Innovation as an Asset Class: The Implosion of the Nasdaq 100 & Ark Invest ETF

2020 was a brutal year for KCR. US bonds rose to offensive levels, offering investors a 0.50% yield, while equities soared to valuations above the dot.com peak. The pain for our team was intense.

Our evidence-based investment process is driven by historical data, algebra, and common sense. By the end of 2020, there was nothing less common than common sense. Basic maths were tossed out the window and replaced by empirically impossible narratives spouted by promotional fund managers and CEOs.

The two years that followed this peak in financial insanity made KCR look intelligent.

This success did not stem from any brilliant forecasts by the team. Rather, we credit our unwavering faith in behavioral finance, which shows that human beings repeat the same mistakes every market cycle. History has taught us that nobody learns from history in financial matter.

Get our insights direct to your inbox: SUBSCRIBE

Coming off a string of winning years like 2021 and 2022, KCR is here to warn our readers of the obvious: nothing happens in a straight line. Today’s story is a cautious one. Results have been “too good for too long.” The market is a humbling machine, and we may be overdue for some uncomfortable months.

As always, we look to history for guidance. Today we will be focusing on price action first and then closing with fundamentals. Like our piece, Anatomy of a Bear Market, which documented how the fallout from speculative bubbles led to violent volatility, we will be looking at the dot.com analog using the NASDAQ 100 Index in the dot.com bubble and ARK Investment Management today.

