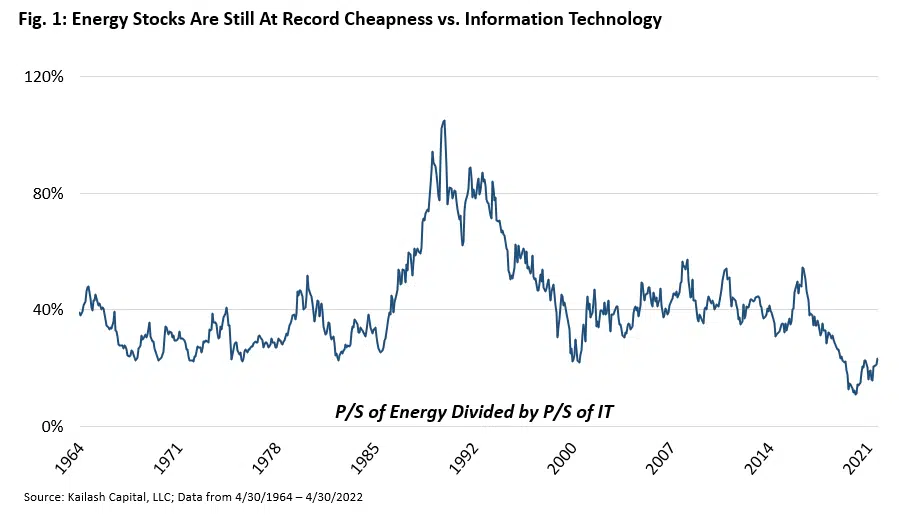

Is it Too Late to Buy Oil Stocks?

We get asked this question. A lot. Investors, scorched by multiple expansion in speculative stocks, are understandably concerned about the movement of prices in oil and gas. We believe the reason to invest in oil stocks stems from a fundamental backdrop for the sector, unlike anything we have seen in our careers.

Tesla PS Ratio & The Coming “Tax” on Index Fund Owners

The Persistence of High-Priced Stocks Sitting on High Hopes - Tesla PS Ratio: A Stock Price & Market Capitalization Problem Owned by the Many

