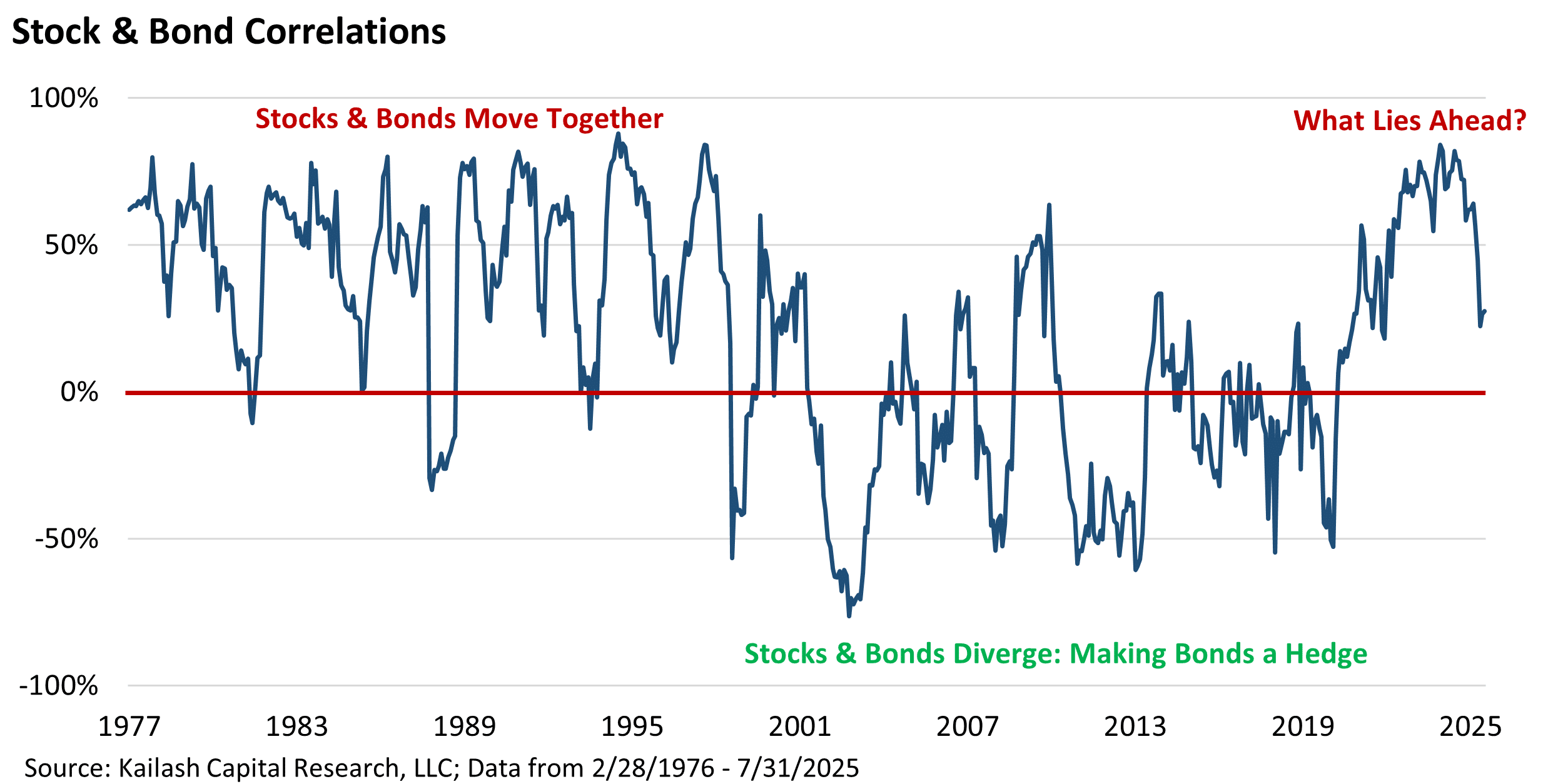

Uncertainty: The Leading Cause of Illness in Healthcare Investing?

