Earnings Quality and Stock Returns with Value as a Tailwind

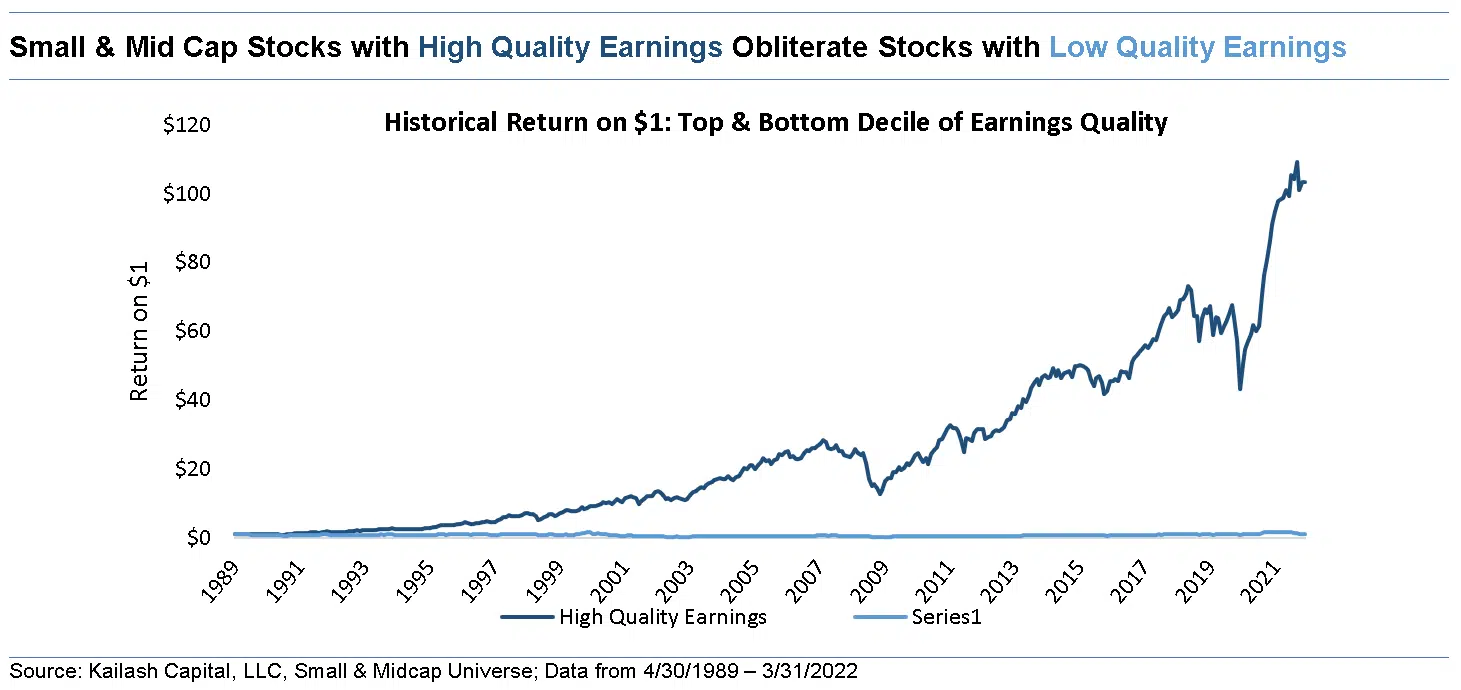

In April last year, KCR penned What is Accounting Quality and Why it Matters. The work discussed the abysmal state of financial reporting and used our earnings quality score to demonstrate that high-quality firms trounced low-quality firms’ performance.

The Art of Stock Picking Returns

“We’ve had 40+ years where all the money went into broadband, or internet, or Netflix or the cloud and no money went into basic productive capacity…” -Robert Friedland, CEO, Ivanhoe group of companies “During the latter stage of the bull market in 1929, the public acquired a completely different attitude towards

Cash Flow to Stockholders is Defined As: Misleading?