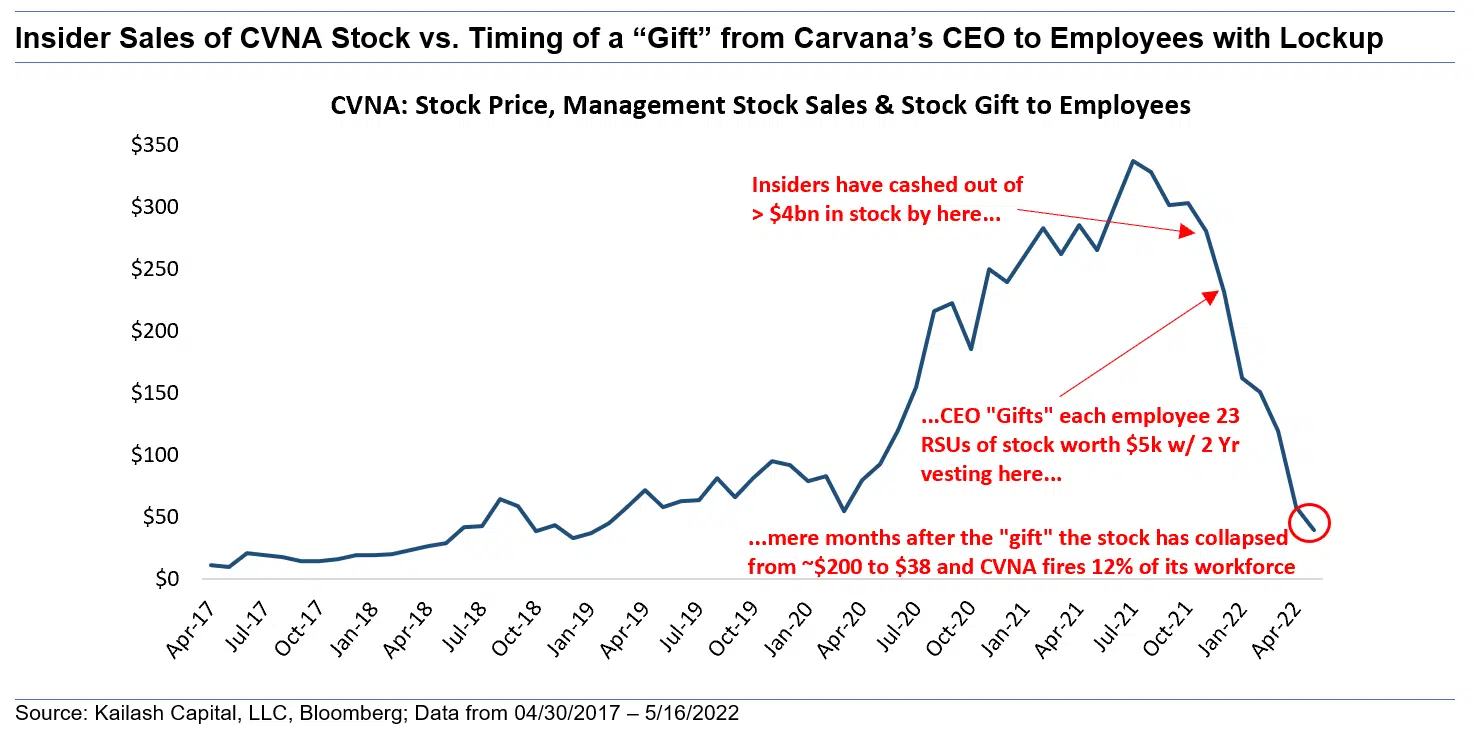

Carvana Investor Relations: A Tough Slog Ahead?

First, an important note: We have no beneficial interest for or against Carvana. Carvana has been panned by us here, here, and here, by Grant’s Interest Rate Observer, Seeking Alpha, Medium and by numerous other skilled and historically informed investors. On January 7th of this year, Carvana was the lead out stock in our “Enron look-alikes” list based on a proprietary KCR screen designed to….identify Enrons.

Vanguard Small Cap Index Fund: The Myth of Low Cost Indexing

A warning to long-time readers: we are about to agree with Elon Musk and Cathie Woods on something. They have come out against index funds due to the belief that they deprive investors of winners like Tesla (Ms. Woods) and that they have too much voting power (Mr. Musk).