What’s causing the current malaise in healthcare stocks? Returns have been lagging and valuation multiples are lower than the vast majority of stocks in the S&P 500. We doubt everyone has become so much healthier that we no longer need medicines and hospitals. Is this as simple as “Healthcare isn’t Tech”? We don’t think so.

Accountability with KCR: Our Views on Tech Since Our Founding

The research published in this newsletter is organized and authored by a group of fund managers and researchers who have over 90 years of combined experience and have worked together for over 14 years. As long-time readers know, our sister company, L2 Asset Management, runs a collection of long-only as well as long/short products.

Pediatrix Medical Group, Inc (MD)

Pediatrix Medical Group, Inc. (MD) operates a nationwide network of more than 2,300 affiliated physicians who provide neonatal, maternal-fetal, and pediatric specialty care. As of December 31, 2024, 1,335 of MD’s neonatal physician specialists provided clinical care, primarily within hospital-based neonatal intensive care units (NICUs), to babies born prematurely or with complications.

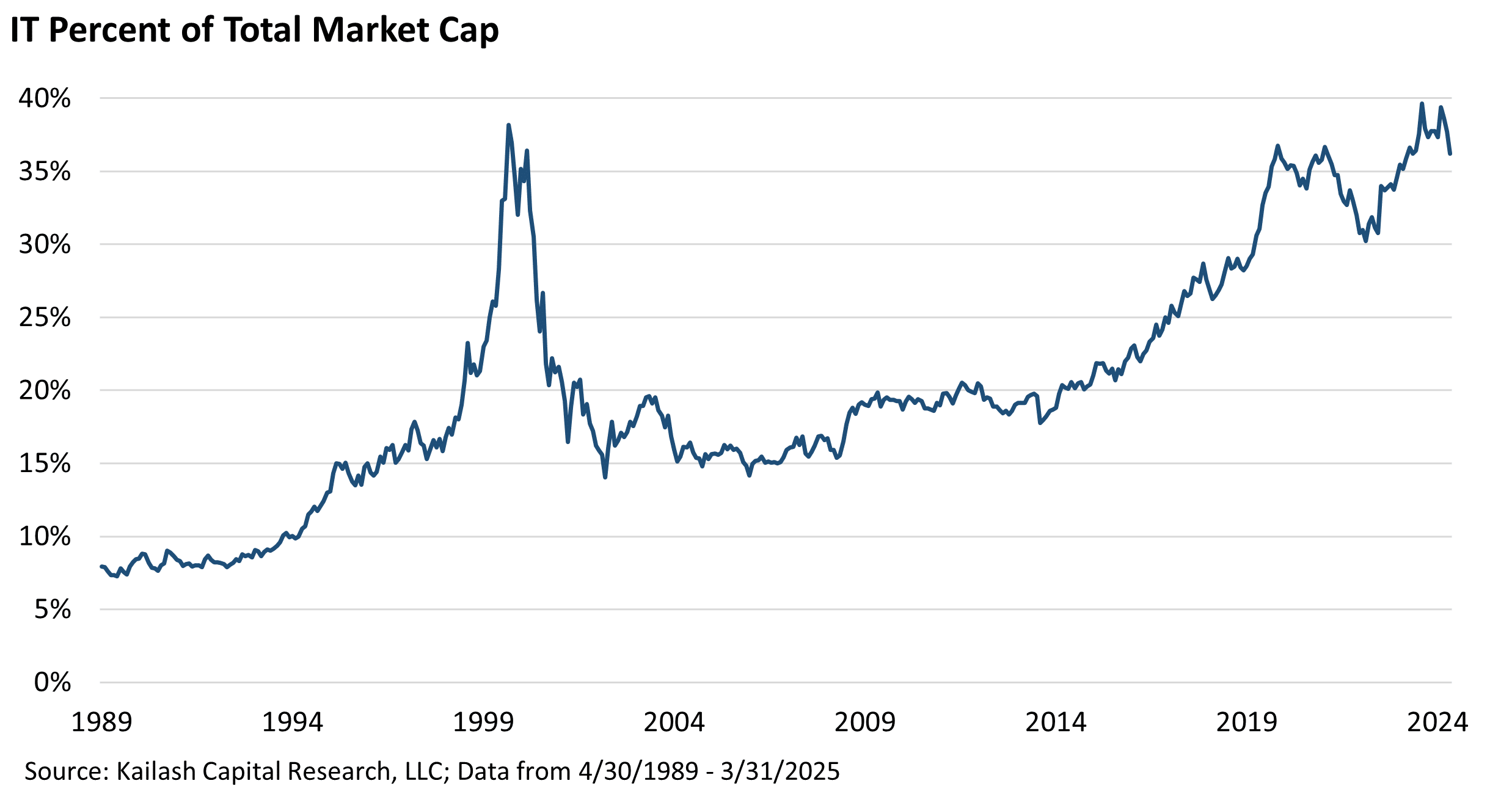

Tackling Technology’s “Earnings Elephant” – the Great Grift Continues

Our last white paper on tech, The Troubles of 2025 are on Full Display, demonstrated that: • Technology’s share of total market cap has eclipsed the prior peak in the dot com bubble • Technology’s bloated market cap has come, in no small part, from multiple expansion

We Have Been Wrong: We are SO Back!

