Bitcoin, Bubbles & BS

In our prior Quick Take, your author threw his 11-year-old daughter to the proverbial wolves in the interests of defending the common-sense investment principles Kailash holds dear. Derived from best-of-breed research in behavioral finance, our models look to find mispriced quality. Our research leans heavily on the historical record that buying good to great companies at reasonable prices is a terrific way to compound wealth. Unfortunately, the last few years have made such a philosophy painful to practice as investors engage in rampant speculative buying of low-quality stocks.

One of our partners recently used the Nasdaq performance since 1995 as a means of recommending, of all things, Bitcoin. Despite vast amounts of reading on the topic, this newsletter has recused itself from the frenzied battle over cryptocurrency. In summary, we have brilliant friends on both sides of the “aisle” so to speak, who either believe it is headed for $1ml per coin and destined to wipe out government money and others who believe it is a total fraud underpinned by leverage and speculation. When it comes to the potential innovative value of cryptocurrencies, Kailash holds a view akin to Switzerland’s foreign policy: neutrality!

Get our insights direct to your inbox: SUBSCRIBE

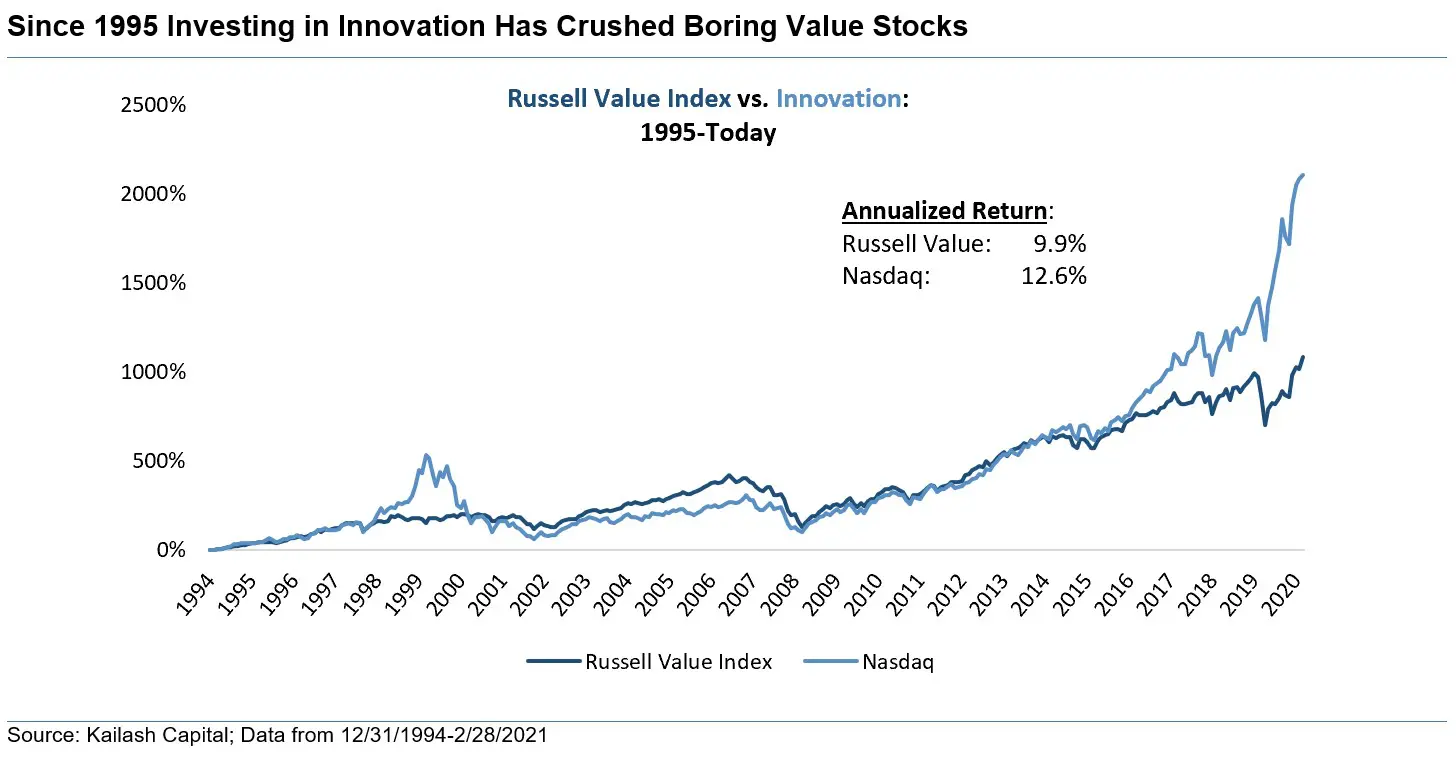

One thing we do have some confidence in is our data on equities. In using the Nasdaq as a “pro-Bitcoin” analogy, our friend suggested that in Bitcoin, as in tech innovators, traditional mean reversion did not apply due to the exponential economics of many tech firms. While acknowledging price volatility, the larger point was that the dot.com bubble of 2000 was but a blip in a return series that yielded fantastic results.[1] The chart below shows the returns to the Nasdaq in light blue and the R1 Value Index.

Summarily, Kailash is sympathetic to backwards looking research that benefits from hindsight bias. Similar to our work on the Nifty Fifty however, if you look at a return series over 20+ years, even intolerable volatility seems acceptable. Kailash suspects much of the world could invest with perfect hindsight. Looking at the below exhibit, our friend’s opinion certainly seems compelling. Look at the fantastic returns that came from investing in the Nasdaq vs. lowly value stocks. Innovation and exponential economics do indeed appear to drive outsized returns.

Get our White Papers direct to your inbox: SUBSCRIBE

Banging the Buffet & Munger Drum: (aka, calling bullsh!t on today’s bubble)

In a recent missive, Kailash reminded readers that Warren Buffett’s investment in a utility company at the height of the dot.com bubble had managed to give customers better rates and make Iowa an entirely green state, all while sinking untold billions into building badly needed grid infrastructure. Buffett also made investors a fortune. Annual profits from investing in that obscenely boring and uninteresting utility in 2000, a period blessed with many disruptive and innovative stocks, led to a situation where Berkshire earned 150% more in a single year (2020) than they paid for the company in 2000. Our decision to highlight Buffet & Mungers’ countercyclical investment style stemmed from our faith in capitalism, America, and the common-sense practice of paying reasonable prices for good businesses.