How the Crypto-FTX-Fraud Could be Masking Epic Capital MisallocationAccounting Tools states that cash flow to stockholders is the amount of money a firm pays its equity owners. They explain that “Investors routinely compare the cash flow to stockholders to the total amount of cash flow generated by a business…”

The Role of Critical Minerals in Clean Energy Transitions

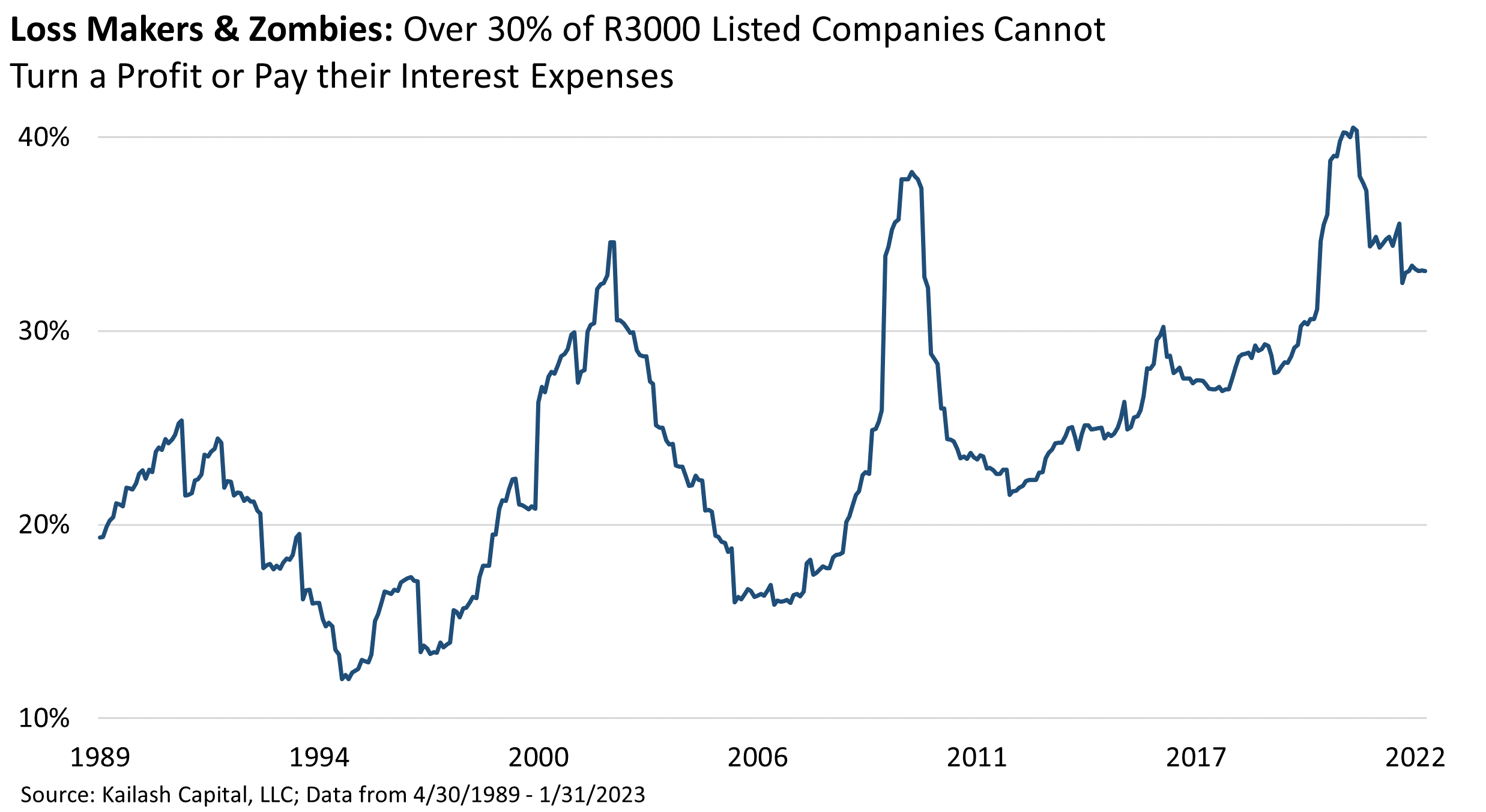

Have Policy-Makers Given Investors a Secular Growth Story for Cyclical Stocks? Our research is empirically based and tends towards places that are uncomfortable and out-of-favor. In 2020, as investors gorged on crypto, loss-making tech and growth stocks of dubious merit..

