• Introduction: The Drawbacks of Indices Weighted by Market Cap

• Equal Weight and Smart Beta Are at Best Only Partial Solutions

• Cheap & Small: The Success Paradox of Random Monkeys and Upside-Down Strategies

• Kailash Core Model Is a More Effective Solution

• Appendix

Introduction: The Drawbacks of Indices Weighted by Market Cap

With the proliferation of ETFs making outsized promises on simple univariate factors and the soaring popularity of simple 2-4 factor models in gathering assets over the last several years, we have had a number of clients ask us to show the potential benefits and drawbacks of passive and smart beta strategies. We recognize that some clients may use this work to help communicate with retail clients and, with that in mind, hope that our exhibits prove clear and constructive.

Get our White Papers direct to your inbox: SUBSCRIBE

Our primary findings in this paper are the following:

- Passive investing in cap-weighted strategies has historically put investors in large and expensive stocks despite the performance headwinds native to these factors.

- Despite being the simplest form of smart beta, equal weighting represents much of the operational underpinnings of the more complex versions of smart beta and benefits from the same value and size tilts that drive the outperformance of most smart beta strategies.

- While smart beta strategies do show small amounts of outperformance over the long haul within the larger cap space, this outperformance comes at the cost of higher volatility and large excess drawdowns relative to the cap-weighted indices.

- The valuation spreads between cap-weighted and equal-weighted indices are currently low relative to history which may indicate negligible performance differences in the future.

- The performance of size (measured by market cap) correlates closely to an equal-weighted index’s outperformance vs. the cap-weighted index. The high correlation (see Figs. 12 & 13) demonstrates that a significant component of the excess returns to equal-weight strategies are a function of size.

- We believe our Core Model is a more elegant and effective solution for better performance than equal weighting or any smart beta strategy as our Core Model has historically outperformed across all valuation deciles on Sales/Price. In addition, unlike the previously documented data on Smart Beta, the inverse of our Core Model strategy (i.e., our bottom ranked stocks) performs roughly opposite of how our Core Model strategy performs.

While we have enormous respect for the benefits of passive investing, we believe that the concept in practice is in some ways difficult to digest. If a money manager approached investors and said, “Our method is going to require us to be structurally underweight smaller firms despite their tendency to outperform over the long haul and to mechanically increase exposure to firms as they become more expensive,” there would probably not be too much interest. Yet this is a simple expression of the approach pursued by many investors in the passive complex. Passive funds that mimic the most popular market cap-weighted benchmarks like the S&P500 or the Russell 2500 are basically forced to do just that despite it being intuitively suboptimal to take larger and larger positions in companies as they become more expensive—and therefore less attractive—while taking smaller and smaller positions in companies as they become cheaper and therefore more attractive. While it is not necessarily always the case that a rising stock price means that a firm is becoming more expensive—as the fundamentals of the firm could be improving even more quickly than the stock is rising—history tells us it is often the case. This was seen especially during the Tech Bubble of the 1990s when rapidly rising stock prices usually indicated an increasing detachment of the stock price from any fundamental value.