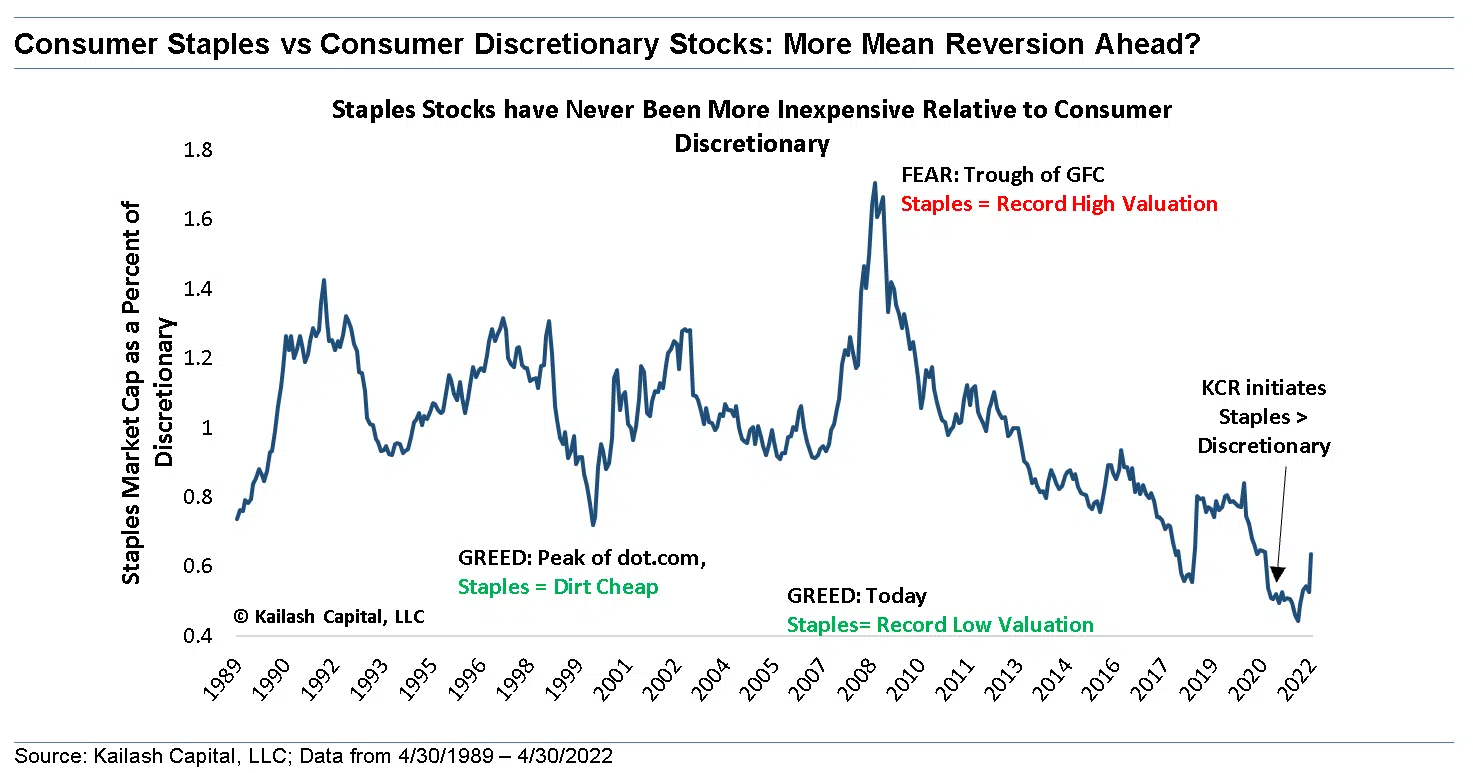

Consumer Staples Sector: A Speculative Refuge

Protecting & Growing Wealth in the Age of Uncertainty - From 2017 - 2020, speculative trading on predatory apps like Robinhood became a true stock market mania. The catastrophic misallocation of capital was, briefly, a very profitable endeavor. We did not flinch.