We believe much of today’s innovation-based wealth is similar to that of the dot.com bubble – based on exorbitant valuations ascribed to stocks with dubious fundamentals. As we have discussed in the past, we believe this is particularly true in the Electric Vehicle space. While stunning leaps forward in technology and product, like the new lineup from Rivian found here, do exist, there have been some bad actors. The folks at Hindenburg Research[2], Michael Lewitt at The Credit Strategist, David Einhorn, Jim Chanos, and many other legendary investors have taken the bubbly component of BEVs to task. Overall, much Electric Vehicle wealth creation has come from the perception that this purported innovation will wipe out existing industries and lead to exponential profits.

In the meantime, Warren Buffett, investing legend, has been maligned again today as he was in 2000. Believing that investors are making the same mistakes (arguably only worse) than in 2000, it is our full intention to merely beat the “Buffett-Munger” drum ever louder. The quotes below represent a partial explanation of how Buffett explained that investing in the “next big thing” is often great for society but not so great for investors. Sourced from Alice Schroeder’s brilliant biography, which we intend to lean on again, Buffett’s remarks were made in a presentation at Sun Valley Idaho in 1999 to many recently minted billionaires from the dot.com bubble.

I will be talking about pricing stocks, but I will not be predicting their course of action next month or next year. Valuing is not the same as predicting. In the short run, the market is a voting machine. In the long run, it’s a weighing machine. Weight counts eventually. But votes count in the short term. And it’s a very undemocratic way of voting. Unfortunately, they have no literacy tests in terms of voting qualifications, as you’ve all learned.

… auto companies: the most important invention, probably, of the first half of the twentieth century. It had an enormous impact on people’s lives. If you had seen at the time of the first cars how this country would develop in connection with autos, you would have said, “This is the place I must be.” But of the two thousand companies, of a few years ago, only three car companies survived. …

Now the other great invention of the first half of the century was the airplane. In this period from 1919 to 1939, there were about two hundred companies. Imagine if you could have seen the future of the airline industry back there at Kitty Hawk. You would have seen a world undreamed of. But assume you had the insight, and you saw all of these people wishing to fly and to visit their relatives or run away from their relatives or whatever you do in an airplane, and you decided this was the place to be.

