generally speaking, active managers have been under immense and growing pressure over the last decade. As Kailash’s goal is to help clients with our work, we decided to examine some possible reasons for this immense pressure.

Get our White Papers direct to your inbox: SUBSCRIBE

Conclusions:

1) Almost all new money flows to equities are going to index funds, ETFs or other passive products with these passive products allocating capital blindly. In other words, capital allocation has been put on autopilot, and we feel the consequences may be circular: as money flows into a list of names, the job of rational capital allocators seeking defensive moats at reasonable prices becomes (temporarily) more difficult as the chaff is bought with the same bluster as the wheat. This reinforces the original benefit of index products (low fees) by creating a performance headwind for people who prefer companies that actually have any number of novel characteristics like earning money.

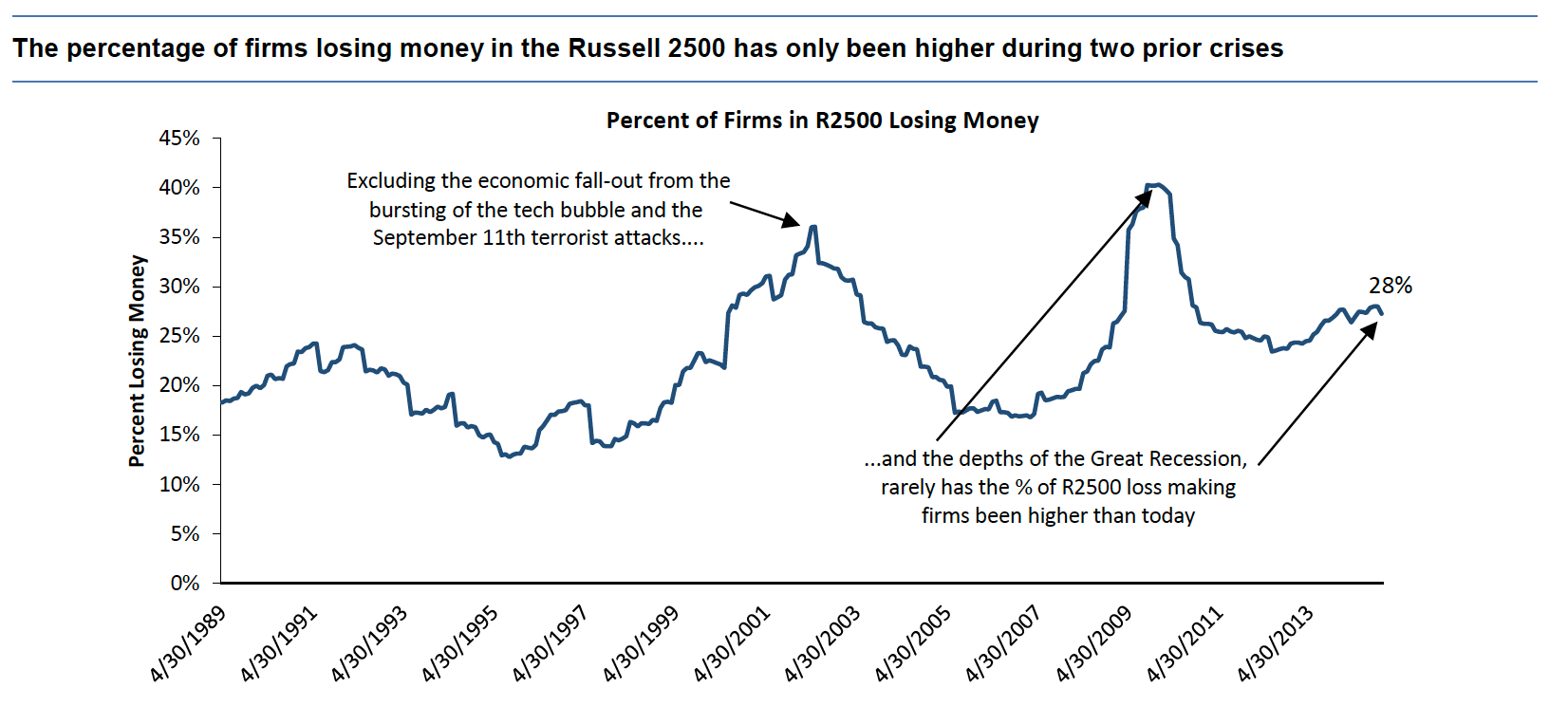

2) Much of the capital is being allocated to unprofitable companies as the percentage of companies in the Russell 2500 that are unprofitable—currently 28%—has never been higher except in major crises. With ample liquidity and growing investor euphoria, KCR believes investors will eventually have an opportunity to buy the best stocks for a recession at cheap prices. This is important as the current situation is even more concerning given that it is happening amidst an epic profit boom.