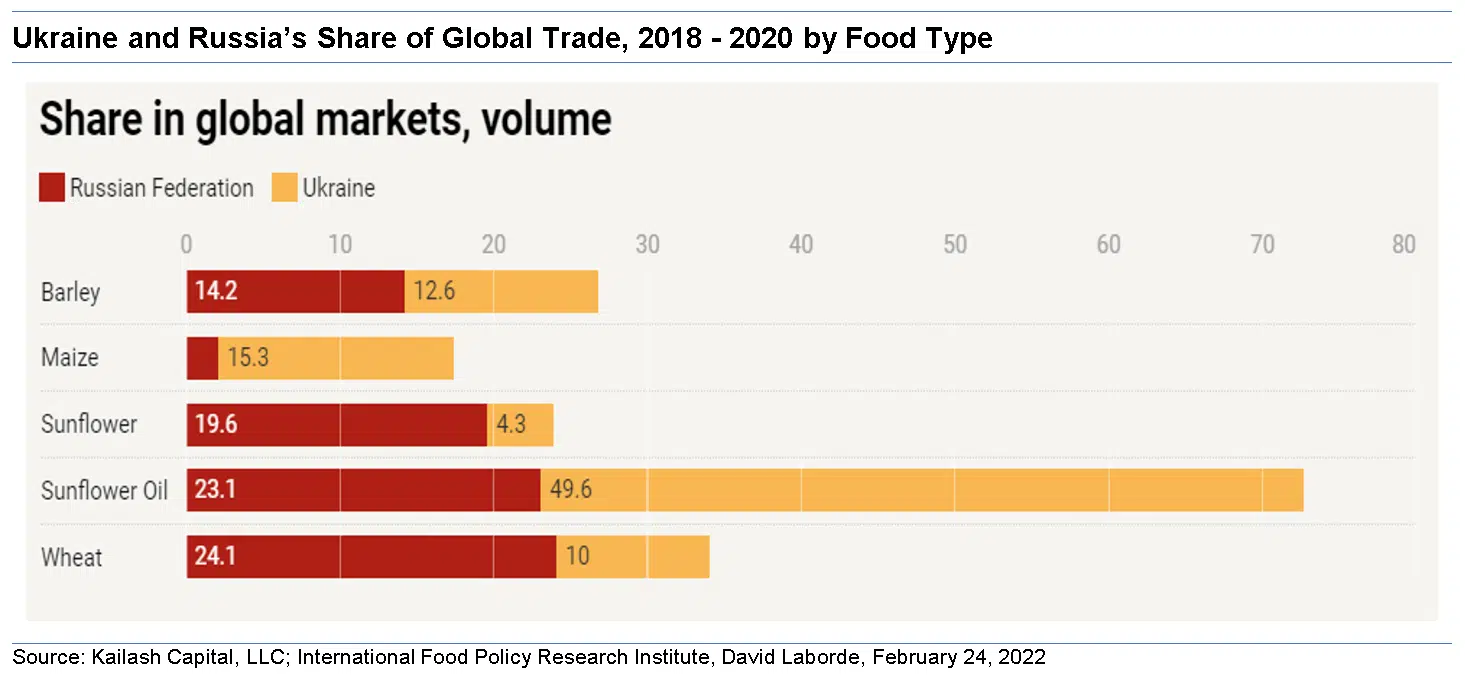

Protecting Capital Amidst War, Drought, Famine & Rising Food Prices

Consumer Staples Stocks, Food, Famine & POLITICS - In this paper, we are going to be talking about food prices and profits. Let’s get our political views on the table so you understand our beliefs and biases. True story.

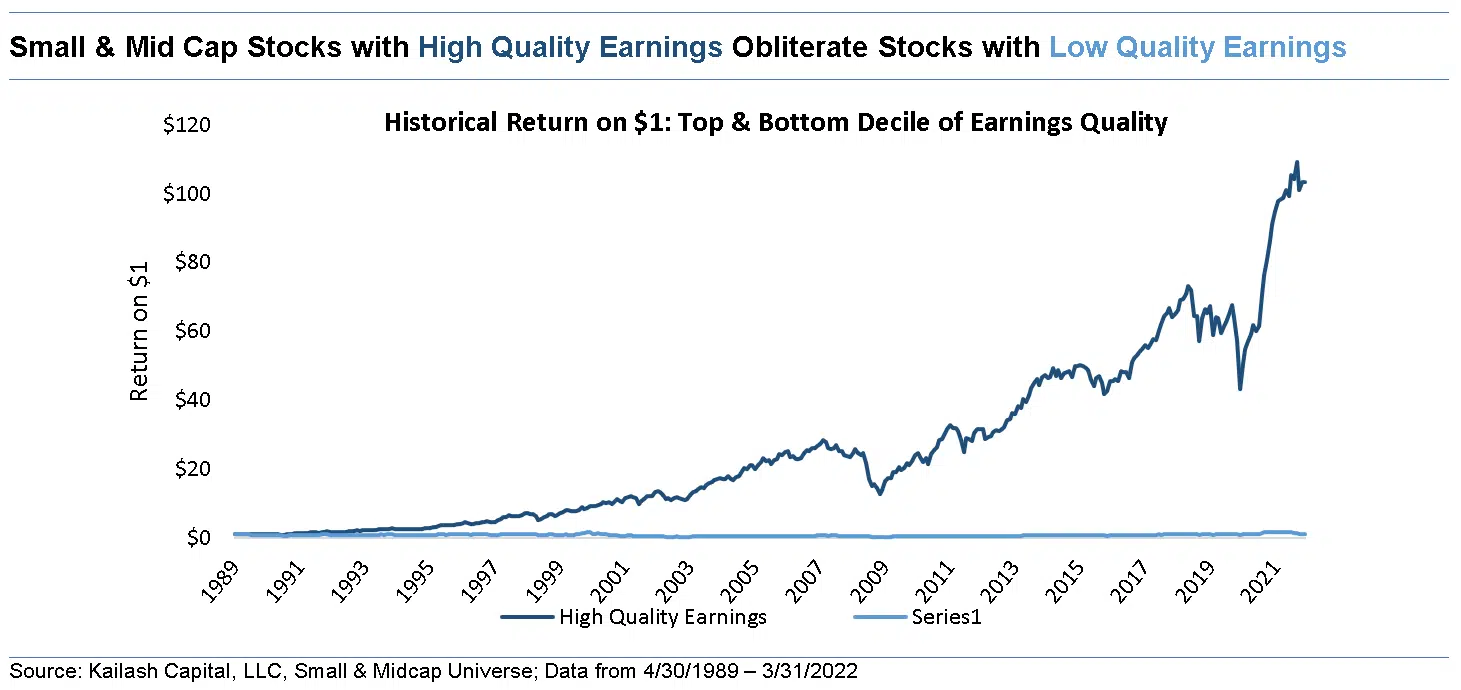

What Is Accounting Quality and Why It Matters

A Quick Walk Through the Recent Age of Miracle, Wonder & Other Lies - It has been a wild couple of years for financial statements. And by “wild,” we mean the quality of financial accounting information hit lows we could not have imagined. Let’s start with the basics.