As of a couple years ago, there had been zero money made from the aggregate of all stock investments in the airline industry in history. So I submit to you: I really like to think that if I had been down there at Kitty Hawk, I would have been farsighted enough and public-spirited enough to have shot Orville down. I owed it to future capitalists.

-Buffett Presentation, Sun Valley Idaho, 1999 (bold emphasis ours)

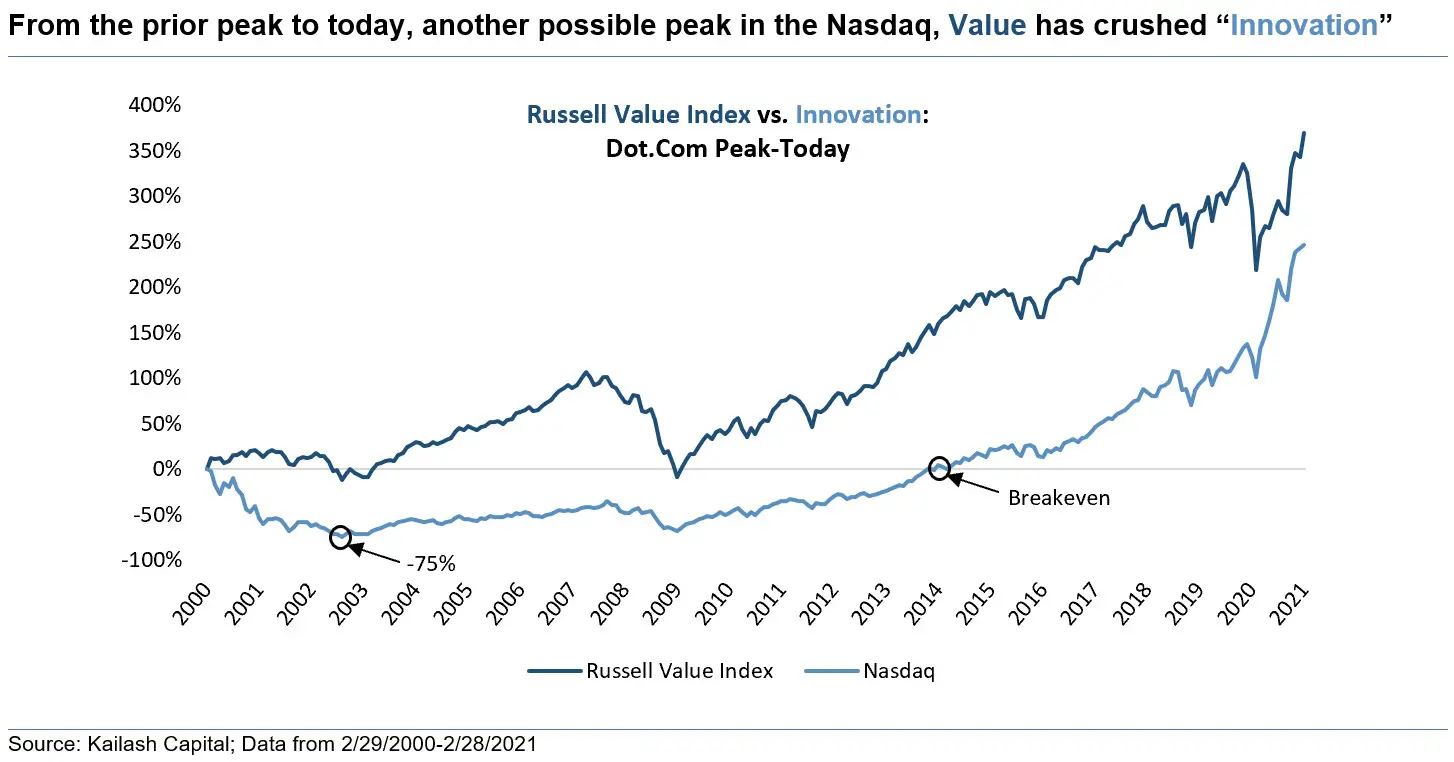

Taking a cue from the wisdom freely on offer from both history in general and the Buffett & Munger duo, Kailash asks its wonderful readers to revisit the issue of “Innovation” vs. “Value.” The chart below is identical to the one on the first page – the only difference? We moved the start date forward to from 1995 to 2000. As this publication has documented extensively here, here, here, and many other places, the market today is as expensive if not more expensive than at the peak of the internet bubble.

