As documented in our recent research on high quality midcap investing, growth investing and value investing firms , the mania for index investing has left many of the market’s highest quality and most profitable firms trading at discounts to the market.

Get our insights direct to your inbox: SUBSCRIBE

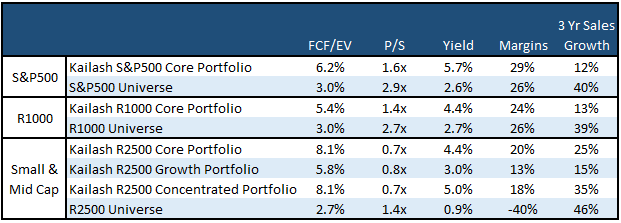

In the box below we show some basic features of our S&P 500, Russell 1000 and Russell 2500 model portfolios vs. their respective benchmarks:

- Our S&P 500 model portfolio has a 6.2% free cash flow yield, trades at only 1.6x sales and yields 5.7% while the S&P has only a 3.0% FCF yield and, at 2.9x sales, is nearly twice as expensive!

- Our R1000 model portfolio is much the same – offering massive advantages in free cash flow and a healthy 4.4% yield for those interested in income investing – a topic we discussed in our research on safe dividend investing and subsequent work on income investing.

- In the Small & Midcap universe we show the properties of our Core, Growth and Highly Concentrated model portfolios vs. the Russell 2500 Index and the results are staggering: our small & midcap portfolios offer compelling yields ranging from 4.4% in our Core portfolio to 5.0% in our Concentrated portfolio – giving investors the potential to not just earn healthy income but to also benefit from the growth and capital appreciation small and midcap stocks are known for.

- Looking at the column titled “Margins” you can see how profitable our portfolio stocks are relative to their benchmarks with the most remarkable feature being that our Russell 2500 Universe has a -40% margin!

- Looking at the last column “3 Year Sales Growth” you can see that all our model portfolios have had lower growth rates over the last three years than their respective universe. For those concerned with these lower growth rates, we hope you read our upcoming piece on income & quality investing using the market’s highest quality and most stable firms – Consumer Staples.

- Kailash would also note that our portfolios’ growth rates are still faster than US GDP growth and that the firms in our model portfolios are achieving this while generating enormous profits and paying healthy yields along the way.

- While growth investing has been all the rage as discussed in our research paper Brilliant to Braindead, which explained the extreme risk involved in buying high growth firms at high valuations like today, Kailash believes that for investors willing to step out of the Indexing Herd, our model portfolios are compelling evidence of the investment opportunities available today.

Get our White Papers direct to your inbox: SUBSCRIBE

Disclaimer

The information, data, analyses, and opinions presented herein (a) do not constitute investment advice, (b) are provided solely for informational purposes and therefore are not, individually or collectively, an offer to buy or sell a security, (c) are not warranted to be correct, complete or accurate, and (d) are subject to change without notice. Kailash Capital Research, LLC and its affiliates (collectively, “Kailash Capital Research, LLC ”) shall not be responsible for any trading decisions, damages or other losses resulting from, or related to, the information, data, analyses or opinions or their use. The information herein may not be reproduced or retransmitted in any manner without the prior written consent of Kailash Capital Research, LLC . In preparing the information, data, analyses, and opinions presented herein, Kailash Capital Research, LLC has obtained data, statistics, and information from sources it believes to be reliable. Kailash Capital Research, LLC , however, does not perform an audit or seeks independent verification of any of the data, statistics, and information it receives. Kailash Capital Research, LLC and its affiliates do not provide tax, legal, or accounting advice. This material has been prepared for informational purposes only and is not intended to provide, and should not be relied on for tax, legal, or accounting advice. You should consult your tax, legal, and accounting advisors before engaging in any transaction. © 2021 Kailash Capital Research, LLC – All rights reserved.

Nothing herein shall limit or restrict the right of affiliates of Kailash Capital Research, LLC to perform investment management or advisory services for any other persons or entities. Furthermore, nothing herein shall limit or restrict affiliates of Kailash Capital Research, LLC from buying, selling or trading securities or other investments for their own accounts or for the accounts of their clients. Affiliates of Kailash Capital Research, LLC may at any time have, acquire, increase, decrease or dispose of the securities or other investments referenced in this publication. Kailash Capital Research, LLC shall have no obligation to recommend securities or investments in this publication as result of its affiliates’ investment activities for their own accounts or for the accounts of their clients.