The Politics of Profits, Volatility Laundering & All-Alts are not Equal

In our piece, Economic Cycles and Mean Reversion, we demonstrated that corporate profit margins had risen to levels above the prior century's peak in 1929. We have updated the chart used in that piece. These margins have been and continue to be the fundamental bulwark on which any bull case for US equities rests.

Citizenship in a Republic: The Man in the Arena

Over nearly 15 years, KCR has never highlighted

The Refinancing Wall Looms Large: When Algebra & Optimism Collide

In our August piece, The Solvency Debate Continues, KCR updated our 2021 missive Junk Stocks Funded by Junk Bonds. We observed that 2023 had seen speculators return with a ferocious appetite for low-quality stocks. Our focus in that piece, and again today, will be on a group of companies that failed the Federal Reserve’s test for financial fragility as defined by interest coverage ratios (“ICRs”).

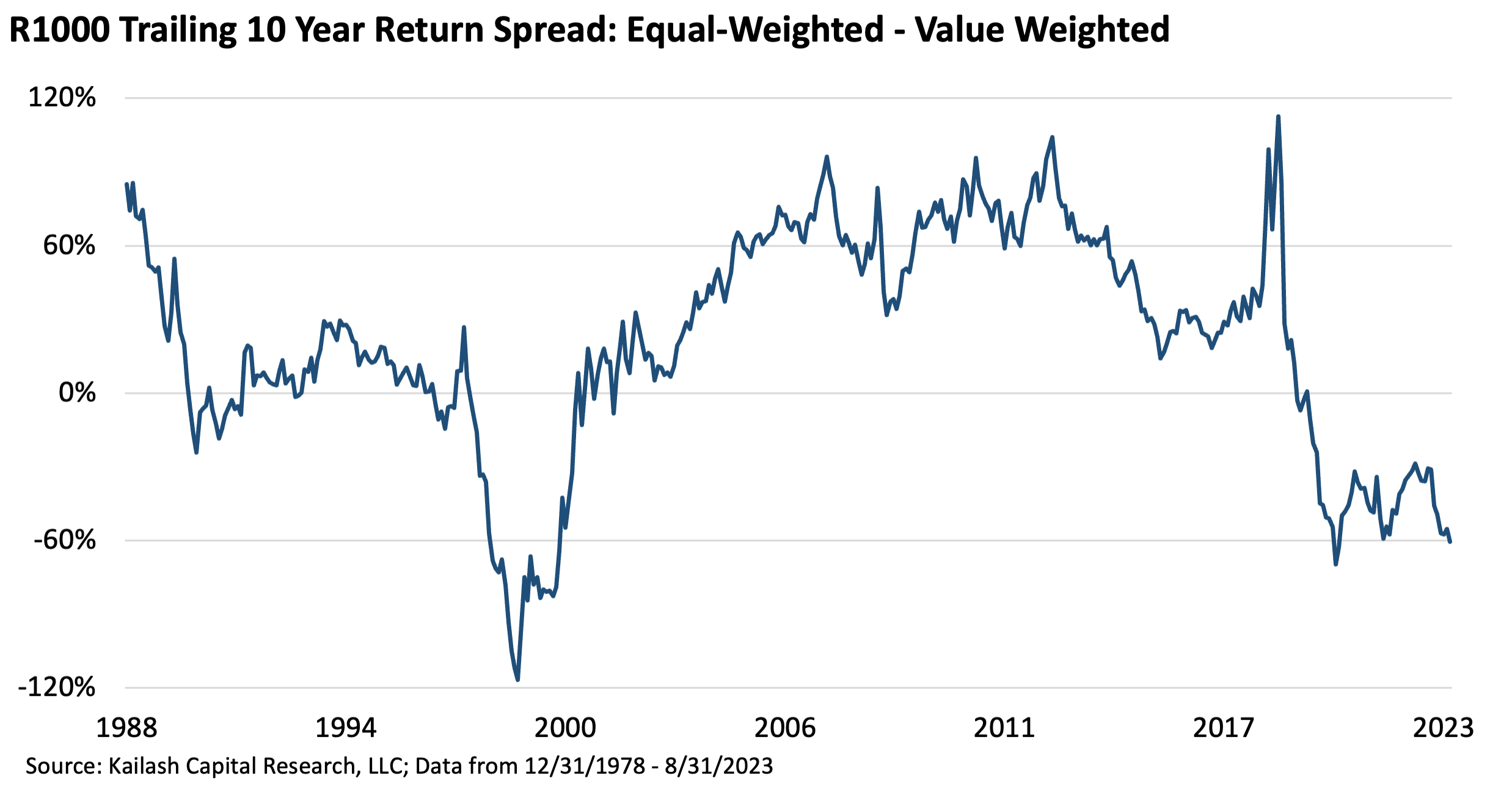

Equal Weight S&P 500 Indexes: A Panacea for Concentration Risk?

KCR has written a blizzard of material on the increasingly dire investment implications of market capitalization weighted index funds due to the outsized performance of large stocks that now sit at brutally high multiples. This is hardly a new topic for us. In 2014, as “smart beta” strategies became wildly popular, we penned Indexing Dilemmas, which laid out the following facts:

“The Unified Field Theory of Overpriced FOMO Nonsense”: Financial Follies, This Time is Different & Other Rubbish

In a single Tweet on the demerits of a “fund of crypto hedge funds,” the legendary Cliff Asness managed to interweave the madness of meme-stocks and the...

The Solvency Debate Continues: A Quick Tour of the Financially Fragile

In August of 2021, we published Junk Stocks Funded by Junk Bonds, which noted that high-yield spreads had hit record lows. Our view was that record low-spreads on record-low nominal yields were a recipe for ruin. Using the Fed’s definition of financial fragility, we highlighted a group of equities that scored poorly on the Fed’s durability test and ranked poorly in our models.

Warren Buffett: Bond Investing, Private Markets & Complacency