Get our insights direct to your inbox: SUBSCRIBE

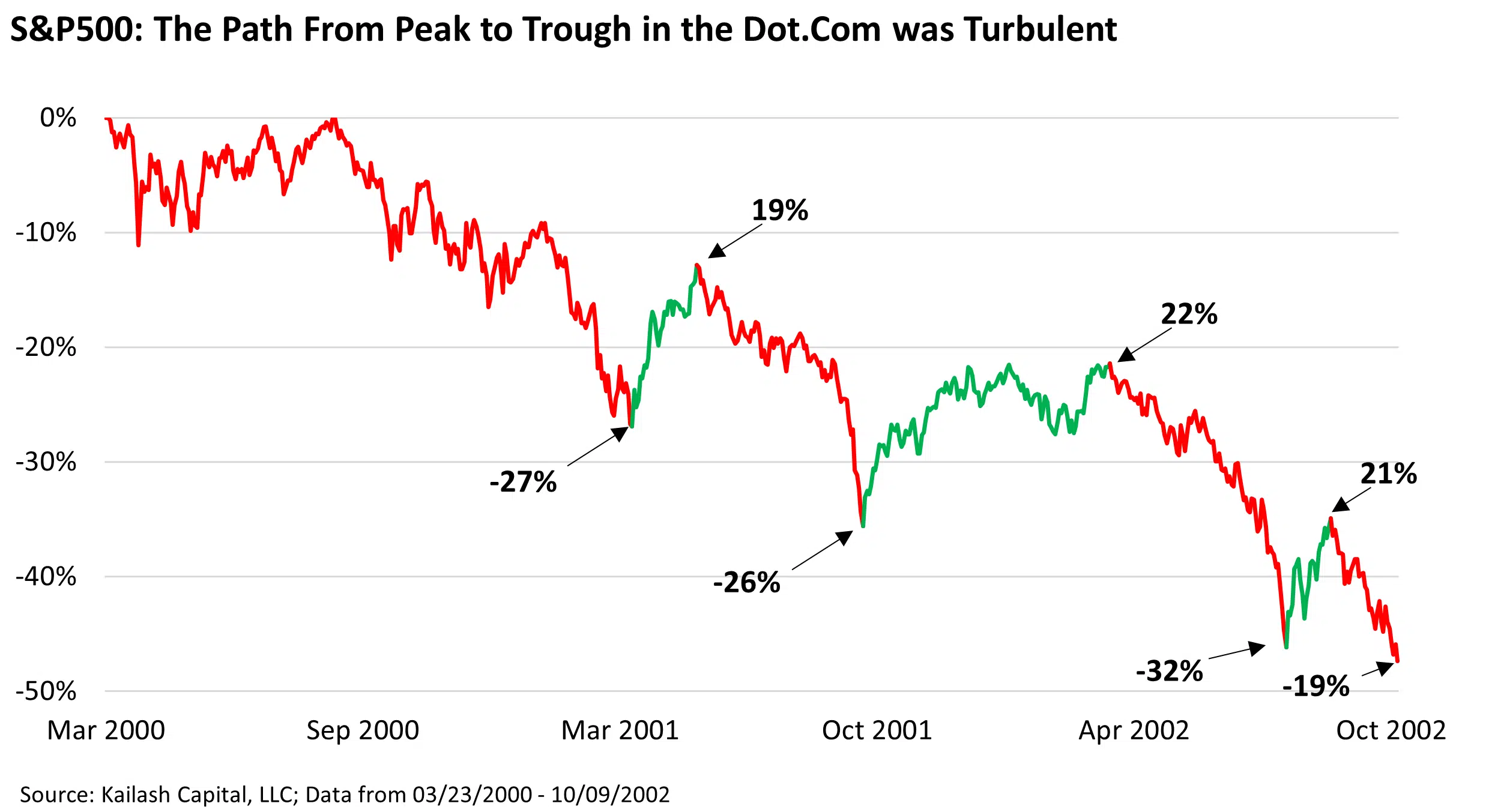

We’ll start off using the S&P 500 before jumping into those more speculative holdings. The chart below shows the decline in the S&P 500 from the peak of the dot.com bubble on 03/23/2000 to its trough on 10/07/2002.

The full extent of the -47% decline is shown on the left-hand axis. Along the way we highlighted in green the counter-trend rallies. Each annotation along the way shows the decline and subsequent rally from the relevant low. Example: the first leg down, the index fell -27%. From there it rallied 19%. Then fell -26% before ripping 22% higher. The path to the final bottom, -47% lower, was characterized by violent volatility.

KCR believes the dot.com implosion is the only modern period analogous to the recent bubble. We have spilled epic ink explaining

Disclaimer

The information, data, analyses, and opinions presented herein (a) do not constitute investment advice, (b) are provided solely for informational purposes and therefore are not, individually or collectively, an offer to buy or sell a security, (c) are not warranted to be correct, complete or accurate, and (d) are subject to change without notice. Kailash Capital Research, LLC and its affiliates (collectively, “Kailash Capital Research, LLC ”) shall not be responsible for any trading decisions, damages or other losses resulting from, or related to, the information, data, analyses or opinions or their use. The information herein may not be reproduced or retransmitted in any manner without the prior written consent of Kailash Capital Research, LLC . In preparing the information, data, analyses, and opinions presented herein, Kailash Capital Research, LLC has obtained data, statistics, and information from sources it believes to be reliable. Kailash Capital Research, LLC , however, does not perform an audit or seeks independent verification of any of the data, statistics, and information it receives. Kailash Capital Research, LLC and its affiliates do not provide tax, legal, or accounting advice. This material has been prepared for informational purposes only and is not intended to provide, and should not be relied on for tax, legal, or accounting advice. You should consult your tax, legal, and accounting advisors before engaging in any transaction. © 2021 Kailash Capital Research, LLC – All rights reserved.

Nothing herein shall limit or restrict the right of affiliates of Kailash Capital Research, LLC to perform investment management or advisory services for any other persons or entities. Furthermore, nothing herein shall limit or restrict affiliates of Kailash Capital Research, LLC from buying, selling or trading securities or other investments for their own accounts or for the accounts of their clients. Affiliates of Kailash Capital Research, LLC may at any time have, acquire, increase, decrease or dispose of the securities or other investments referenced in this publication. Kailash Capital Research, LLC shall have no obligation to recommend securities or investments in this publication as result of its affiliates’ investment activities for their own accounts or for the accounts of their clients.