Watching the mega-cap bubble reflate in 2024, the research in this newsletter peppered readers with warnings about the law of large numbers, soaring capital intensity, dubious accounting and vendor financing activities.

Could Evidence Based Investment Processes Predict the Future? AMGN & The Case for KCR’s Fact-Based, Forecast-Free, Investment Methods

Answer: Nobody can predict the future. With that done, let’s revisit a moment of pain for the KCR team. October of 2010 marked the single first ranking list produced by KCR. The top-ranked stocks were a magnificent collection of companies, in our view. Stocks like Lubrizol, Microsoft, Lorillard, Discover Financial and the 8th ranked stock, Eli-Lilly, sat as our highest ranked healthcare name.

A Tech Talk: The Troubles of 2025 are on Full Display

Today’s piece will discuss the current state of tech investing in US markets. A decade of zero interest rates coupled with the dramatic and unsustainable fiscal stimulus post Covid has taught investors a precarious lesson:

Venture Capital: Turning Today’s Dreams into Tomorrow’s Write-Downs

KCR believes that many of the most speculative, loss-making, hype-driven, low-quality tech companies are actually in private hands today. Many of them held by venture capital funds. Why does this matter?

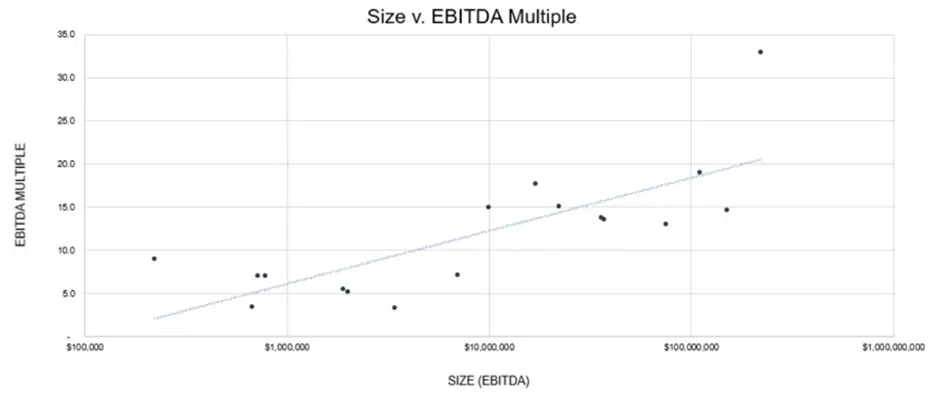

The Merits of Microcaps Continued: United Natural Foods (UNFI)

Just shy of a year ago, the KCR team wrote A Penchant for Pain: A Search for Big Returns in Small Packages. The piece made a table-pounding case to invest in