Revisiting the returns to the “exponential innovators” and comparing them to prosaic value stocks from 2000 through today is instructive. As we documented in our piece on the hazards of Predicting Progress, even if you have the fundamental thesis right, at too high a price bad things happen. Let’s assign some probability to the views of legendary investors and researchers like GMO, Yale University, Goldman Sachs, Carl Icahn, Stan Druckenmiller, and Warren Buffett, who all have said directly and indirectly: stocks are very expensive. That would mean that the chart below represents the peak-to-peak returns for investing in value and innovation as captured by the Nasdaq.

Even more important – Kailash encourages readers to stare at the returns to INNOVATION. As we have documented repeatedly, there are many innovative tech and clean tech stocks valued at multiples that dwarf those seen at the peak of 2000. Owners of the Nasdaq would have had to hold on through an ~80% drawdown and waited 14+ years to break even. Even more remarkable, Value has crushed Innovation from peak to peak!

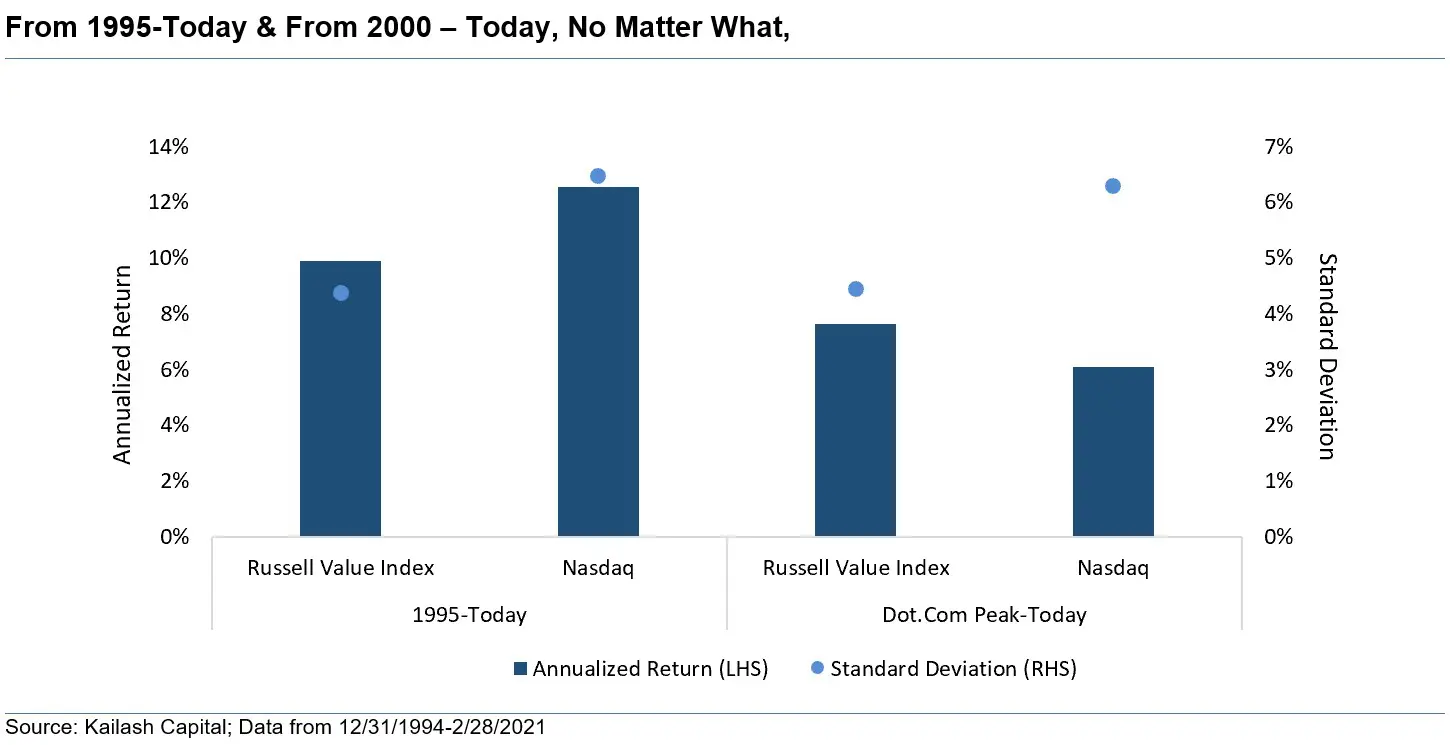

The chart below summarizes the data from the previous two charts as follows:

- 1995-Today: The left two bars show the annualized returns to Value and Innovation

- The bubble on the bars show the volatility of those returns over the 1995-today period

- Even cherry-picking a period where the Nasdaq beat Value Investing, you achieved 20% higher returns but had to endure 50% higher volatility by betting on Innovation

- Dot.Com Peak – Today: The two bars on the right show the annualized returns to Value and Innovation

- Over this period, peak to possible peak, Value generated vastly higher returns with a fraction of the volatility

Let’s circle back to the beginning: are returns to the Nasdaq, the presumed proxy for access to the “exponential” growth of technology, better than dumb old value? The history books suggest that investing in innovation is difficult and volatile at best, while Value tends to compound in a less dramatic but more reliable fashion. To the degree someone wants to make the case that Bitcoin is a great investment, Kailash suggests they prove how it is nothing like the Nasdaq! Kailash finds it amusing that there are no long-tenured “innovation indexes,” and they tend to come and go with unfortunate timing![3]

Recently, Kailash has written a trove of papers bringing powerful empirical evidence demonstrating that many of the market’s longest-tenured and most profitable firms can be had for below-average multiples. These pieces of research have demonstrated that today looks painfully similar to the peak of the internet bubble. Today, like then, we find that some of the most stable, predictable, and income-producing firms in markets are trading at steep discounts.[4] No matter if it was Part I or Part II of our work on Staples, our work on High Quality Midcaps, or even our highlighting the remarkable opportunity in High Quality Small Cap companies; our work simply cannot stack up to the manic returns to firms perceived to be innovators today.