Small Cap Investing Strategies, Large Caps & Active Management

Welcome everyone, my name is Matt Malgari. Today’s presentation is going to be an update on the bull case for high..

Welcome everyone, my name is Matt Malgari. Today’s presentation is going to be an update on the bull case for high..

Inflation is Taxation without Legislation or Representation

The Cash Crucible & the Acceleration of Financial Repression - “Cash is a Legitimate Asset Class for the First Time in Decades, Investors are piling into products that shield them from losses in a rising rate environment.” So said a recent article in Bloomberg. Any headline-hailing investors “piling” into anything should trigger instant paranoia.

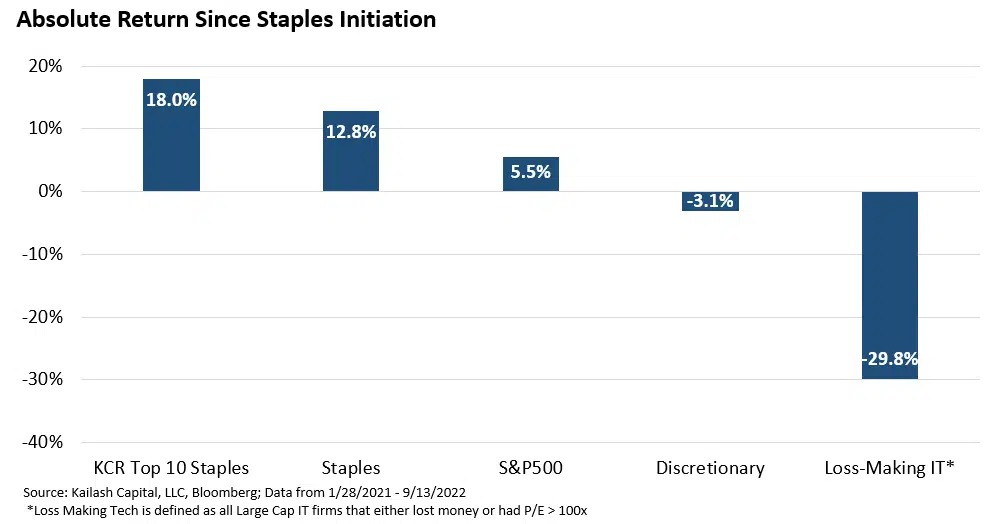

Safe Dividend Stocks: A Staples Update & A Brand New Bag

KCR’s systematic, evidence-based analytical and investment process is driven by the historical record. Our financial faith resides in what the data shows. Human beings have made the same mistakes in slightly different forms again and again for centuries. Stick to a low-cost, tax efficient process and winning is inevitable.