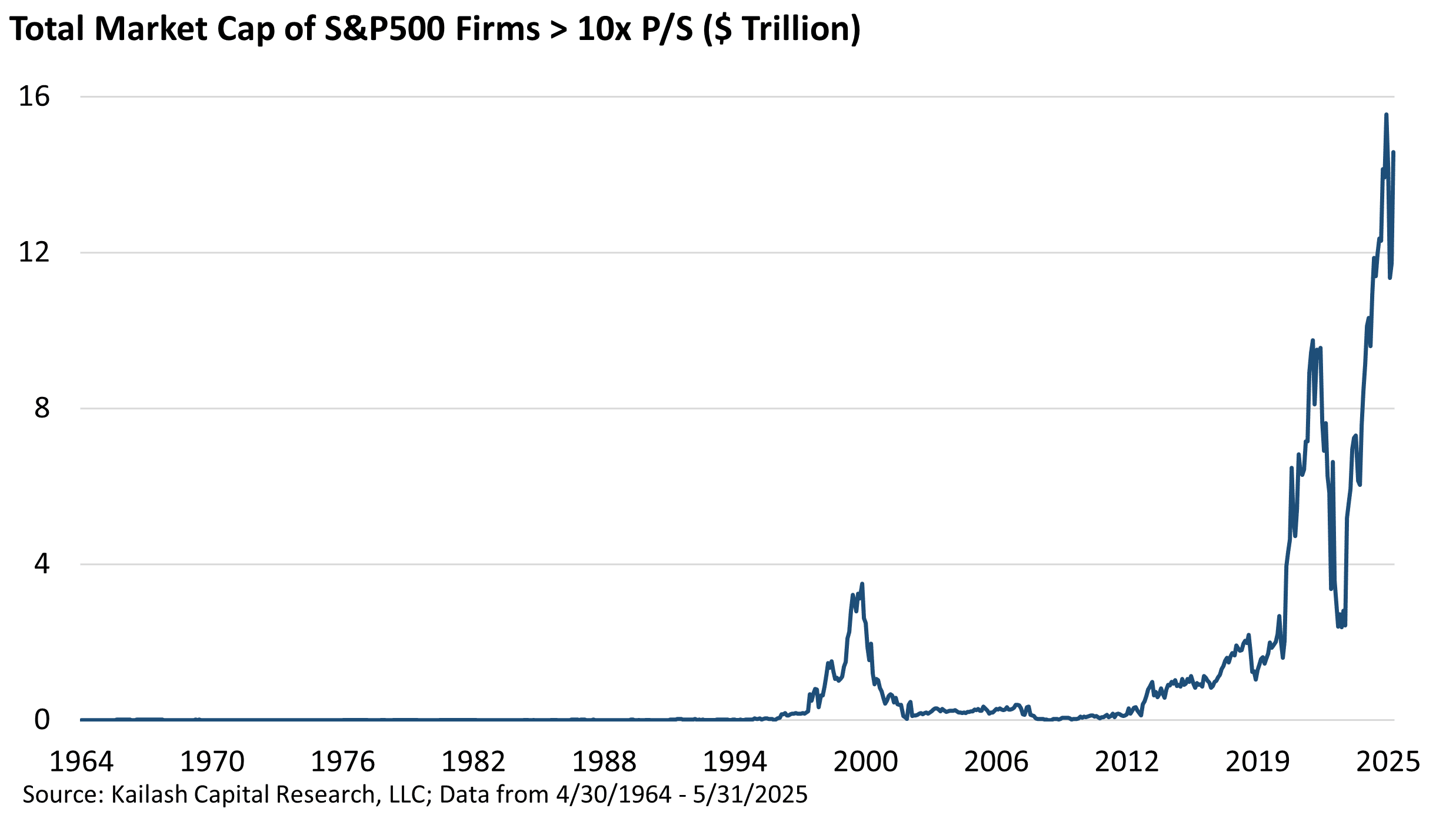

Sometimes the Most Obvious Things to Do are the Most Difficult

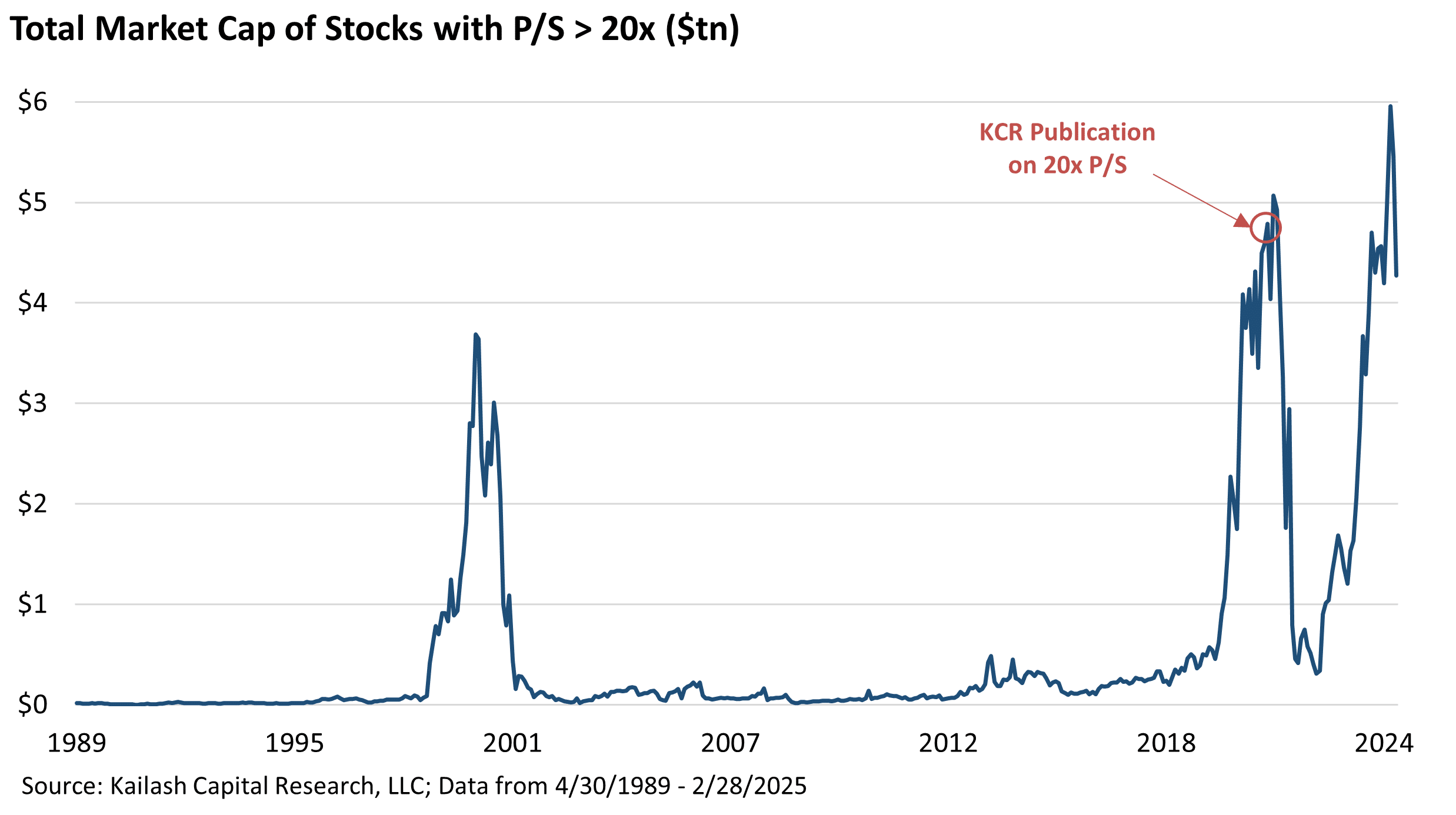

There are two times in a man’s life when he should not speculate: when he can’t afford it, and when he can. -Mark Twain Back in September of 2021, KCR penned a piece The Market Cap of Companies Over 20x Price to Sales is Out of Control. You can see on the chart below that

Is Capitalism in Crisis? Or is this cycle of stupidity just longer and larger than usual?