For investors who believe that capitalism, America, and the very basics of arithmetic will once again reassert themselves on what we believe is an obviously speculative set of equities, please see our GARP research and securities list or possible starting points or any of our vast body of research to find common sense alternatives.

Disclaimer

The information, data, analyses, and opinions presented herein (a) do not constitute investment advice, (b) are provided solely for informational purposes and therefore are not, individually or collectively, an offer to buy or sell a security, (c) are not warranted to be correct, complete or accurate, and (d) are subject to change without notice. Kailash Capital Research, LLC and its affiliates (collectively, “Kailash Capital Research, LLC ”) shall not be responsible for any trading decisions, damages or other losses resulting from, or related to, the information, data, analyses or opinions or their use. The information herein may not be reproduced or retransmitted in any manner without the prior written consent of Kailash Capital Research, LLC . In preparing the information, data, analyses, and opinions presented herein, Kailash Capital Research, LLC has obtained data, statistics, and information from sources it believes to be reliable. Kailash Capital Research, LLC , however, does not perform an audit or seeks independent verification of any of the data, statistics, and information it receives. Kailash Capital Research, LLC and its affiliates do not provide tax, legal, or accounting advice. This material has been prepared for informational purposes only and is not intended to provide, and should not be relied on for tax, legal, or accounting advice. You should consult your tax, legal, and accounting advisors before engaging in any transaction. © 2021 Kailash Capital Research, LLC – All rights reserved.

Nothing herein shall limit or restrict the right of affiliates of Kailash Capital Research, LLC to perform investment management or advisory services for any other persons or entities. Furthermore, nothing herein shall limit or restrict affiliates of Kailash Capital Research, LLC from buying, selling or trading securities or other investments for their own accounts or for the accounts of their clients. Affiliates of Kailash Capital Research, LLC may at any time have, acquire, increase, decrease or dispose of the securities or other investments referenced in this publication. Kailash Capital Research, LLC shall have no obligation to recommend securities or investments in this publication as result of its affiliates’ investment activities for their own accounts or for the accounts of their clients.