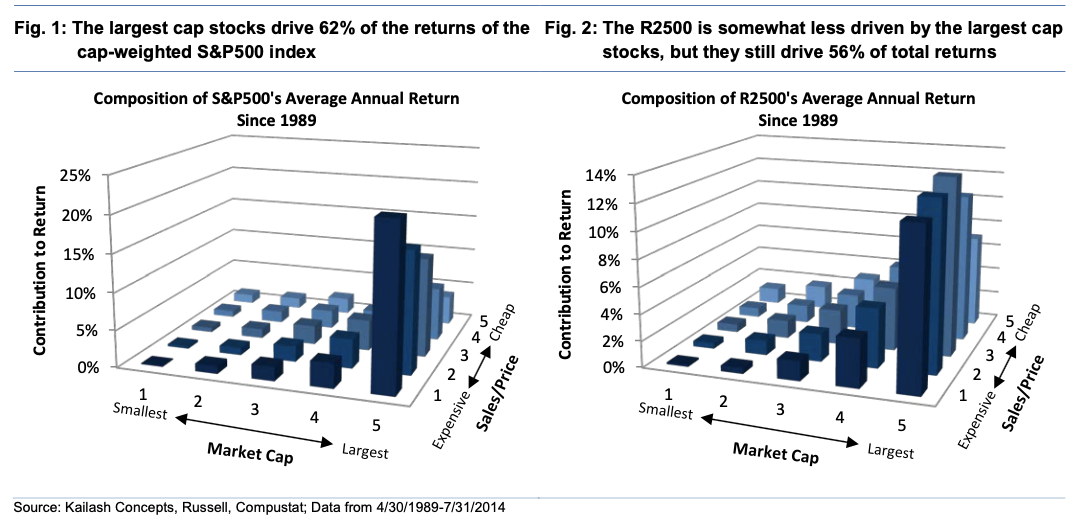

In Figures 1 and 2 below we show the historical contribution to the S&P500’s and Russell 2500’s average annual return sorted by the intersection of size and valuation. What the charts very clearly show is that for both indices, the vast majority of these market cap-weighted returns is coming from the largest quintile of stocks. Historically, the largest 20% of the names has been responsible for 62% and 56% of the S&P500’s and Russell 2500’s average annual returns, respectively. Interestingly, these historical numbers are nearly identical to what we would expect based on current weights within the index as the top 20% of the names in the S&P500 and R2500 represent 63.4% and 55.8% of the index weights, respectively. Even more remarkable, for the S&P500, the most expensive large stocks alone (front right bar in Fig. 1) generated nearly 22% of the benchmark’s absolute average annual return.

Disclaimer

The information, data, analyses, and opinions presented herein (a) do not constitute investment advice, (b) are provided solely for informational purposes and therefore are not, individually or collectively, an offer to buy or sell a security, (c) are not warranted to be correct, complete or accurate, and (d) are subject to change without notice. Kailash Capital Research, LLC and its affiliates (collectively, “Kailash Capital Research, LLC ”) shall not be responsible for any trading decisions, damages or other losses resulting from, or related to, the information, data, analyses or opinions or their use. The information herein may not be reproduced or retransmitted in any manner without the prior written consent of Kailash Capital Research, LLC . In preparing the information, data, analyses, and opinions presented herein, Kailash Capital Research, LLC has obtained data, statistics, and information from sources it believes to be reliable. Kailash Capital Research, LLC , however, does not perform an audit or seeks independent verification of any of the data, statistics, and information it receives. Kailash Capital Research, LLC and its affiliates do not provide tax, legal, or accounting advice. This material has been prepared for informational purposes only and is not intended to provide, and should not be relied on for tax, legal, or accounting advice. You should consult your tax, legal, and accounting advisors before engaging in any transaction. © 2021 Kailash Capital Research, LLC – All rights reserved.

Nothing herein shall limit or restrict the right of affiliates of Kailash Capital Research, LLC to perform investment management or advisory services for any other persons or entities. Furthermore, nothing herein shall limit or restrict affiliates of Kailash Capital Research, LLC from buying, selling or trading securities or other investments for their own accounts or for the accounts of their clients. Affiliates of Kailash Capital Research, LLC may at any time have, acquire, increase, decrease or dispose of the securities or other investments referenced in this publication. Kailash Capital Research, LLC shall have no obligation to recommend securities or investments in this publication as result of its affiliates’ investment activities for their own accounts or for the accounts of their clients.

September 16, 2014 |

| Authors: Matthew Malgari, Nathan Przybylo, Dr. Sanjeev Bhojraj and John Durkin

September 16, 2014

Authors: Matthew Malgari, Nathan Przybylo, Dr. Sanjeev Bhojraj and John Durkin