George Noble, Finance, Fools & The Meaning of Multiples

A Rant About a Rant From one Boston Hedge Fund Manager to Another - An Introduction to George Noble

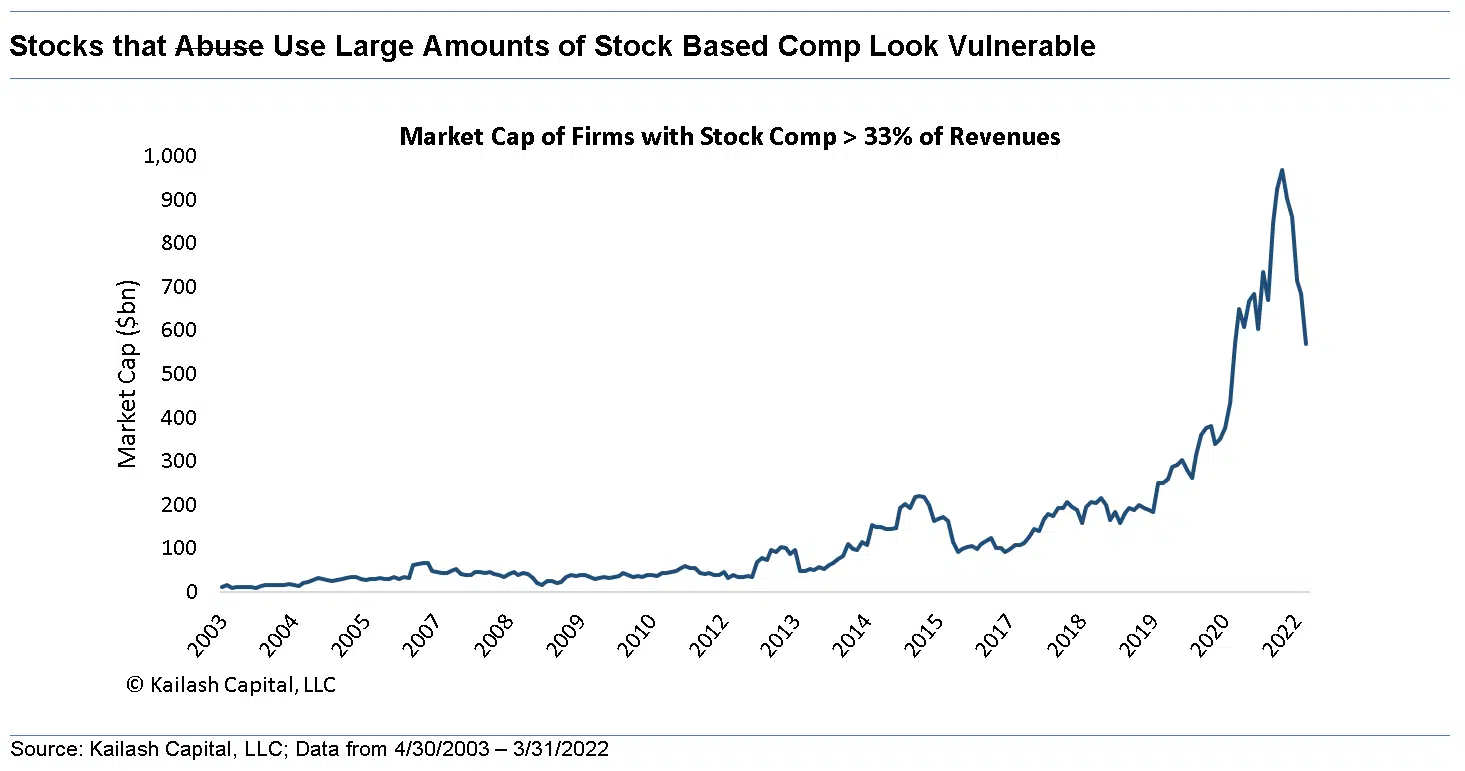

SBC Finance: An Update on the Absurd

The Real Cost of Stock Based Compensation Expense -- Stock Based Compensation (“SBC”) doesn’t matter for investors (and employees/employers) until it is ALL that matters.

