In our piece, Economic Cycles and Mean Reversion, we discussed how corporate profit margins had risen to levels above the prior century’s peak in 1929. We have updated the chart used in that piece below. These enormous margins have been and continue to be the fundamental bulwark on which much of the bull case for US equities rests.

Get our insights direct to your inbox: SUBSCRIBE

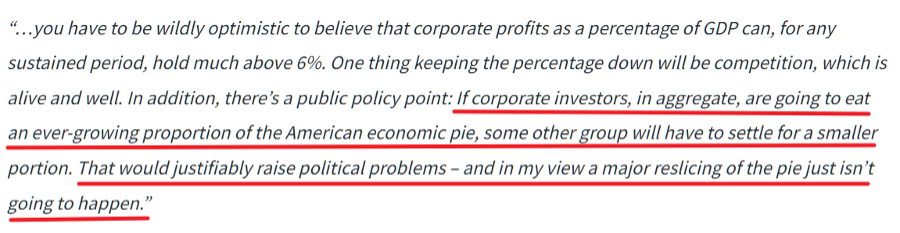

Across numerous pieces of research, we have cautioned that these record margins were sourced from a combustible mix of leverage, falling interest rates, falling labor costs and that all three secular trends could be stalling or ending. The methodologies we used were from a 1999 interview Mr. Buffett gave explaining the algebra he uses to estimate the market’s long-run returns (we built a simple calculator to replicate his thinking you can use here). We quoted Mr. Buffett as follows:

From KCR’s Economic Cycles & Mean Reversion:

So, Mr. Buffett has proven to be very wrong. Margins have soared. A major re-slicing of the pie has, in fact, happened. But we think most would agree that he was correct in his assessment that such a re-slicing has caused political problems.

We have very cautiously brought the issues around “labor’s share of the pie” to our readers’ attention with follow-on pieces like You Will Pay the Plumber and numerous other pieces that suggested the mercenary crews running Private Equity shops have used empirically dubious methods of valuation and reporting to inhale capital and plunder American enterprises.

What we did not do was tread into the murderous and murky waters of political discourse.

In a recent commentary, the always erudite Jesse Felder put out a note highlighting the same Buffett quote noting the emphasis on Buffett’s “…justifiable political problems…”

Explaining that he, like us, typically avoided politics, Mr. Felder then plunged into the void. Using articles from the Wall Street Journal and Financial Times, he demonstrated that there is now bipartisan support for a more equitable distribution of the economic pie. He walks through how politicians have taken notice and are working to help labor on both ends of the political establishment.

Mr. Felder explains that a reversal of the neoliberal economic policies that have dominated the last 30 years could create headwinds to profit margins. Equally interesting is how he ties in research from the State of Wisconsin Investment Board and Robeco to note that the negative correlation of bonds and equities over the past 20 years “…may have already reverted to a more historically normal positive correlation.”

Macro forecasting is not our thing. We avoid it like the plague. But reading Mr. Felder’s logic, one must acknowledge that a major switch in equity and bond correlations is in the probability distribution.

This matters a great deal considering few of the main-stream asset allocation programs we are aware of have assigned much, if any, probability to this outcome. Most are valuation-agnostic and backward-looking, with empirical principles derived from roughly 30 years of data. If someone is aware of a firm with an allocation program that contemplates 1) a longer horizon that 2) embeds the period when bonds and equities were positively correlated, we would be grateful if you would reach out to us.

The implications of all this for everything asset allocators do cannot be overstated. In June 2020, KCR saw that equity valuations were well above the peak of the dot.com bubble and that bond yields were at the lowest levels in history. We penned 60/40 Portfolio: Buying a Ticket on the Titanic, which explained that bonds had become instruments of “return-less risk,” meaning the classic asset allocation model was in trouble.

Since the work was based on simple arithmetic and offered investors a simple method of non-correlated diversification, we thought it anything but controversial. We were wrong. Rather than recognize….math….people got upset with us.

Mr. Felder’s acknowledgment that bonds and equities have historically experienced long periods of positive correlation creates a new and most unwelcome headwind to this consensus method of asset allocation. This is particularly true when we observe the chart below from the always-brilliant Tavi Costa at Crescat. The chart from their recent investor letter shows the yield of a 60/40 portfolio over history.

Disclaimer

The information, data, analyses, and opinions presented herein (a) do not constitute investment advice, (b) are provided solely for informational purposes and therefore are not, individually or collectively, an offer to buy or sell a security, (c) are not warranted to be correct, complete or accurate, and (d) are subject to change without notice. Kailash Capital Research, LLC and its affiliates (collectively, “KCR”) shall not be responsible for any trading decisions, damages, or other losses resulting from, or related to, the information, data, analyses or opinions or their use. The information herein may not be reproduced or retransmitted in any manner without the prior written consent of KCR. In preparing the information, data, analyses, and opinions presented herein, KCR has obtained data, statistics, and information from sources it believes to be reliable. KCR, however, does not perform an audit or seek independent verification of any of the data, statistics, and information it receives. KCR and its affiliates do not provide tax, legal, or accounting advice. This material has been prepared for informational purposes only and is not intended to provide, and should not be relied on for tax, legal, or accounting advice. You should consult your tax, legal, and accounting advisors before engaging in any transaction.

Nothing herein shall limit or restrict the right of affiliates of KCR to perform investment management or advisory services for any other persons or entities. Furthermore, nothing herein shall limit or restrict affiliates of KCR from buying, selling, or trading securities or other investments for their own accounts or for the accounts of their clients. Affiliates of KCR may at any time have, acquire, increase, decrease, or dispose of the securities or other investments referenced in this publication. KCR shall have no obligation to recommend securities or investments in this publication as a result of its affiliates’ investment activities for their own accounts or for the accounts of their clients.

© 2023 Kailash Capital Research, LLC – All rights reserved.

October 5, 2023 |

| Authors: Matthew Malgari, Nathan Przybylo, Dr. Sanjeev Bhojraj and John Durkin

October 5, 2023

Authors: Matthew Malgari, Nathan Przybylo, Dr. Sanjeev Bhojraj and John Durkin