- Introduction: Traction in the tails, using fundamental facts to avoid promises and pain

- Exploiting the procyclical nature of M&A

- In the Anti-Algebra Index-Era, M&A makes the case that fundamental facts are worth figuring

- Exhibits

- Appendix: Small and Mid Cap Figures

Introduction: Traction in the tails, using fundamental facts to avoid promises and pain

Over the last seven years the Kailash ranking methodology has faced intermittent criticism for failing to see the “potential” in a recent acquisition after partners of the product have seen some of their favorite stocks show up at the bottom of the rankings file—and on one of the numerous short lists—after a deal. We are frequently told the numbers do not catch the revenue, cost or capex synergies that will soon rain down on the pro forma income statements, or that the vagaries of acquisition accounting are distorting the numbers and the calculation of fundamental metrics rendering them meaningless. We have often been told that we should make adjustments or just remove M&A from the rankings because there is no merit to the analysis. In this paper we will avoid delving into the maze of academic research which we believe does a superb job outlining a number of plausible explanations for the often abysmal post-deal performance of companies. With that said, we would be happy to hear your thoughts and supply relevant research that may help shed light on your particular view from the sea of academic research published on the topic.

Get our White Papers direct to your inbox: SUBSCRIBE

We will start with intuition painfully learned over decades in the industry that not all mergers or acquisitions are created equal, that oftentimes synergies and cost savings are not realized and that the quality of a firm as an investment candidate can best be seen through the dispassionate lens of post-acquisition data. The money managers at Kailash carry deep scars from younger days when they were more easily enamored by the purported skill of a management team’s acumen and the ability to assess such things. In hindsight we have learned to recognize that, like all human beings, we are prone to both overconfidence and overoptimism when it suits our predispositions.

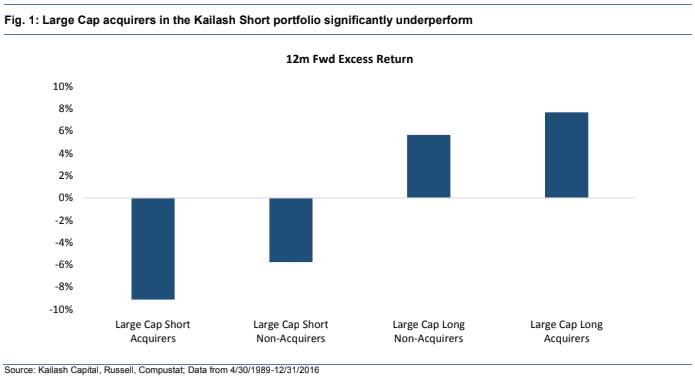

In order to examine whether or not the anecdotal observations would prove out under the merciless lens of historical review, we decided to analyze the constituents of the Kailash monthly short and long picks on the basis of whether or not they had completed an acquisition within the last year and how these firms performed over the next 12 months. We used four buckets for the purposes of our analysis:

- Short Acquirers: stocks in the monthly short picks that had closed an acquisition in the last year

- Short Non-Acquirers: stocks in the monthly short picks that had NOT closed an acquisition in the last year

- Long Non-Acquirers: stocks in the monthly long picks that had NOT closed an acquisition in the last year

- Long Acquirers: stocks in the monthly long picks that had closed an acquisition in the last year

As Figure 1 shows, when the model does not like a post-acquisition equity (first bar) the results are catastrophic with the average Large Cap Short Acquirer underperforming by over 9%. This is a powerful finding as can be seen by the second bar to the right which is how the rest of the stocks in our short book perform. While 6% underperformance is a powerful number for a short, the 9%+ underperformance of the post-acquisition shorts would imply that these firms are an even more fertile area for short-sellers to hunt and an even more precarious group for long-only managers to traffick in. While somewhat less compelling, we would also note that acquirers in the long picks go on to outperform the market by modestly larger amounts than other long picks.

Disclaimer

The information, data, analyses, and opinions presented herein (a) do not constitute investment advice, (b) are provided solely for informational purposes and therefore are not, individually or collectively, an offer to buy or sell a security, (c) are not warranted to be correct, complete or accurate, and (d) are subject to change without notice. Kailash Capital Research, LLC and its affiliates (collectively, “Kailash Capital Research, LLC ”) shall not be responsible for any trading decisions, damages or other losses resulting from, or related to, the information, data, analyses or opinions or their use. The information herein may not be reproduced or retransmitted in any manner without the prior written consent of Kailash Capital Research, LLC . In preparing the information, data, analyses, and opinions presented herein, Kailash Capital Research, LLC has obtained data, statistics, and information from sources it believes to be reliable. Kailash Capital Research, LLC , however, does not perform an audit or seeks independent verification of any of the data, statistics, and information it receives. Kailash Capital Research, LLC and its affiliates do not provide tax, legal, or accounting advice. This material has been prepared for informational purposes only and is not intended to provide, and should not be relied on for tax, legal, or accounting advice. You should consult your tax, legal, and accounting advisors before engaging in any transaction. © 2021 Kailash Capital Research, LLC – All rights reserved.

Nothing herein shall limit or restrict the right of affiliates of Kailash Capital Research, LLC to perform investment management or advisory services for any other persons or entities. Furthermore, nothing herein shall limit or restrict affiliates of Kailash Capital Research, LLC from buying, selling or trading securities or other investments for their own accounts or for the accounts of their clients. Affiliates of Kailash Capital Research, LLC may at any time have, acquire, increase, decrease or dispose of the securities or other investments referenced in this publication. Kailash Capital Research, LLC shall have no obligation to recommend securities or investments in this publication as result of its affiliates’ investment activities for their own accounts or for the accounts of their clients.

January 25, 2017 |

| Authors: Matthew Malgari, Nathan Przybylo, Dr. Sanjeev Bhojraj and John Durkin

January 25, 2017

Authors: Matthew Malgari, Nathan Przybylo, Dr. Sanjeev Bhojraj and John Durkin