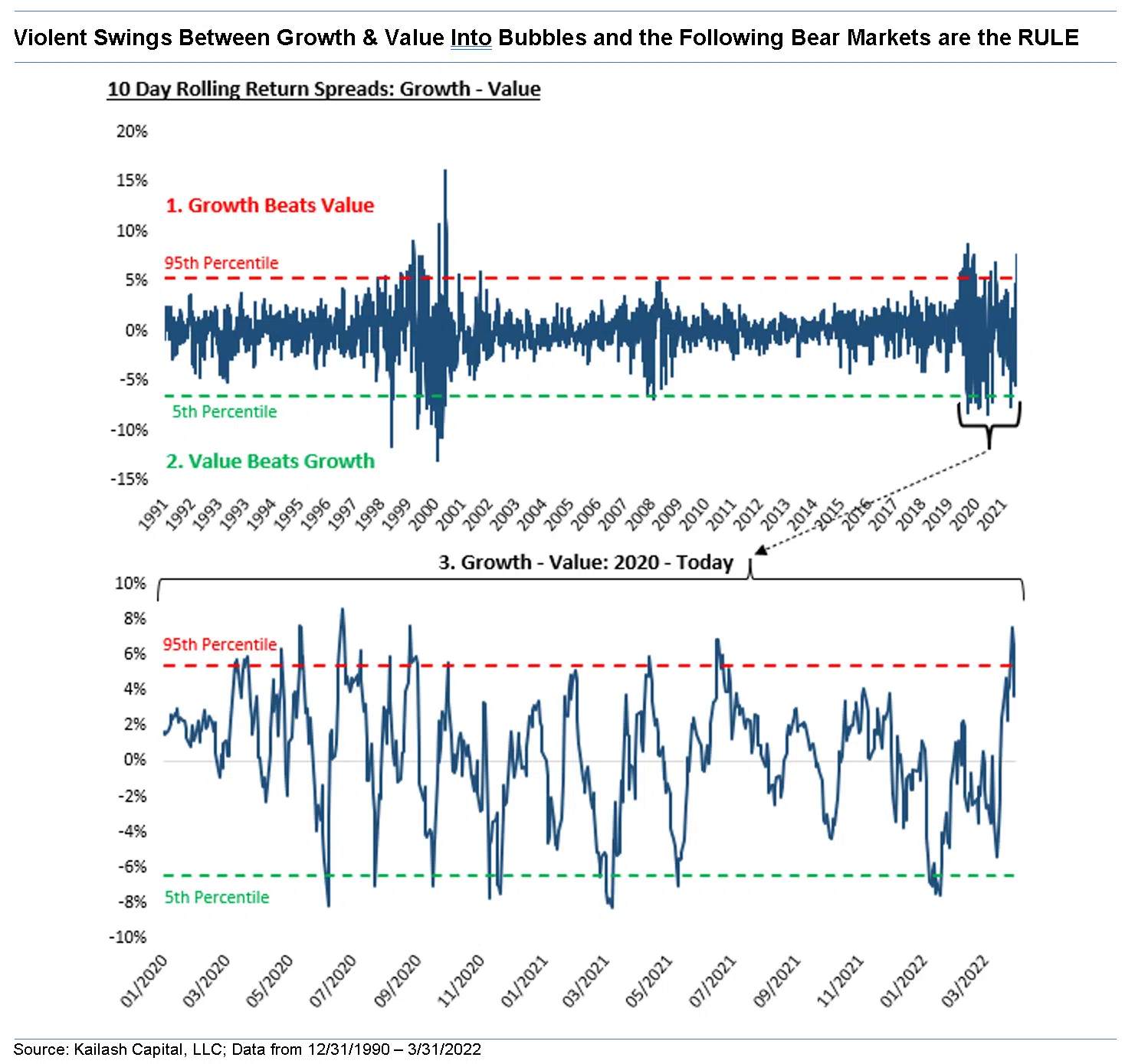

Anatomy of a Bear Market: Violent Volatility

A Quick Review of Equity Market Declines Post Bubble Peaks - Brutal end to Q1 for investors who buy cheap stocks, quality stocks, or some mix of the two. Quick review.

