Mr. Buffett recently extolled the powerful economic moat of one of the world’s most iconic companies: Apple. Berkshire spent a bit over $30bn to acquire their Apple stake, which now sits at 936 million shares. The relentless rise in the share price puts Berkshire’s Apple position at $160bn today, their largest holding.

Mr. Buffett has dubbed the tech giant a consumer products company. No matter what you call it, Berkshire Hathaway’s Apple investment has created staggering profits. Tim Cook’s iPhone maker has charmed the Oracle of Omaha. Berkshire seems content to not-pay-taxes and hold this incredible profit engine.

We certainly understand his view and that of other Apple bulls. At 199 ranked, our model sees shares of Apple for what they are: a fantastic company trading at an unforgiving multiple. This leaves the stock in the dreaded land of “neutral,” an issue we detailed in Apple II Flashback: The Fantasy of Predicting the Future.

Get our insights direct to your inbox: SUBSCRIBE

Warren Buffett’s Apple Investment vs. a Popular Growth Stock

Unlike some other bloated market caps that rest on little to no profits, Apple is an extraordinary cash machine. Yet, in its most recent earnings report, the company showed the inevitable headaches around the law of large numbers.

Quite simply, growth gets harder as you mature into a monolith as shown in the below chart.

Source: Otavio Costa at Crescat Capital

At 30x monstrous ex-growth earnings, Apple’s PE ratio leaves little room for any equity risk premium. Yet this is hardly an anomaly, particularly in the land of big tech stocks.

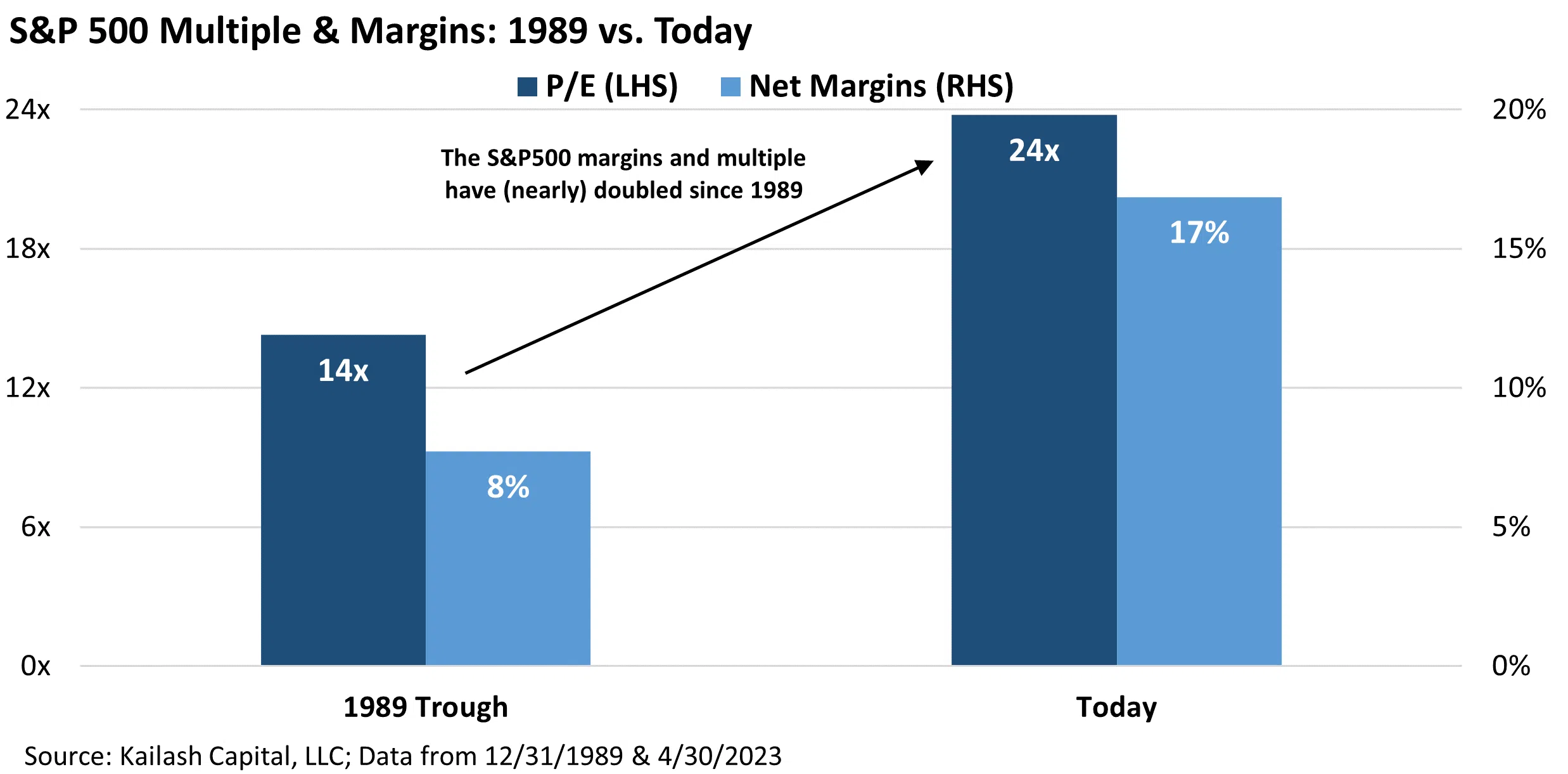

As KCR has extensively documented, US stocks currently sit at near-record multiples on record margins. The investing public is as bullish as any time in history on American equities. This stands in sharp contrast with 1989.

In that awful year, the investing public found little to like about US equities. The S&P traded at a 50% lower multiple on margins that were half today’s record levels.

With investors all-in on America today, it is worth noting that some have highlighted how Apple is effectively a Chinese company. KCR would also note that Mr. Buffett is putting new money to work in Japan.

Disclaimer

The information, data, analyses, and opinions presented herein (a) do not constitute investment advice, (b) are provided solely for informational purposes and therefore are not, individually or collectively, an offer to buy or sell a security, (c) are not warranted to be correct, complete or accurate, and (d) are subject to change without notice. Kailash Capital Research, LLC and its affiliates (collectively, “Kailash Capital Research, LLC ”) shall not be responsible for any trading decisions, damages or other losses resulting from, or related to, the information, data, analyses or opinions or their use. The information herein may not be reproduced or retransmitted in any manner without the prior written consent of Kailash Capital Research, LLC . In preparing the information, data, analyses, and opinions presented herein, Kailash Capital Research, LLC has obtained data, statistics, and information from sources it believes to be reliable. Kailash Capital Research, LLC , however, does not perform an audit or seeks independent verification of any of the data, statistics, and information it receives. Kailash Capital Research, LLC and its affiliates do not provide tax, legal, or accounting advice. This material has been prepared for informational purposes only and is not intended to provide, and should not be relied on for tax, legal, or accounting advice. You should consult your tax, legal, and accounting advisors before engaging in any transaction. © 2021 Kailash Capital Research, LLC – All rights reserved.

Nothing herein shall limit or restrict the right of affiliates of Kailash Capital Research, LLC to perform investment management or advisory services for any other persons or entities. Furthermore, nothing herein shall limit or restrict affiliates of Kailash Capital Research, LLC from buying, selling or trading securities or other investments for their own accounts or for the accounts of their clients. Affiliates of Kailash Capital Research, LLC may at any time have, acquire, increase, decrease or dispose of the securities or other investments referenced in this publication. Kailash Capital Research, LLC shall have no obligation to recommend securities or investments in this publication as result of its affiliates’ investment activities for their own accounts or for the accounts of their clients.