Today’s presentation is going to be an update on the bull case for high quality small cap stocks we made in May of 2021. In that May 2021 piece, we highlighted the following three key factors that endeared us to small caps in general, but particularly to KCR’s Small Cap Model portfolio.

(Please view KCR’s Small & Mid Cap Portfolio – Nov 2022 at the bottom of the transcript.)

Slide 2 – DISCLAIMER

First, we explained that the spread in raw market cap between large cap and small cap stocks was bouncing off a three standard deviation low

Second, we highlighted the hugely problematic nature of large cap indexes which featured valuations that were, at the time, significantly above the levels seen at the peak of the internet bubble

Third, we highlighted the power of KCR’s Small Cap Model portfolio vs. the Russell 2000, expressing our now long held and much discussed belief that the small cap indexes are deeply flawed constructs bloated with overpriced loss-making companies.

Slide 3 – Agenda

Over the course of this presentation, we will quickly update you on every one of these items per the agenda you see here. We are going to show how the recent sell-off has materially improved the case for KR’s small cap model portfolio. Before we do that, I think it is really important for us to acknowledge what we got right and what we got wrong.

Slide 4 – Small Cap vs. Large Cap: Update & Mea Culpa

As money managers ourselves, KCR does not believe in hiding and there is no doubt that we came off the blocks too early on this view. The chart below shows the following:

1. First bar: the return of the Russell 2000 since our May 2021 call is -17%, so small caps in aggregate have taken a beating

2. Second bar: the model portfolio we pointed our readers to has only fallen -9%, and while that does mean our model has given the Small Cap Index a profound drubbing, there is no denying that, since our call in May of 2021….

3. Third bar: our small cap portfolio has underperformed the large cap index by about 1%

So net net, certainly not our finest moment but certainly not our worst. Having said that, let’s walk through the evidence and see if you believe, as we do, that the case for small caps – and specifically KCR’s model portfolio – has merely improved.

Note for slide four: “small cap stocks” are generally stocks with market capitalizations that are under $10bn for the purposes of this presentation. In terms of benchmarking, we use the Russell 2000 Index as our choice of small cap index for comparative purposes. KCR’s Small Cap Universe may, at times, differ somewhat materially from the constituents in the Russell 2000 due to our demanding set of data minimums for stock inclusion in our ranking models. When discussing large cap stocks, we are referencing the R1000.

Slide 5 – A Simple Small Cap Strategy

This slide just takes the total market cap of the Russell 2000 and divides it by the Russell 1000. When the line is at the lower end of its range, it indicates that the aggregate market cap of small stocks is very low when compared to the aggregate market cap of large cap stocks.

You can see that, over the long-term, the series tends to swing between highs of around 13% or 14% and dead lows of around 6%. You can see where we initiated these views back in May 2021, and you can see that as small caps have fallen faster than large caps, the ratio has moved back out to near the all-time record wides.

While a simple metric, this ratio of smaller vs larger companies’ market caps offers us a basic reference point regarding good and bad times to invest in small cap companies.

To give you a sense of how powerful even a mundane chart like this can be, we can look at the first time the ratio troughed at about 6%, that was on November 30th of 1990. Over about the next four years, through October 31 of 1994, small caps would double, putting up annualized returns over 19% a year – roughly double that seen by large cap stocks.

If we look at the last time small caps hit the 1 standard deviation low vs. large cap during the dot com bubble, that was on May 31 of 2000. Over the next 6 years small caps would rise over 61% which is an 8.5% annual return over that 6-year window vs. Large Caps, which were flat over that period. Large cap earned you a near-meaningless 1.7% total over 6 years. And that is important as today looks like a far more extreme variant of that unhealthy dynamic than it does the earlier one seen in 1990.

Slide 6 – Valuations: Headwinds for Large Cap

Small Cap Investing Strategies: Why Now & What’s Wrong with Large Cap Indexes?

Moving forward we are going to be revisiting concepts that are rooted in basic arithmetic fact that we have covered in detail in past pieces. The first is Buffett’s market cap to GDP metric. You can see in the chart below the market cap to GDP of the Russell 1000 since the late 1970s.

Despite the recent sell-off, large cap stocks are still valued as richly as they were at the peak of the dot.com mania. For active managers in the space this is good news as much of our recent work has highlighted the abundance of opportunities that lay within this bloated and expensive index.

Unfortunately, as this next slide shows, we are still in uncharted territory.

Slide 7 – Valuations: Headwinds for Large Cap

This scatter plot shows you the 10-year average annual return of the Russell 1000 Index on the vertical axis subsequent to the valuation at the time of investment as defined by market cap to GDP which is on the horizontal axis.