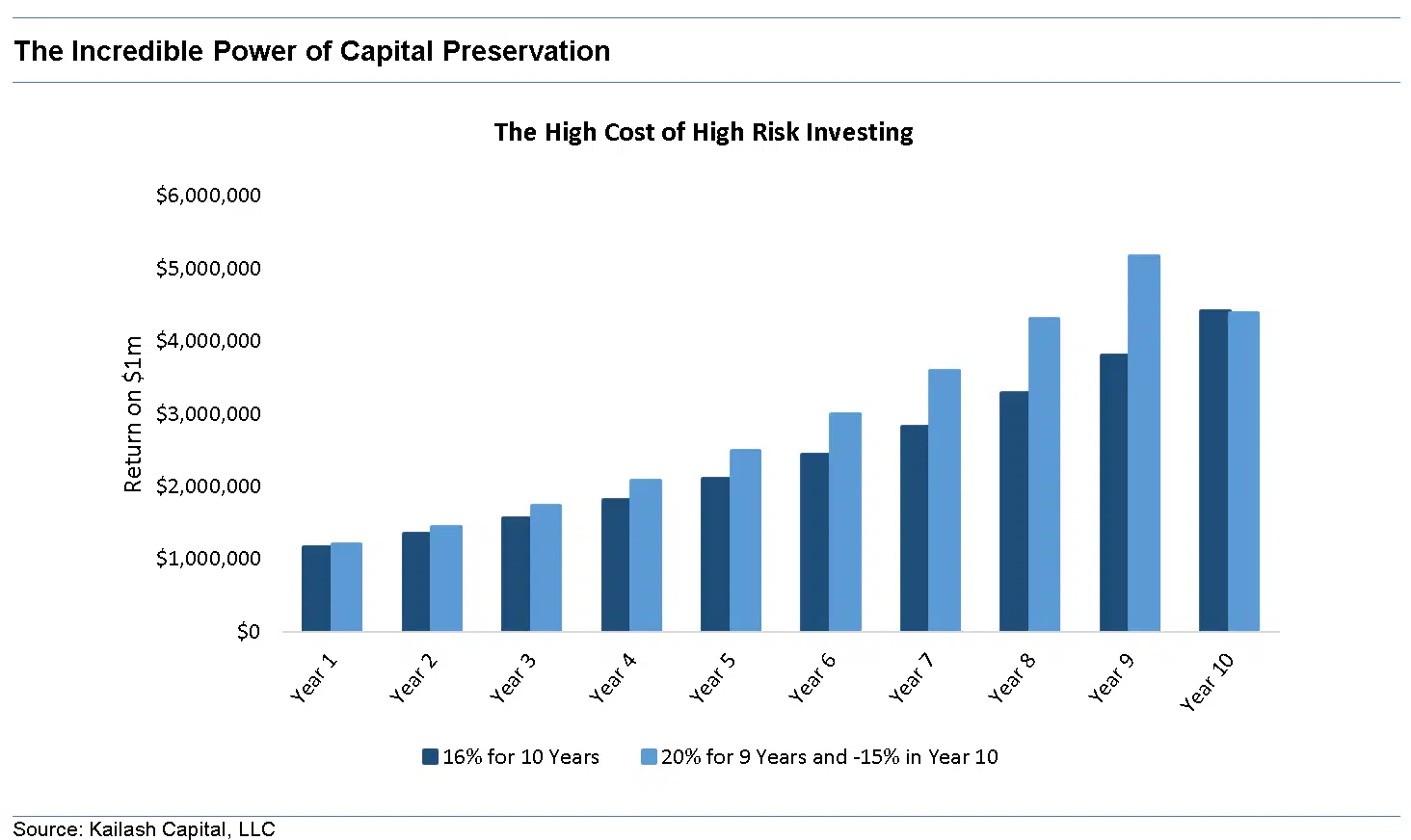

Private Equity Returns: Are Private Markets “Safe”?

Multiple Expansion and Two Markets to “Three Markets” – The High Risks to Small InvestorsIn his legendary book A Margin of Safety, Seth Klarman explains what few investors can remember ...

Growth Investing Gone Wrong: Avoiding the Double Bogeys

In Fast Growth Stocks, we explained the risks to “growth investors” seeking quick profits in some of the market’s most speculative firms. That rant laid the groundwork for our paper explaining the obvious opportunity to invest in growth companies at reasonable prices. A once in 20-year opportunity, in our view.