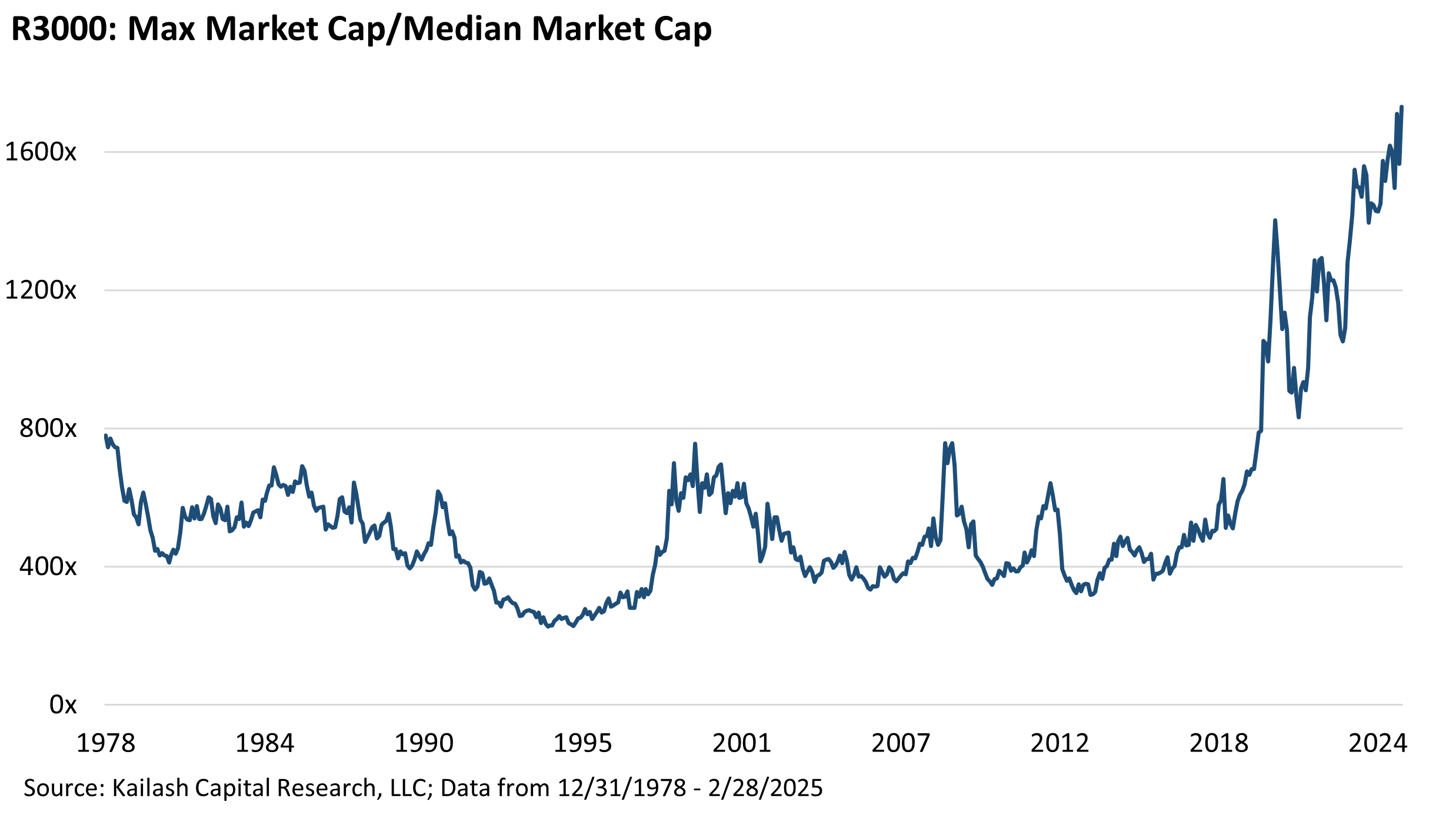

In our recent piece, If Not Now, When?, we pounded the table on the investment merits of mid-cap stocks. Much of the thesis rests on the unforgiving valuation of the Russell 1000 Index of large cap stocks. In that piece, we demonstrated that much of the overvaluation in the large cap index came from just the 50 largest stocks.

Midcap Stocks Part II: If Not Now, When?

In Part I of our piece on Midcap stocks, we led out with a chart showing that investors’ allocation to midcap stocks had fallen to levels last seen at the peak of the dot.com bubble; the lowest levels since 1964. We explained how investors willing to pivot into unloved midcaps in 1999 saw outsized gains while those who remained in the large cap index spent five solid years earning precisely nothing.