"The private credit market has grown to the size where there is no edge other than the fake attraction of not having to mark their assets accurately and showing artificially low volatility. The space is competing for the same deals as the public market. So, the original concept where it was smaller specialty deals and the lenders had to pay up and give special terms is simply gone.

Stock Bubble Charts: YTD Update on the Echo-Bubble Driving Equities

Hello everyone. This is Matt from KCR. Today we will do what is effectively a tardy half-year update. The speed and tone will be quick and sharp as the year has been challenging for evidence-based investors like us. The summary is that the sharp speculative rally we have seen YTD

AI, Oil and Gas: Misadventures in Capital Allocation

Our recent pieces, How to Value Tech Companies and External Obsolescence: Tech Investors’ Newest Nightmare?, discussed how AI algorithms, big data, and machine learning could be undermining the moats of tech stocks that now sport multiples last seen during the dot.com mania. We noted that our empirically

A Nod to America’s Oldest Living World War II Vet

So often in the world, darkness takes over. Traumatizing events rock our foundations. Unexpected tragedies shock the world. And when these things happen, it affects people. We often grow a little darker. Cynical. Hardened. But some people—often the best of us—have the exact opposite reaction. They go through the worst and come out of it with a positive attitude and a sense of gratitude.

How to Value Tech Companies Everyone Loves?

“Disturbing research warns AI may be the ‘Great Filter’ that wipes out human civilization” -The Independent “…artificial general intelligence or AGI is AI’s ‘big brass ring’ and will become a trillion-dollar industry by the 2030s…it will also do good in the world.” -Business Insider “What is certain is that creating [artificial general intelligence] AGI is the explicit aim of the leading AI companies, and they are moving towards it far more swiftly than anyone expected...

External Obsolescence: Tech Investors’ Newest Nightmare?

The definition of external obsolescence principally applies to real estate. One real-estate firm explains that “...external obsolescence is something outside of a property, off-site, that negatively affects its value. Definitions of external obsolescence often include the chilling term “incurable,” and examples are trains, traffic, commercial properties, institutional properties, geologic conditions, and industrial installations.”