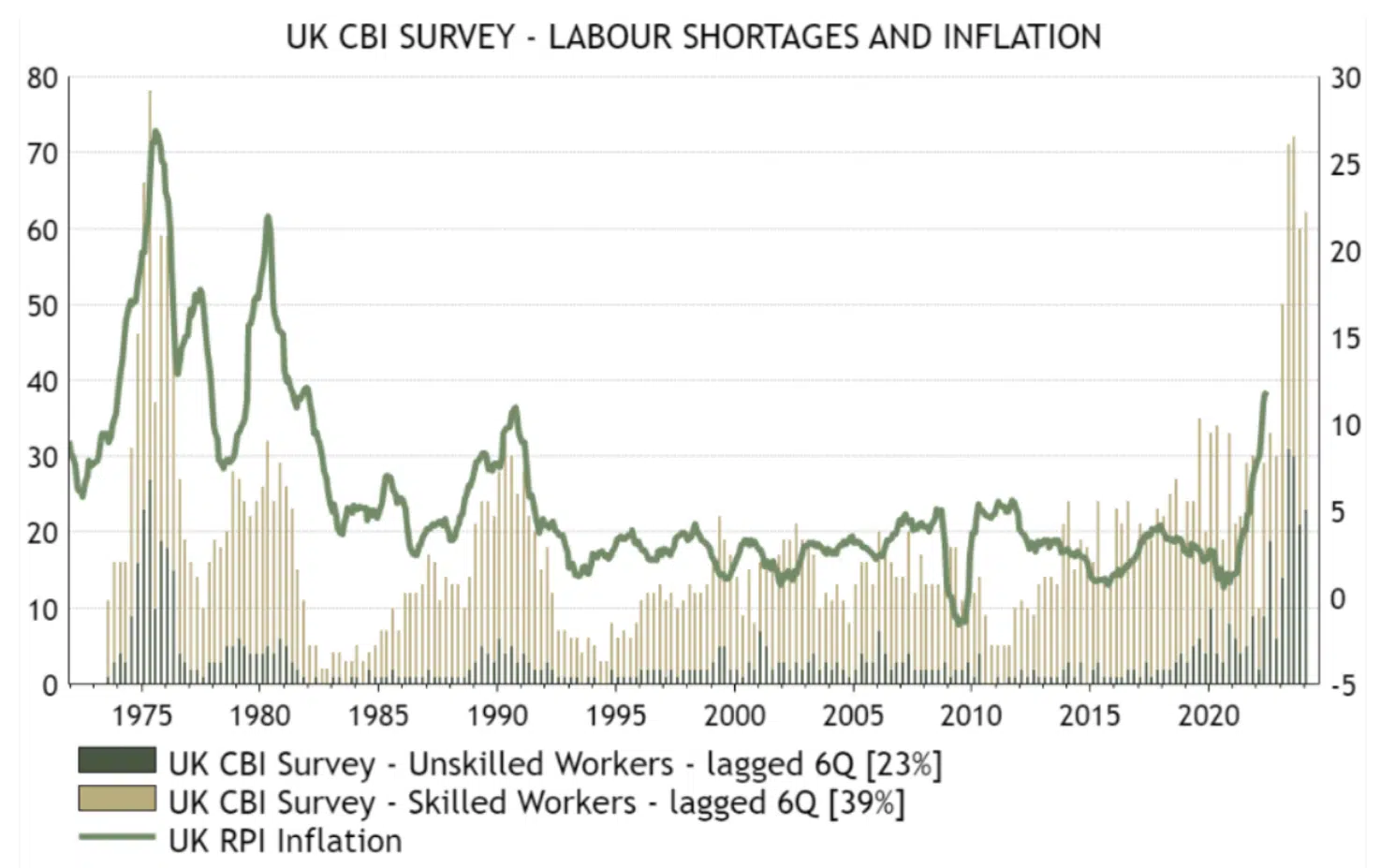

A Tight Labor Market Returns the Upper Hand to American Workers

A Tight Labor Market Returns the Upper Hand to American Workers - The always wonderful John Authers put out a recent piece on inflation. Discussing comments out of the UK, he observed, “I cannot remember a central bank of a large, industrialized country being this negative about its own economy.”

Market Neutral Strategy: Transcript & Video

At KCR, we believe in solving problems and one of the greatest issues we hear from subscribers is how to compound...

At KCR, we believe in solving problems and one of the greatest issues we hear from subscribers is how to compound...

Economic Cycles and Mean Reversion

In 1999, Warren Buffett gave a rare explanation of why he felt the stock market would generate poor returns for investors over the long haul. He used simple arithmetic to show that elevated valuations and profit margins made equities vulnerable. The piece was 9 pages, over 4,000 words long, and had a single exhibit.