Let’s look at the dot.com peak in 2000. At the peak, the Russell 1000 traded at a record 145% of GDP. If you bought the index there, over the next decade you ended up making no money for a decade. What this chart does not show is the brutal drawdowns and ruthless volatility along the way.

No look to the right – that’s where we are today. Again, even after the sell-off, large caps, in aggregate, are really expensive. Buffett’s valuation tool suggests you will, again, likely earn no returns over a decade.

For those that want to push back, we want to hear from you. We’ve written entire papers about this valuation metric, discussed the narrative that globalization somehow makes it different this time and even built out a simple four factor calculator that approximates a more sophisticated version of this simple guidepost.

In the interests of time, let’s move on to see what this venerated metric suggests for small cap strategies.

You can find a simple walk-through in our post Warren Buffett’s Market Cap to GDP. Economic Cycles and Mean Reversion offers a detailed note explaining how profit margins, globalization and interest rate risk impact Buffett’s valuation metric. Finally, you can click on our S&P 500 Calculator for Warren Buffett’s Valuation Spreadsheet which allows you to plug in four simple estimates of your own for growth, interest rates, margins and multiples so get a 10 year price return calculation.

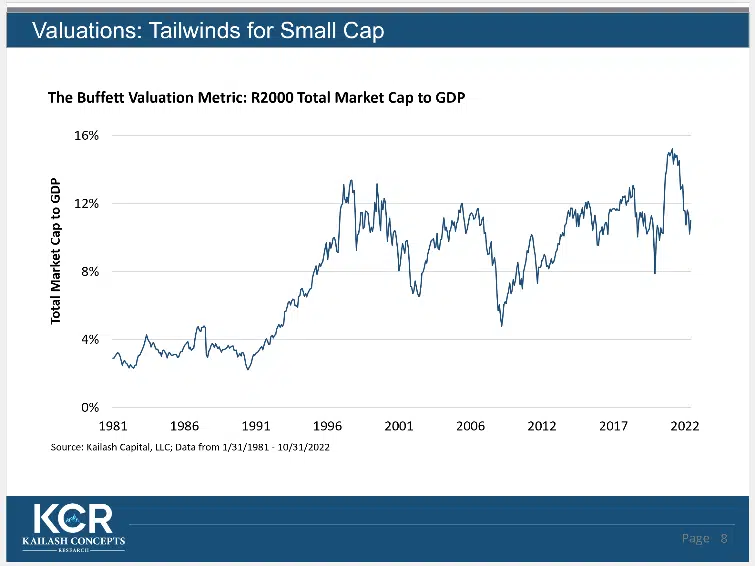

Slide 8 – Valuations: Tailwinds for Small Cap

You can see in this picture that the market cap of small caps looks roughly in-line with its average since the mid 1990s

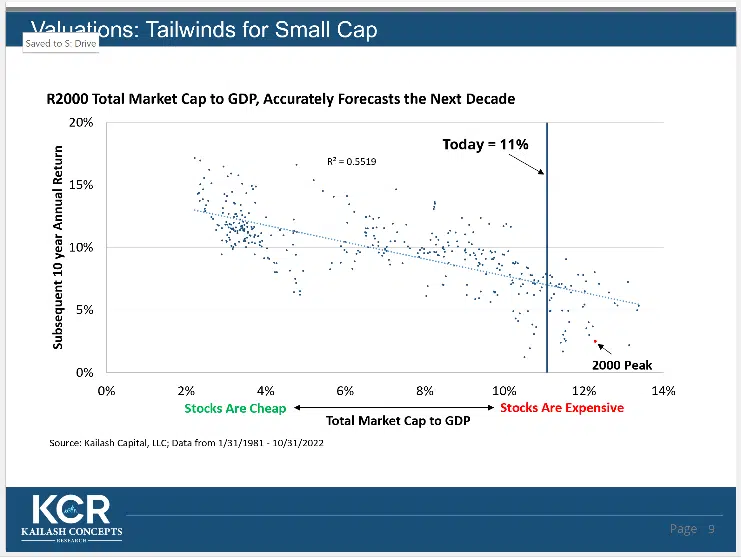

Slide 9 – Valuations: Tailwinds for Small Cap

The good news is in this chart. This is the same scatter plot as for large cap. 10 year annual returns on the vertical axis and valuation expressed as market cap to GDP across the horizontal axis. We would note a couple things: 1) the “fit” in this chart for small caps is nowhere near as tight as it is in large caps meaning the margin of error is wider here and 2) that makes both intuitive and empirical sense.