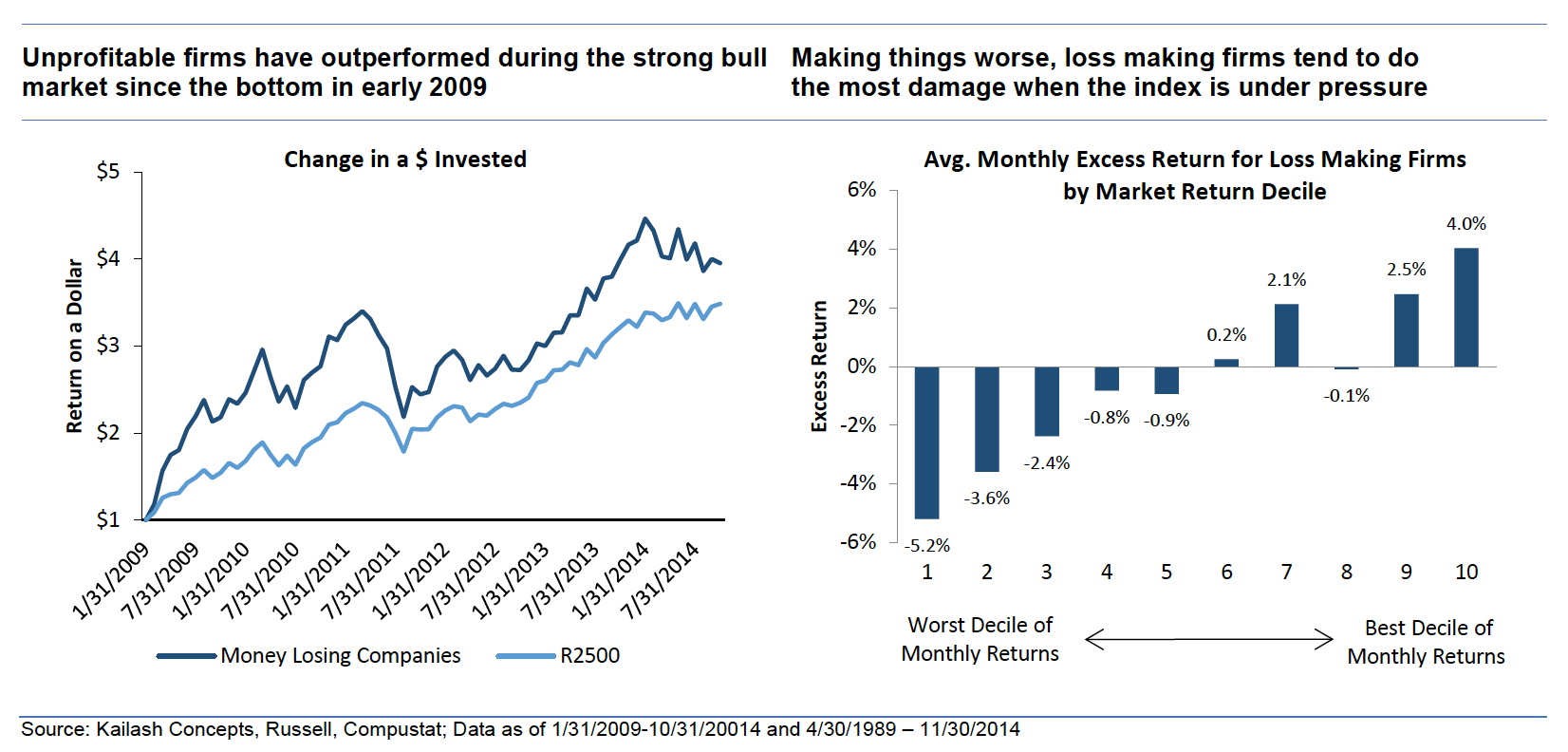

3) The chart below on the left shows that the compound returns to owning just the money losing firms in the Russell 2500 since the bottom of the great recession have actually exceeded the broader index returns. We believe this is notable because, as we show in our paper, unprofitable firms as a group underperform the benchmark 70% of the time on a 1 year basis and 86% of the time on a 3 year horizon. The below chart on the right shows the relative returns to money losing firms sorted by market environment. You can see that while money losing firms tend to be terrible performers in most periods, this is particularly true in downturns.

4) Buying index products now gives investors significant exposure to the performance of unprofitable companies. Active managers may want to explain to their customers that part of the reason index funds have been difficult to beat is we are now well into our fifth year of a strong bull market post the Great Recession—an environment in which loss making firms’ stocks can thrive. Maybe now might prove a suboptimal time to buy an index fund loaded with near record amounts of loss-making firms!