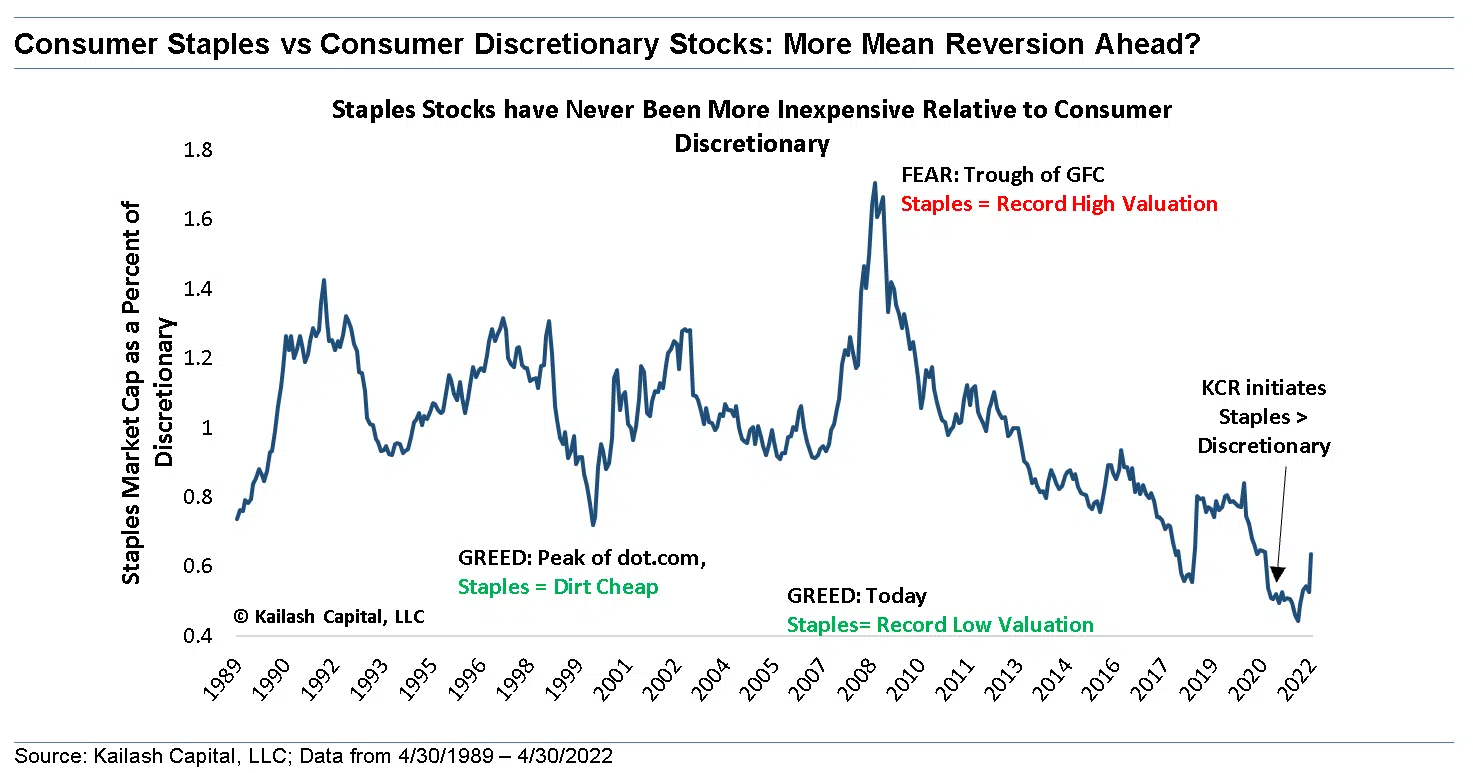

Consumer Staples Sector: A Speculative Refuge

Protecting & Growing Wealth in the Age of Uncertainty - From 2017 - 2020, speculative trading on predatory apps like Robinhood became a true stock market mania. The catastrophic misallocation of capital was, briefly, a very profitable endeavor. We did not flinch.

What Is Accounting Quality and Why It Matters

A Quick Walk Through the Recent Age of Miracle, Wonder & Other Lies - It has been a wild couple of years for financial statements. And by “wild,” we mean the quality of financial accounting information hit lows we could not have imagined. Let’s start with the basics.