For the mega cap stocks that dominate large cap indexes, it is very hard to grow much faster than GDP. In contrast, small stocks can take share from each other and, possibly most importantly, they can become the leviathans of tomorrow.

If you haven’t read it, we’d encourage you to check out our post Apple II Flashback, the Fantasy of Predicting the Future. In it we walk readers through the tortured history of Apple. It is easy to forget that as recently as 1997 Apple was a lowly small cap value!

That is exactly what we see in the below. Unlike large caps which offer you a 0% return over the next decade, based on history, small cap valuations today should offer you something around an average of 7% a year. Even if we put a +/-2.5% range on that average, we’d suggest that’s a heck of a lot better than what you’re likely to get in a large cap index.

Slide 10 – Valuations: Headwinds and Tailwinds

These last couple charts tackle valuation through the more traditional lens of price to sales. The chart below shows the following:

• Navy Blue Line: The price to sales ratio of the Russell 1000, which has just fallen below the dot.com peak level

• Light Blue Line: The price to sales ratio of the Russell 2000 which is right around 1x – about the same level as during the dot.com peak when the index would go on to compound at 8.5% a year for six years while large caps did nothing and

• Black Line: This line is the price to sales ratio of KCR’s Small Cap portfolio. Our firm was founded in 2010 so everything prior to that is hypothetical while everything after that represents a period of continuous production

One of the key items we would like to draw your attention to is the KCR model portfolio. Not only is it trading at a massive discount to both the Russell 1000 and Russell 2000, at just 0.5x sales, these stocks are about as cheap as any time in its history on an absolute basis.

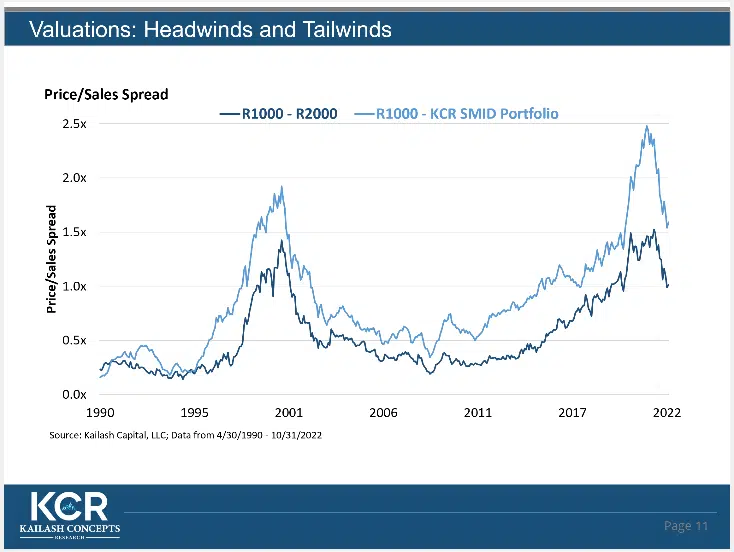

Slide 11 – Valuations: Headwinds and Tailwinds

So, in this chart

The navy blue line deducts the P/S ratio of the Russell 1000 from the P/S ratio of the Russell 2000.

The light blue line deducts the P/S ratio of the Russell 1000 from the P/S ratio of our Small Cap Model.

What’s remarkable is the spread between large caps and our small cap portfolio. They are still vast, and we believe this speaks to the remarkable dispersion on valuation and quality within small caps that our proprietary tools are capturing.

Slide 12 – Valuations: Headwinds and Tailwinds

This is our last chart. Promise. This is the FCF Yield of our Small Cap model portfolio. You can see that our portfolio currently has a FCF yield in excess of 10%. This is in small caps. These are companies with huge headroom to grow.

For those of you wondering about that comical looking spike to 25% that is the GFC crash. And there are two things we’d like to highlight for those in the crowd predisposed to doom:

1. That spike really did happen, our small cap portfolio fell -48% from the peak in 2007 to the trough in 2009

2. that performance almost perfectly matched the Large Cap and Small Cap Indexes which fell -51% and -52% respectively as correlations went to “1” and the world collapsed, but

3. our stocks truly were grossly mispriced and would rise a stunning 94% and 163% over the following one and two years respectively, numbers which nearly doubled the large-cap index