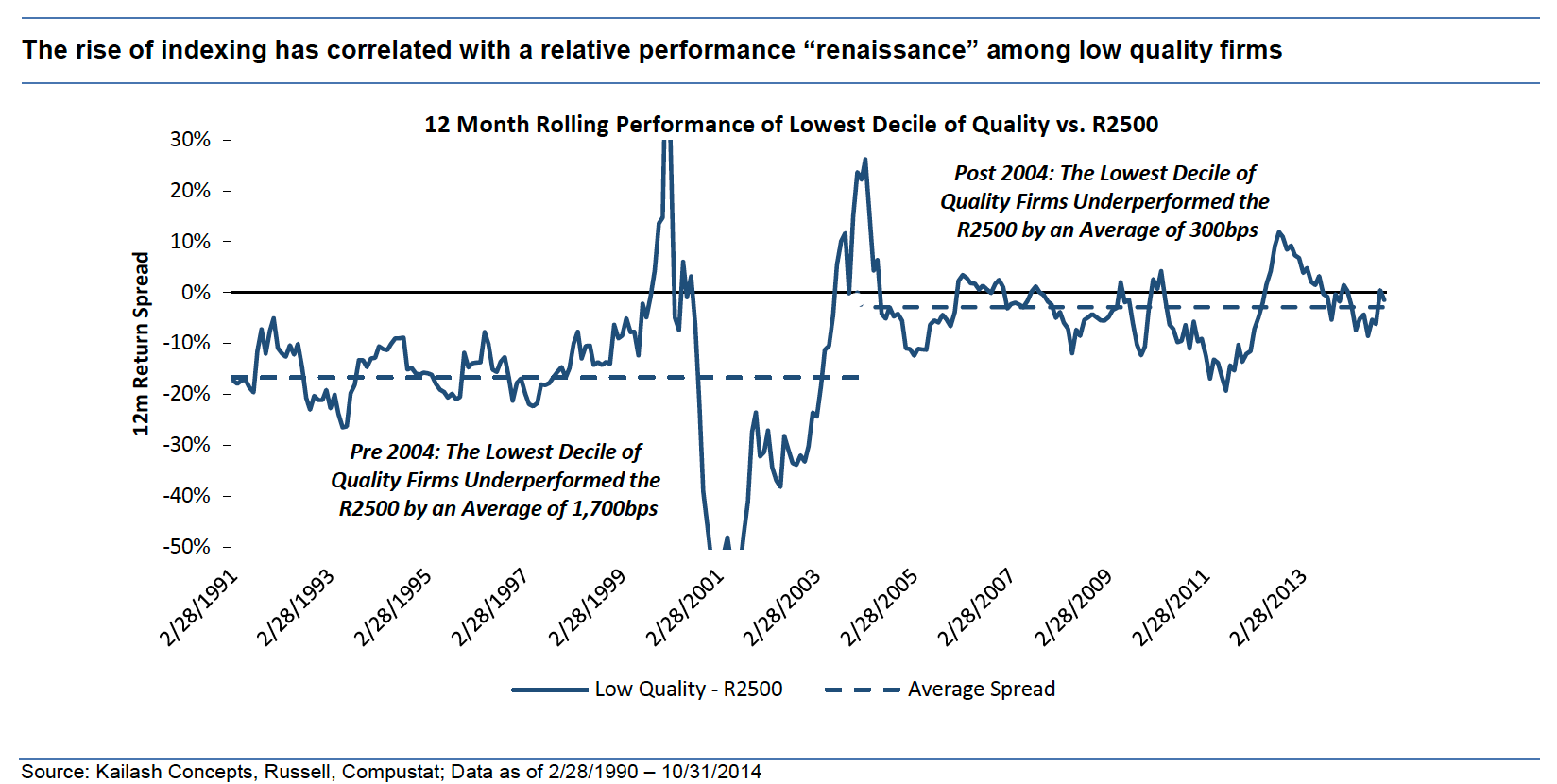

5) The “age of indexing” since 2004 has been highly correlated with atypically good stock performance of low quality firms.

- Please see the full paper that follows for important disclaimers and a detailed discussion of this topic. Please contact Bill Roddy from Kailash on 414-298-5268 to learn more about the Kailash platform.

Disclaimer

The information, data, analyses, and opinions presented herein (a) do not constitute investment advice, (b) are provided solely for informational purposes and therefore are not, individually or collectively, an offer to buy or sell a security, (c) are not warranted to be correct, complete or accurate, and (d) are subject to change without notice. Kailash Capital Research, LLC and its affiliates (collectively, “Kailash Capital Research, LLC ”) shall not be responsible for any trading decisions, damages or other losses resulting from, or related to, the information, data, analyses or opinions or their use. The information herein may not be reproduced or retransmitted in any manner without the prior written consent of Kailash Capital Research, LLC . In preparing the information, data, analyses, and opinions presented herein, Kailash Capital Research, LLC has obtained data, statistics, and information from sources it believes to be reliable. Kailash Capital Research, LLC , however, does not perform an audit or seeks independent verification of any of the data, statistics, and information it receives. Kailash Capital Research, LLC and its affiliates do not provide tax, legal, or accounting advice. This material has been prepared for informational purposes only and is not intended to provide, and should not be relied on for tax, legal, or accounting advice. You should consult your tax, legal, and accounting advisors before engaging in any transaction. © 2021 Kailash Capital Research, LLC – All rights reserved.

Nothing herein shall limit or restrict the right of affiliates of Kailash Capital Research, LLC to perform investment management or advisory services for any other persons or entities. Furthermore, nothing herein shall limit or restrict affiliates of Kailash Capital Research, LLC from buying, selling or trading securities or other investments for their own accounts or for the accounts of their clients. Affiliates of Kailash Capital Research, LLC may at any time have, acquire, increase, decrease or dispose of the securities or other investments referenced in this publication. Kailash Capital Research, LLC shall have no obligation to recommend securities or investments in this publication as result of its affiliates’ investment activities for their own accounts or for the accounts of their clients.

January 17, 2015 |

| Authors: Matthew Malgari, Nathan Przybylo, Dr. Sanjeev Bhojraj and John Durkin

January 17, 2015

Authors: Matthew Malgari, Nathan Przybylo, Dr. Sanjeev Bhojraj and John Durkin