Slide 13 – Fundamentals

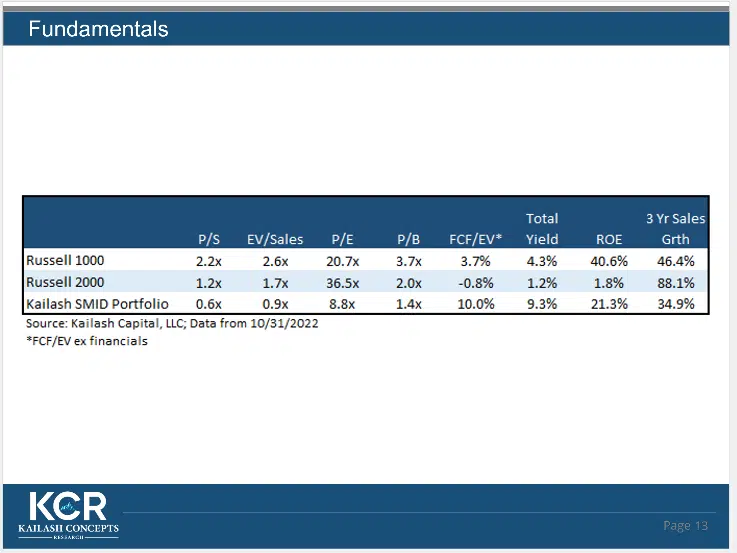

History doesn’t exactly repeat of course, but if you are a doomster and believe we are facing a GFC type credit event, then KCR’s small cap portfolio does not have a history of being some stellar hiding place. What it does suggest, however, is that while the companies we tend to own may get swept down in a cataclysmic arc should one occur, they really are the survivors.

The fundamental panel below shows the simple valuation and quality metrics of the Russell 1000, Russell 2000 and KCR’s Small Cap model portfolio. We think the message at the outset of this presentation rings the bell for small caps in general but that the real money is made by those willing to engage in low-cost, systematic processes predisposed to high quality firms with robust fundamentals and healthy growth.

I’d like to close with a general comment about markets today. The media floods us with stories about record divisiveness and political angst in this country and at times it can feel like our country is in trouble. Students of history, however, will be quick to remind us we have been in tough places before. This is nothing new. I’d also encourage people to talk to their neighbors – its been my experience that we have a lot more in common than many would like us to believe.

While highly imperfect, American capitalism characterized by the innovative and dynamic nature of our people has proven to be a fruitful place for those looking to build success out of their garages.

As one of our longest and most successful investors and partners is fond of reminding me: “Matt don’t let people complicate things for you – build an equal to better product than what’s out there, charge less for it and little companies become big companies. That’s capitalism.”

We believe America is as good a place as any for exactly that and we believe select US Small Caps represent one of the most compelling opportunities since the depths of the GFC on an absolute basis. Even more important for those that must deploy capital, we believe the dispersion between the large cap indexes and high-quality small caps available today has never looked better.

Slide 14 – Appendix

(Please view KCR’s Small & Mid Cap Portfolio – Nov 2022 at the bottom of the transcript.)

Disclaimer

The information, data, analyses, and opinions presented herein (a) do not constitute investment advice, (b) are provided solely for informational purposes and therefore are not, individually or collectively, an offer to buy or sell a security, (c) are not warranted to be correct, complete or accurate, and (d) are subject to change without notice. Kailash Capital Research, LLC and its affiliates (collectively, “Kailash Capital Research, LLC ”) shall not be responsible for any trading decisions, damages, or other losses resulting from, or related to, the information, data, analyses or opinions or their use. The information herein may not be reproduced or retransmitted in any manner without the prior written consent of Kailash Capital Research, LLC . In preparing the information, data, analyses, and opinions presented herein, Kailash Capital Research, LLC has obtained data, statistics, and information from sources it believes to be reliable. Kailash Capital Research, LLC , however, does not perform an audit or seek independent verification of any of the data, statistics, and information it receives. Kailash Capital Research, LLC and its affiliates do not provide tax, legal, or accounting advice. This material has been prepared for informational purposes only and is not intended to provide, and should not be relied on for tax, legal, or accounting advice. You should consult your tax, legal, and accounting advisors before engaging in any transaction.

Nothing herein shall limit or restrict the right of affiliates of Kailash Capital Research, LLC to perform investment management or advisory services for any other persons or entities. Furthermore, nothing herein shall limit or restrict affiliates of Kailash Capital Research, LLC from buying, selling, or trading securities or other investments for their own accounts or for the accounts of their clients. Affiliates of Kailash Capital Research, LLC may at any time have, acquire, increase, decrease or dispose of the securities or other investments referenced in this publication. Kailash Capital Research, LLC shall have no obligation to recommend securities or investments in this publication as a result of its affiliates’ investment activities for their own accounts or for the accounts of their clients.

© 2022 Kailash Capital Research, LLC – All rights reserved.